By Cami Pendell

By Cami Pendell

In a time of sharp divisions and fiery rhetoric, civility can seem like a remnant of a quieter past. But for those committed to advancing free markets and limited government, civility is essential to progress. It is the foundation on which durable ideas are built, tested and ultimately adopted.

This article originally appeared in The Detroit News March 3, 2026.

Gov. Gretchen Whitmer’s administration is not over, but her final State of the State address last week marks the beginning of the end. A governor’s first State of the State is about the agenda. The fourth address is the case for continuity and reelection. The eighth is about legacy, accomplishments and unfinished business.

Michigan’s budget process has been sharply improved by new statutes that require legislators to file public requests when they seek grants for projects of their choice. It used to be that these grants, sometimes called earmarks or pork projects, popped into the budget at the last minute with no public warning. Now legislators have to describe the projects they want and what the money will be used for. The process gives legislators a chance to show that that their requests benefit all Michigan residents, not just the direct beneficiaries.

Gov. Gretchen Whitmer is stretching the limits of her emergency powers, just as she did during the COVID-19 panic. She declared a state emergency on April 2, suspending some state rules about what kind of gasoline may be sold, because prices reached $3.89 per gallon. State law gives governors the authority to unilaterally suspend rules or laws, among other actions, in case of an energy shortage. But Whitmer’s justification is based on high gas prices rather than a threat to Michigan’s energy supply.

Food trucks in Michigan have been banned, overly regulated and even, occasionally, subsidized. None of that has been good public policy, and state lawmakers are doing something about it. A proposed package of bills would set up a new framework.

House bills 5450 and 5451 are sponsored by Rep. Timothy Beson, R-Bangor Township. They would, according to Michigan Votes, “revise Michigan’s Food Law to create a more uniform statewide regulatory framework for mobile food establishments by prohibiting local fees and taxes on mobile vendors, while also strengthening safety and transparency through mandatory annual and post-modification fire inspections, public access to inspection records, and standardized compliance and reporting requirements.”

Special economic zones have brought prosperity to places like Hong Kong and Singapore, but they have never been tried in the United States. Michigan developer Rod Lockwood wants to change that by turning Detroit’s Belle Isle into a separate polity that would avoid the Motor City’s crushing taxes and regulations. In a new version of his 2013 novel “Belle Isle: Detroit’s Game Changer,” Lockwood demonstrates how a special economic zone on the island, which now serves as a park, could turn around the fortunes of Detroit as well as Windsor, Ont., and the entire Midwest.

Even the biggest opponents of a bill to make zoning less burdensome agree that local zoning rules prevent the housing people want from getting built. In response to a bill to preempt local governments rules that prohibit most types of housing to be built, local government advocates introduced their own legislation to subsidize local governments that loosen building rules.

Most people agree that local zoning rules are preventing construction of the kind of housing people want – even municipal governments themselves. Two bill packages in the Michigan legislature, including one proposed by associations for local governments, propose to reduce the zoning burden at the local level.

Michigan lawmakers had $9 billion in expected surplus funds at their disposal in January 2023. Many people today wonder what happened to that money. The short answer is that lawmakers spent it. The better question is whether the spending was worth it.

Michigan ranks 16th on the Tax Foundation’s State Tax Competitiveness Index. Ranking in the top third is fairly good, but Michigan’s trajectory is not. The state ranked 11th only five years ago and has been sliding ever since. While other states improve their tax competitiveness, Michigan is standing still.

The ongoing litigation and legislation campaign against Mackinac Island ferry operators became a little clearer when a federal judge dismissed the city of Mackinac Island’s antitrust claims against the ferry companies. The city had claimed that the current arrangement among the ferry companies is an illegal monopoly and tried to assume the power to regulate ferry fares and parking fees on mainland parking lots.

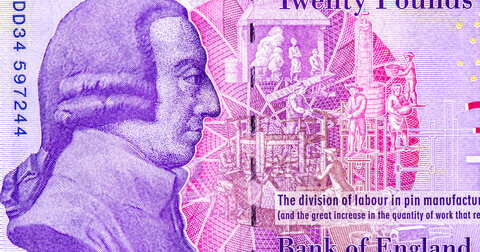

Americans will celebrate the 250th anniversary of our nation’s founding this July, and rightly so. But March marks another significant event from 1776 that demands our attention.

A few months before the American founders approved the Declaration of Independence, the Scottish philosopher and economist Adam Smith published “An Inquiry into the Nature and Causes of the Wealth of Nations,” widely known by its shorthand title, The Wealth of Nations.

Rx Kids distributes cash to pregnant women and young mothers in Michigan. A pilot program that launched in Flint in 2024 quickly expanded to dozens of cities. Lawmakers gave $270 million to the program this year.

Nobel Prize-winning economist Milton Friedman championed helping the poor with direct cash payments, and others agreed. Economic theory says programs such as Rx Kids should outperform typical government welfare systems, which are run by distant bureaucracies and controlled by politicians. Rx Kids takes a different approach and trusts that recipients know how to help themselves better than government officials do.

Michigan is finally inching toward putting its $1.6 billion share of federal Broadband Equity, Access and Deployment (BEAD) funds to work. Nearly five years after the federal bill was passed, the state of Michigan received approval from Washington for it’s final plan in order to access and deploy the funds. Things are moving at the speed of government.

This article originally appeared in USA Today February 19, 2026.

The past few years have been tough for criminal justice reform. While the 2010s saw a slew of smart state and federal policies, making communities safer and saving taxpayer money, concerns over crime in the 2020s put further progress on hold.

Jonah Goldberg has spent decades writing columns, authoring books, and appearing on television. But a few years ago, he decided the media landscape needed something different.

Goldberg joins The Overton Window Podcast to talk about where that led him: The Dispatch, a digital media company he co-founded with Steve Hayes that has quietly become one of the more interesting experiments in modern journalism.

Gov. Gretchen Whitmer recommends a series of tax hikes in her executive budget, spending that would boost state outlays beyond sustainable levels. The governor recommends a 4% increase in the state budget, not counting federal transfers.

Michigan lawmakers do not need to tax people more.

Congress is considering a 10% cap on credit card interest rates and President Trump voiced his support for such legislation in his Jan. 21 speech at the World Economic Forum in Davos, Switzerland. Trump said that capping the interest rate on credit card debt at 10% would “help millions of Americans save for a home.”

According to 23&Me, I don’t have an ounce of Irish blood in me. But that has never stopped me from appreciating a holiday that celebrates a holy man through festivities, eating salted meat, wearing silly green mustaches, and most importantly, drinking rather fine stouts. Some years I even dust off my old Leprechaun movies starring Warwick David for some fantastic entertainment.

This article originally appeared in The Detroit News February 24, 2026.

Two-hundred and fifty years ago, America’s founders pledged their lives, fortunes and sacred honor to launch this great national experiment. They laid the foundation, but the country’s future depends on us.

This article originally appeared in the Washington Times February 23, 2026.

President Trump is trying to make homeownership more affordable for families. If he wants to make lasting progress, then he should take an example from my home state of Michigan, where lawmakers unveiled a bipartisan package this month to lower the costs of building and buying homes. The plan rests on the time-tested principle that government simply needs to get out of the way.

In many of the cities we all love, most of the housing was built before Michigan established zoning laws, under a regulatory structure far less strict than the one we see today. Cities used to be built organically, driven by market factors and demand from residents. As a result, Michigan was affordable even when it was a fast-growing state.

A few years ago, my family was going to walk down the street to the school playground a few blocks away. We live in a quiet, safe neighborhood where all of our children walk to school.

Right before we left, our baby needed a diaper change. Our two older kids left to go to the park and, unbeknownst to us initially, our three-year-old started following them. We finished with the baby and walked to catch up – but when we turned the corner, she was with a police officer.

For several years, the punitive anti-innovation approach of California dominated state-level debates on Artificial Intelligence policy. Last year the tide started turning, with “Right to Compute” emerging as a more balanced alternative for preserving the benefits of AI innovation while protecting against the risks. Several states are considering Right to Compute laws in their 2026 legislative sessions. Michigan should do the same.

Michigan lawmakers operate a Field of Dreams economic development program. They spend millions buying land and preparing it for private businesses. But if the state builds it and companies don’t come, taxpayers are out the money and have no jobs to show for their trouble. It’s a bad structure that wastes taxpayer funds.