April 18, 2005 marks the 10th anniversary of The Michigan Economic Growth Authority, a program established by Michigan government with the mission of spurring in-state job creation and business investment. The authority is the state of Michigan’s agent for selecting firms to receive Single Business Tax credits in return for creating new facilities and jobs in Michigan.

April 18, 2005 marks the 10th anniversary of The Michigan Economic Growth Authority, a program established by Michigan government with the mission of spurring in-state job creation and business investment. The authority is the state of Michigan’s agent for selecting firms to receive Single Business Tax credits in return for creating new facilities and jobs in Michigan. These MEGA agreements also result in local incentives for the recipient firms, and often in other state incentives, as well.

MEGA was originally limited to providing packages only to firms that created new jobs at single sites in such industries as manufacturing, office operations, or research and development. Five substantive amendments to the program since 1995 have allowed MEGA to offer packages in return for smaller job and investment totals, for the retention of existing jobs, and for jobs in additional industries.

Through 2004, more than $1.8 billion in Single Business Tax relief has been offered to more than 200 firms in 230 MEGA agreements over as much as 20 years. The value of these MEGA agreements rises to more than $3 billion with the inclusion of other state and local incentives, such as property tax abatements, job training subsidies and infrastructure improvements. Nearly one-third of this total — $987 million — has been provided by local units of government or by local economic development agencies.

Scholarly estimates suggest that nationwide, the targeted incentives distributed by state and local governments exceed $50 billion annually.

The number of MEGA packages and the total size of the SBT credits offered each year has generally been rising, despite dips in 1997, 2001 and 2003. In 1996, MEGA’s first full year, MEGA offered just 15 deals, totaling $89.9 million in SBT credits. In 2004, however, MEGA produced 41 packages valued at $253.3 million (for up to 20 years) in SBT relief alone.

Direct Jobs

MEGA agreements are expected to create two types of jobs — "direct" and "indirect." "Direct" jobs are new jobs at the specific firm sites that are the subject of the MEGA package. "Indirect jobs" are new jobs created outside these specific firm sites in response to MEGA-related investment and direct employment.

State documents indicate that approximately 127 of MEGA’s agreements should have produced fully employed facilities through 2004 — i.e., sites hosting all of their projected direct jobs.

Of these 127, about 56, or 44 percent, have claimed credits under the MEGA program. A company can claim these tax credits, however, without meeting the initial total direct job projections.

In fact, only about 10 of these 56 cases can be shown to have created the number of direct jobs originally projected within the expected time frame.

MEGA originally projected that these 127 MEGA deals would generate 35,821 direct jobs by 2005. MEGA figures obtained in December 2004 shows that these deals have actually generated about 13,541 direct jobs — roughly 38 percent of original expectations.

MEGA’s direct job total through late last year thus represents about 0.3 percent of Michigan’s 2004 workforce.

Between 1996 and 2004, MEGA originally estimated that more than $220 million in SBT credits would be redeemed as a result of MEGA agreements. Lagging direct job creation, however, meant that companies claimed just $75 million in credits, or about 34 percent of original expectations.

Indirect Jobs

In two commentaries published in newspapers in November 2004, state officials claimed that the MEGA program had produced 28,812 total jobs. This figure is higher than 13,541 because it includes indirect jobs purportedly created by the program.

MEGA’s estimate of the indirect jobs in the 28,812 job total is unreliable for at least four reasons:

It employs a constant, rather than a varying, formula for MEGA’s diverse projects, even though MEGA’s own analyses show that these projects have different potentials for generating indirect jobs;

It implicitly employs assumptions about the economy in future years — well past 2005 — in order to estimate indirect jobs for past years;

It implicitly counts indirect jobs that would be created only after 2005 in its indirect job estimates for the past 10 years, thereby overstating the numbers;

It fails to fully correct assumptions made in earlier years that have since proved too optimistic, with the likely result of overstating the numbers.

Because MEGA could theoretically generate economic benefits despite its lagging success rate, the authors employed a detailed econometric analysis to determine whether MEGA credits influenced economic growth in Michigan counties during the years 1995 to 2002 (2002 was the last year for which county-level data are available). The authors also tested the impact of MEGA credits on the manufacturing, warehousing and construction sectors. The authors found the following:

MEGA did not improve Michigan’s per-capita personal income, employment or unemployment rate.

MEGA did not improve any Michigan county’s per-capita personal income, employment or unemployment rate (estimates of impact ranged from zero to modestly, though not significantly, negative);

Michigan counties that did not host companies receiving MEGA deals fared as well as counties that did host such companies;

MEGA essentially did not affect aggregate income or employment in manufacturing and warehousing (the one statistically significant effect was negative, but too small to be economically significant);

MEGA apparently caused a temporary shift to higher construction employment without increasing overall employment. One temporary construction job was created for every $123,000 in MEGA credits awarded; 75 percent of these jobs disappeared after one year, and the remaining 25 percent fell away after two. There was a concurrent, statistically significant decline in construction wages as a result of MEGA credits, but it was too small to be economically meaningful.

There are potentially several reasons why MEGA’s actual economic impact has been less than expected, as is shown by a review of specific MEGA projects, the academic economic literature and information about MEGA’s procedures. These reasons fall into four categories:

Political and Business Incentives Can Interfere With MEGA’s Policy Goals

Academic economic literature increasingly recognizes a "political economy" in public policy whereby political incentives to gain public approval for a program and its supporters can interfere with effective policy decisions. In economic development programs, this dynamic can favor projects with a higher public profile, such as those that benefit well-known or exciting new businesses or industries, even if these efforts are not necessarily the wisest use of resources.

State officials’ promotion of MEGA and other state economic development programs has in the past suggested political incentives may be playing a role in officials’ support for these policies. Legislative support for the Jobs I and Jobs II packages in 2003 appear to be instances of this.

Concern over potential political appeal may also be evident in several apparent overestimates of job impact by state officials in MEGA and related state programs. In one specific MEGA agreement, a company official detailed his disagreement with MEGA’s projections of job creation at his firm. Michigan’s auditor general has also twice criticized (non-MEGA) Michigan development agencies for the overstated job creation numbers the agencies had reported on audited programs.

Such overestimates of economic impact are not particular to Michigan. A Toledo, Ohio-area economic development agency recently reduced its own job creation claims substantially following the departure of an agency executive. Media scrutiny played a role in this reduction, but it came several years after the fact, and after the responsible official had departed — a delay in accountability that is unsurprising given the long-term nature of economic development programs.

The presence of targeted economic development programs can generate counterproductive business incentives, as well. A recent study of the state of Ohio’s economic development incentives between 1993 and 1995 found that while the incentives had no positive economic impact, the businesses that received incentives were more likely to overestimate employment forecasts than businesses that had not. Similarly, at least one major consulting firm has recently counseled businesses on how to position themselves aggressively to receive state economic development grants. Such tactics can lead government officials to favor less productive deals over better ones.

The MEGA program could begin to serve specific, short-term political and corporate interests, rather than the long-term goals that inspired the program. Not only might this combination of interests lead to a misallocation of state development monies toward less effective projects; it might also lead to lower economic growth, according to a 1999 study of state economic statistics in the continental United States.

The Inherent Complexity of the Marketplace

MEGA officials are faced with the task of picking companies that can create and sustain jobs in the Michigan marketplace. But the marketplace decisions that lead to new employment and new business investment in Michigan are made by millions of individuals with their own subjective preferences and individual understanding of local market conditions. The economic literature increasingly recognizes that the inherently dispersed nature of their knowledge and preferences makes predictions about which companies can successfully create and maintain new jobs exceedingly difficult for any observer or organization to determine. One recent analysis shows that that between 1995 and 2000, only one of the 45 largest stock funds outperformed the Standard and Poor’s 500 index, and it did so only by a small margin.

Assumptions in the "REMI" Modeling Employed by MEGA

MEGA engages economists at the University of Michigan to aid MEGA’s future employment projections through the use of a respected computer-based economic model known as REMI, short for Regional Economic Modeling Inc. The REMI modelers at the university appear to use the model skillfully and responsibly.

Nevertheless, several aspects of the model and the assumptions used with it may be leading to optimistic estimates. These issues involve the treatment of the direct cost of state tax relief, the cost of local incentives in MEGA packages, the differences between high- and low-unemployment areas, the failed employment and wage assumptions apparent in past simulations, and the potentially increased cost of new state and local government services following new business investment and employment.

The Problem of Ensuring MEGA Credits Are Necessary

State law specifically requires MEGA to determine that "the expansion or location of the eligible business will not occur in this state without the tax credits offered under this act." If there is an error in determining this — i.e., if a firm would have located in Michigan without the credit — the cost of the credit to the state and its economy rises.

In practice, making such a determination will be difficult, both for MEGA officials and for the firms concerned. Several case studies indicate how business calculations can change, so that an unattractive location may become attractive on further review, despite the absence of a tax credit. The potential for a revision of opinion can be particularly high if a firm already had strong reasons to locate in a particular location.

One way to determine the rate at which businesses might not ultimately need a credit that initially appears essential would be to study the subsequent actions of businesses that sought MEGA credits but were denied them. Gathering a comprehensive list of such firms has proved difficult, however.

End the MEGA Program

Given the underperformance of MEGA projects, the program’s manifest lack of economic impact in its first seven years, and the inherent difficulties in making such a program work, it would probably be best to cancel the MEGA program. The state has alternative ways to improve its business climate that are more likely to be effective.

Concerns about MEGA are only amplified by questions about the program’s fairness to firms that do not receive tax credits. These concerns are further underscored by a recent federal court case that suggests MEGA may be unconstitutional.

Other Reforms

While reforms of the MEGA program are unlikely to increase its economic value, policy-makers can take several steps that might improve MEGA if they choose to continue it:

Audit MEGA. The state could consider asking the Office of the State Auditor General to conduct regular, expanded audits of MEGA’s direct job counts. Such oversight could help improve the authority’s accounting procedures. The auditor general’s office could also be encouraged specifically to review applications by MEGA candidates that were rejected. The results of such a review could help clarify the extent to which the MEGA credits have truly been necessary.

Count Direct Jobs Only. It would probably facilitate public review and understanding of the MEGA program if indirect job benefits were no longer reported and cited by MEGA officials. "Spin-off" considerations could still be part of the evaluation process for a particular project, but MEGA would no longer make a formal or informal practice of tallying the indirect jobs its past and future projects could claim. Removing MEGA officials’ focus on indirect job counts might free the authority to more carefully document its direct job creation.

Develop a Transparent Framework for Tracking Success and Failure. The status of each MEGA project could be posted and updated live on the Web each month to show such basic items as the following: the state and local incentives offered in each MEGA package; the state and local incentives claimed in each MEGA package; the cost of these incentives so far and in the current year; the current direct job figures; what the direct job figures were originally projected to be at present; and so on. Such reporting would facilitate effective public oversight of the program’s effectiveness.

Commission an Independent Econometric Review. An independent researcher could be engaged to maintain a peer-reviewed and publicly transparent econometric model that annually reassessed MEGA’s impact. The model employed in this study was crafted to detect past impact, rather than predict future performance. Regular updates of the findings would therefore be appropriate if the MEGA program continues.

In recent decades, the age-old economic competition among the United States has turned into an economic battle for specific companies and jobs. It is a skirmish fought with targeted tax incentives, such as abatements in property or business taxes, offered to firms seen by government officials as particularly desirable for their ability to create jobs and stimulate broader economic growth.

Kenneth Thomas, a University of Missouri-St. Louis political scientist, estimates that the cost of U.S. state and local incentives provided to corporations every year is $48.8 billion in 1996 dollars[1] (though his figure excludes incentives offered in Kentucky, due to a dearth of data). Thomas is not the only scholar to tally a figure of this magnitude. University of Iowa economists Peter S. Fisher and Alan H. Peters believe the annual value of state and local incentives distributed in pursuit of “economic development” exceeds $50 billion.[2]

The Michigan Economic Growth Authority is Michigan’s primary tax incentive program. Established by former Gov. John Engler and the Michigan Legislature in the hope of fostering state job growth by encouraging specific out-of-state businesses to relocate to Michigan and specific Michigan businesses to expand here, the program’s 10th birthday is April 18, 2005.

State documents show that in the past 10 years, MEGA has offered business tax relief exceeding $1.8 billion to more than 200 companies in a total of 230 deals (the exact number of companies depends on how one counts subsidiaries and acquisitions).[3] This is a substantial track record. It allows us to form meaningful conclusions about the program’s effectiveness as an instrument for stimulating Michigan’s economy.

As we recount in "Appendix E: A Brief History of State Economic Development," there have been at least eight major institutional vehicles created since 1947 to carry out Michigan’s government economic development policies. These policies generally aim to improve the state’s economy by creating or retaining jobs either with specific companies or with specific kinds of companies, typically in order to promote diversification of the state’s economy away from the automobile industry. MEGA is currently the most prominent of the state’s economic development programs.

The creation of MEGA was particularly notable because of its primary champion, former Gov. John Engler. In the 1980s, Engler, then Michigan senate majority leader, had often criticized central economic "planning," chiding Gov. James Blanchard for such programs as the Michigan Strategic Fund, which was an earlier tool of state economic development planning. Engler argued that such programs were unfair because they failed to "treat everyone in the marketplace … equitably by dealing with Michigan’s oppressive tax burdens," and because such programs benefit a firm "if you are a friend of government, if you’re a friend of the current administration, if you know somebody … or any other number of keys that sort of unlock the magic door that controls these funds."[4]

When he came to office, Gov. Engler initially called for an end to state economic incentives. In February 1992, according to the Detroit Free Press, he and Gov. Jim Edgar of Illinois began trying to persuade their counterparts in other states to stop trying to lure each others’ commercial enterprises with targeted tax incentives. Engler reiterated his views at the August 1992 National Governors Association conference in Princeton, N.J., leading the Free Press to observe:

Engler believes — and he is backed by some economists — that such competition is bad in the long run because it creates an unfair tax system that often produces fewer jobs than promised. States, Engler said, should lure new businesses with good schools, low taxes and skilled workers — things that benefit all types of commerce.[5]

In keeping with these observations, Gov. Engler did implement a number of general policy changes meant to improve Michigan’s services and business climate, including tax cuts, privatization and public school choice measures. Nevertheless, following his unsuccessful attempts to persuade other governors to forgo targeted tax incentives and business subsidies, he chose to increase Michigan’s own targeted economic incentives — first, with his 1993 reorganization[6] of the state’s existing economic development programs, and second, with the introduction of MEGA, which offered targeted tax relief and other incentives to businesses to encourage them to invest or locate in Michigan.

The original MEGA law, passed in 1995, established the Michigan Economic Growth Authority as an eight-member state board that was directed by the chief executive officer of the then-Michigan Jobs Commission. This board administered the MEGA program, which provided Single Business Tax credits to corporations it chose following certain general criteria described below.[7]

MEGA’s agreements with targeted businesses required (and continue to require) a contribution to the overall MEGA incentive package from the local government or local economic development unit in the area hosting the new or expanded business facility.[8] These local business incentives usually take the form of tax abatements on real or personal property, though they sometimes include such items as permit waivers, road improvements and even discounted access to the local municipal golf course for the business’s employees.

The MEGA incentive package also can include state incentives other than Single Business Tax credits. The incentives, such as job training subsidies, were originally arranged by the Michigan Jobs Commission; later, they were provided by the Michigan Economic Development Corporation, an offshoot of the Jobs Commission that was established in 1999 to oversee the state’s primary economic development programs — including, in effect, MEGA as well.

The original law was relatively strict about who could qualify for MEGA credits. A business pursuing MEGA credits had to assure the state that it would in fact create new jobs at the specified Michigan site after the company’s executives signed the MEGA agreement. These jobs, in turn, had to involve such industries as manufacturing, research and development, or office operations. Retailing operations, such as a local Home Depot store, and tourist-related industries, such as hotels or restaurants, were excluded from assistance in the program.

The original law also required a MEGA recipient to meet relatively strict qualifications (most of these original qualifications remain despite subsequent amendments to MEGA law). As outlined in the Mackinac Center for Public Policy’s study "MEGA Industrial Policy: An Analysis of the Proposed Michigan Economic Growth Authority," the requirements included the following:

The business must create a minimum of 75 "qualified new jobs" if expanding in Michigan, or 150 qualified new jobs if locating in Michigan, within 12 months of opening the facility. A "qualified new job" means a full time job in excess of the number of jobs existing in the year before the new facility opens.

The business must agree to maintain the 75 (or 150) new jobs each year that a credit is received.

The business must agree to maintain a number of employees greater than the number employed in the year before the new facility is opened.

The average wage paid for the new jobs must be greater than the average wage paid by private-sector firms in that county.

The business must certify that the expansion or location would not have occurred in Michigan without the tax credit.

Local government must make a financial or economic commitment to the business for the facility.

The business must not have begun construction or announced the specific location of the facility.

It is the MEGA board’s job to determine if the proposed business facility or expansion meets the criteria above, as well as the following:

The expansion or location will "benefit the people of this state by increasing opportunities for employment and by strengthening the economy of this state."

The tax credit is needed due to a significant cost disparity — including economic incentives offered by a competing state — between this state and the competing state.

The business has a sound financial record based on the financial statements of the last three years.

The final step is for the MEGA board and the business to execute a written agreement that officially makes the business an "authorized business" (that is) able to receive an SBT credit. The MEGA board determines the length of the credits (not to exceed 20 years). This agreement must provide that a misrepresentation in the application or a violation of the agreement may result in revocation of the "authorized business" status and loss of the tax credit.[9]

Since 1995, the MEGA law has been substantively amended five times. Three major aspects of these changes follow, and they remain in effect today:

The MEGA program’s "flexibility"[10] was enhanced, allowing additional kinds of businesses to participate with lower job and capital investment thresholds. Such changes increased the number of MEGA deals.

MEGA law now allows the board to hand out targeted relief to a business for retaining jobs that already exist, instead of creating new ones. It also allowed MEGA credits for "high tech," "rural," and "distressed" businesses, which do not have to create as many new jobs as were originally required under MEGA law.

MEGA law now allows certain approved companies to meet their job goals by counting the total number of jobs at multiple company sites, rather than just a single facility. The state also loosened minimum capital investment and aggregate job counts for multi-site facilities.

MEGA LAW

The following is a list of amendments that made substantive changes to the original Michigan Economic Growth Authority Act of 1995. This summary highlights the major modifications; not every change to the law appears in the text below.

This legislation expanded the MEGA law to include "high-technology" businesses. Authorized high-technology businesses were required to create both a minimum of five new qualified jobs at a particular facility and 25 more within five years — a departure from the original law’s requirement that 75 new jobs be created if the business was expanding in the state. High-technology businesses receiving MEGA packages also had to agree that "not less than 25 percent of the total operating expenses of the business will be maintained for research and development for the first 3 years of the written agreement."[11] No more than 50 high-technology MEGA deals were permitted in any given year.

The act also expanded to "make the retention of jobs and businesses a goal of MEGA SBT credits,"[12] meaning the MEGA program was no longer limited simply to the creation of new jobs. Companies qualified for "retention credits" by keeping at least 500 existing jobs in the state and making at least a $250 million capital investment in Michigan.[13]

Effective Jan. 9, 2001, this legislation changed the definition of the kind of "qualified new job" that could qualify for MEGA incentives. The original law’s definition required that jobs created by the authorized business be counted as a new job only after the expansion or location occurred in Michigan. The liberalization of MEGA’s "qualified new job" definition meant that a qualified new job also included a "full-time job at a facility created by an eligible business that is in excess of the number of full-time jobs maintained by that eligible business in the state 120 days before the business becomes an authorized business, as determined by (MEGA)."[14]

This legislation dramatically expanded the number and types of businesses that could qualify for MEGA deals. For instance, the bill allowed a retention credit for businesses that "made a capital investment of $100 million between three years before and two years after becoming an authorized business and agreed to maintain at least (1,500) jobs at the facility. …" The new law also stipulated that "the (retention) credit available under this provision could be granted only as part of a package of incentives that addressed international competition and included a negotiated labor contribution," such as a wage concession.[15]

Public Act 248 also expanded MEGA to include two new types of businesses, according to the following guidelines:

Distressed businesses. A business was deemed distressed if all three of the following criteria were met:

"four years immediately preceding the application to the authority under this act, the business had 150 or more full-time jobs in this state";

"within the immediately preceding 4 years, there has been a reduction of not less than 30 percent of the number of full-time jobs in this state during the three-year period"; and

the business "is not a seasonal employer." The law also limited MEGA to executing no more than 20 new deals or less for distressed businesses each year.[16]

Rural businesses. If a business were located in an area considered "rural" — a county of 75,000 people or fewer — it could qualify for MEGA deals provided it could create five qualified new jobs at an expanded or relocated facility and maintain 25 jobs within 5 years after the expansion or relocation. This requirement was similar to those for high-technology firms. Under the law, only five new rural deals could be approved annually.[17]

This legislation expanded MEGA law to allow businesses with multiple sites in the state to receive tax credits for retained or new jobs using employment totals from more than one facility. The legislation mandated that a company with multi-site authorization not only maintain 150 retained jobs at a particular location, but maintain 1,000 or more full-time jobs across Michigan and make new capital investment in the state.[18] The legislation also included four other ways for firms to qualify for MEGA approval.

This legislation again expanded MEGA law, providing more opportunities for companies to become an authorized business. For example, the law allowed a company to qualify for MEGA deals if it retained just 100 jobs at a single facility and agreed to make a capital investment of either $10 million or $100,000 per job retained at a particular facility, whichever was greater.[19]

The primary sources of financial data concerning MEGA and its related local incentives are documents produced by the MEDC and its predecessor agency, the Michigan Jobs Commission, obtained by the Mackinac Center under Michigan’s Freedom of Information Act. Graphics 2 and 3 (see links below) provide two-page samples of the "All MEGA Projects" and "MEGA Credits" spreadsheets that are referenced throughout this study.[20]

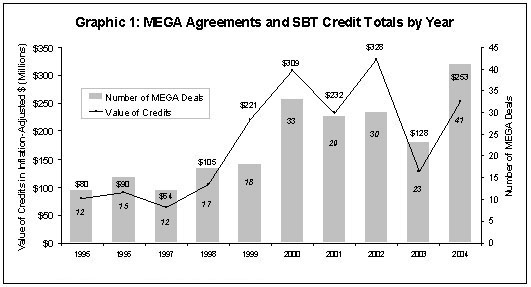

Since its inception, MEGA has offered targeted business tax relief exceeding $1.8 billion in a total of 230 deals to more than 200 companies or related subsidiaries.[21] (As mentioned earlier, the precise count of the companies involved in these deals can be debated, depending on how one treats acquisitions, subsidiaries or suppliers.[22]) Graphic 1 shows a year-by-year breakdown of total MEGA deals and the approximate, inflation-adjusted value of their respective MEGA credits.

The number of MEGA packages and the total size of the SBT credits offered each year has generally been rising, despite dips in 1997, 2001 and 2003. In 1996, MEGA’s first full year, MEGA offered just 15 deals, totaling $89.9 million in SBT credits;[23] only 25 MEGA deals were allowed annually at the time.[24] In 2004, however, MEGA produced 41 packages valued at $253.3 million (for up to 20 years) in SBT relief alone.[25]

The amount of MEGA state tax credits for individual firms has varied over the years, from a tiny offer of $160,000 to Integrity Design Inc. in April 2001 to an $88 million MEGA "retention" credit to the Ford Motor Company in November 2000 (these credits could be earned over five and 20 years, respectively).[26]

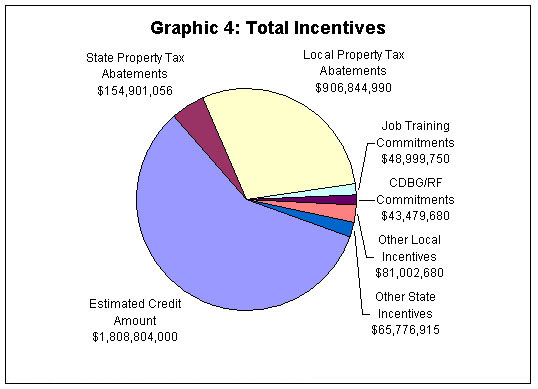

Each MEGA deal has included additional state or local tax incentives for the recipient firms. To date more than $987 million[27] has been offered to MEGA companies by local units of government or local economic development agencies. As mentioned earlier, local incentives offered in MEGA deals usually involve tax abatements on real or personal property, permit waivers, road improvements or municipal perquisites for company employees.

The incentives offered through MEGA packages total more than $3 billion since the beginning of the program. These incentives include state tax credits, local abatements and other state and local inducements, such as job training and road improvements. Graphic 4 shows the approximate value of all known incentives offered to recipients of MEGA deals by category.

According to MEGA Briefing Memos produced by the MEDC, the smallest local incentive in MEGA history appears to be a $28,000 break to Universal Forest Products in 2002 (though it is possible that a smaller incentive was offered that was not discernible in the MEDC documents obtained by the authors).[28] The largest local incentive was $165 million over 25 years to General Motors Corp. in June 2000.[29]

General Motors Corp. has been the direct beneficiary of six MEGA deals, by far the most of any corporation.[30] Additional MEGA deals have been concluded with GM suppliers as part of an overall package benefiting GM. For instance, CMI‑Schneible Co., Machining Enterprises Inc. and Michigan Production Machining Inc. have all received MEGA deals. The MEGA credits and other incentives offered to these companies were all designed to support the "General Motors Nodular Iron Redevelopment Project" in Saginaw.[31]

Assumptions

While calculations about jobs creation are, in theory, straightforward, they depend on assumptions that may differ. MEDC has not provided all of the clarifications we had originally sought about the basis of some of the projected MEGA jobs figures,[32] so we adopted two key assumptions: first, that all predictions of direct job creation by MEGA corporations by a certain year (1999, for example) meant the jobs would exist at midnight on Dec. 31 of the previous year (1998); second, that this previous year roughly corresponded to the tax year listed on the "MEGA Credits" spreadsheet. Changing the methodology would change the precise totals, though probably with no significant impact on the findings.[33]

Another issue that must be decided in reviewing MEGA’s performance involves distinguishing between "direct" and "indirect" jobs purportedly created by the program. The MEDC defines "direct jobs" attributable to a MEGA package as the increase in the number of jobs at the specific firm sites that are the subject of the MEGA package. It defines "indirect jobs" as those jobs that are created outside the specific MEGA business sites following the MEGA-related investment and direct employment.

We have chosen to work primarily with direct job counts in this study. Estimating indirect job counts is a subjective exercise, and econometricians and accountants with the best of intentions can produce widely varying figures, depending on their assumptions and estimation techniques. In addition, the indirect job totals implicitly claimed by state officials in recent press commentaries are, at best, rule-of-thumb estimates, and they appear to be unreliable, as we will detail below.[34] Thus, when we do discuss indirect job counts (also known as "spin-off" jobs), we will say so specifically.

Another key issue in evaluating MEGA’s track record on jobs is captured by the remarks of David Hollister, Director of the former Michigan Department of Consumer and Industry Services, in discussing MEGA’s job program:

There is usually a lag time of several years between MEGA board approval of a project and reporting of jobs created. Many of these projects involve the construction of new plants and facilities, which can take several years. Therefore the number of jobs created by MEGA-aided projects … is only a fraction of the actual number of jobs that MEGA will eventually help to stimulate. … MEGA has been in existence for less than eight years, (so) we are just beginning to see the benefits of credits granted early on.[35]

It is true that economic and financial investments can involve lag time. Thus, it is necessary to factor in the delays projected by MEGA officials in each specific tax credit package, and we have done so in our calculations in the following section. We do not assume, however, that time lags can effectively be infinite.

Finally, we would note here that we have kept track of MEDC incentives differently than MEDC officials do. MEGA officials often remove data from their "All MEGA Projects" spreadsheet for deals that fail early on, and MEGA then subtracts from the spreadsheet the amount of the incentives originally offered to those firms. We have maintained this data, so we often report different and higher MEGA incentive totals.

MEGA Job and Project Performance

Based on state documents compiled since 1995,[36] we estimate that 127 of MEGA’s agreements should have produced fully employed facilities through 2004. (For a discussion of the assumptions we employed in calculating this number, see "Appendix C: Determining MEGA’s Job Counts.") Of these 127, about 56, or 44 percent, have claimed credits under the program.

The ability to claim credits does not mean, however, that a firm has achieved the job goals that it projected in its MEGA agreement. For instance, for most MEGA deals, a company must create an initial 75 "qualified new jobs," usually within a year of commencing operations a particular site.[37] If it does reach this minimum job threshold, it can begin claiming its tax credits, even if it never achieves the job count it originally projected.

Many of the 56 cases in which tax credits were claimed did not fully meet original projections. In fact, only 10 of the 56 can be shown to have created the number of direct jobs originally projected within the expected time frame — although three of the 10 (Kmart, for instance) have had setbacks following their initial success in meeting the targets (see "Appendix C: Determining MEGA’s Job Counts").

According to MEDC figures, MEGA originally projected that 35,821 direct jobs would be created at MEGA companies by the 127 MEGA deals that were supposed to be fully operational by 2005.[38] Based on a MEGA document obtained in December 2004, about 13,541 jobs exist at those companies, or roughly 38 percent of what was originally hoped for. Given this figure, MEGA’s direct job total represented about 0.3 percent of Michigan’s 2004 workforce (see Graphic 5a by clicking on the hyperlink "More Images...," which appears beneath Graphic 4 above).[39]

This finding, we note, is similar to an independent estimate made by The Detroit News in 2003.[40] The News used state documents similar to those employed in this study and calculated that 10,787 direct jobs had been created at authority-aided projects."

Our direct job figure of 13,541 is admittedly lower than the job estimate MEGA officials have sometimes cited. For example, in a November 2004 commentary in Business Direct Weekly, MEDC Chief Executive Officer Donald Jakeway claimed, "Of the MEGA projects that have collected SBT credits for their projects to date, 28,812 total jobs have been created at an actual SBT credit cost of $75.1 million."[41]

According to the MEDC’s "MEGA Credits" spreadsheet, however, the $75.1 million in MEGA SBT credits referred to in the commentary actually created 13,541 direct jobs.[42] Our exchanges with MEGA over the discrepancy eventually indicated that the additional 15,271 jobs are MEGA’s estimate of the indirect jobs created by these MEGA projects.[43] As a result of additional inquiries in the ensuing three months, we received the following explanation of how the indirect jobs figure was calculated:

The MEDC staff member [who produced the total jobs number] figured the proportion of indirect to direct jobs project[ed] and applied that proportion (approximately 1.1 to 1) to the number of actual jobs (13,541) that had been reported to us up to that point in time. The number of actual new indirect jobs was thus estimated to be approximately 14,709, for total actual new direct and indirect jobs of a little more than 28,000.[44]

Thus, MEGA officials have used a ratio to estimate the number of indirect jobs created by existing MEGA projects. An MEDC spokesman notes that this calculation is based on projected job estimates produced by an economic modeling software program known as REMI (Regional Economic Modeling Inc.),[45] and that MEDC officials "trust the statistical model used in the widely used REMI analyses to provide a good estimate that helps us determine the economic value of a proposed new facility or expansion."

While we respect the power of the REMI model, we would note that the method described above was developed by an MEDC official, not the professional REMI modelers on contract with the state. Further, we would add that this method of estimating existing indirect job totals is unreliable for at least four reasons.

First, the MEDC starts with 13,541 existing direct jobs and applies to all of them a constant ratio (of indirect jobs to direct jobs). But this ratio would not be constant; rather, it would vary for each of the 56 projects that produced the 13,541 jobs.[46] Indeed, one key reason for employing the REMI model is to determine what the indirect job creation rate will be for each project, since spin-off job creation can vary in complex ways.

Second, the constant ratio that the MEDC employs is based on projected direct and indirect job creation for all of MEGA’s projects. In many of these cases, however, the MEGA-related investments and job creation will happen many years from now, well past 2005.[47] Many of the assumptions made about the creation of these future jobs are not valid for job creation during the past 10 years — the very interval for which the projection of 28,812 jobs was made.[48]

Third, even if the ratio of indirect jobs to direct jobs were constant and based on relevant figures, the 14,709 indirect jobs calculated by the MEDC would necessarily overstate the number of indirect jobs that have been created. In REMI models, indirect job projections do not stop once the direct jobs have been created. Instead, the model assumes that indirect jobs will continue to be generated for years into the future. Thus, the indirect jobs estimate calculated by the MEDC method will inevitably include some jobs that have not yet come into existence. Unfortunately, the public claim of 28,812 jobs created implies that all of these jobs already exist.

Fourth, the jobs claim output of the REMI model is based on a series of assumptions (such as estimates of direct job creation) that we know in retrospect to be false. This observation is no criticism of the REMI model or of those who use it; assumptions of this kind are always necessary in economic modeling, and they are often seen to be inaccurate in hindsight. Nevertheless, any current determination of MEGA’s indirect job creation should acknowledge that these projections and any ratio based on them are no longer sound. The MEDC’s method does not do this.

As a result of these and other concerns about estimating MEGA’s indirect job figures, we have not used the 28,812 job total in our analysis. Nevertheless, we show in Graphic 5b what MEGA’s job contributions to state employment would represent if the 28,812 figure were correct (view Graphic 5b by clicking on the hyperlink "More Images...," which appears beneath Graphic 4 above).

We would note that the performance figures we have calculated for MEGA’s projects are consistent with reports that the MEDC sends to the state Treasury each year. These reports include tallies of the size of the SBT credits that are projected to be claimed under MEGA agreements that year, and the Michigan Treasury in turn reports and revises these numbers periodically.[49]

Based on state Treasury figures, between 1996 and 2004, MEGA originally estimated that more than $220 million in SBT credits would be redeemed as a result of the MEGA program. (Graphic 6 shows the year-by-year tax credit claims projected for the MEGA program; the graphic can be viewed by clicking on the hyperlink "More Images...," which appears beneath Graphic 4 above.) As mentioned earlier, however, credits of just $75 million have been claimed,[50] or about 34 percent of the amount originally expected.

According to the State of Michigan’s "Executive Budget Appendix on Tax Credits, Deductions, and Exemptions Fiscal Year" documents, MEGA officials expect foregone SBT revenue to total only $9.7 million in 2005,[51] down from $37 million in 2004[52] and from an all-time high of $57 million in 2002.

These anticipated drops in annual SBT revenue effectively represent expected drops in the employment totals of MEGA businesses. If MEGA were meeting its original job creation projections, the size of the claims of annual SBT tax credits would be rising, not dropping, as more MEGA companies brought their new or expanded facilities online.

Case Studies

Three Major News Events

One of the purported benefits of an economic development program like MEGA is the positive publicity about the state’s business climate that can follow the success of a MEGA project. We therefore reviewed in greater depth several MEGA packages that provided the potential for significant job creation under well-publicized agreements with well-known firms.

The MEGA agreements described immediately below were concluded in 2000, 1996 and 1999 respectively. State government press releases described them as follows:

In further promotion of the MEGA agreements, former MEDC President Doug Rothwell told Site Selection magazine that Webvan, the subject of the third news release, was "one of the best-financed retailers on the market for the next wave of e-retailing."[56]

Seven companies are included in the MEGA packages described in these press releases: Altair Engineering, Case Systems,[57] Delphi Automotive Systems, LDM Technologies, National TechTeam, Shape Corp. and Webvan. Of the 5,249 projected jobs described in the news releases above, 3,455 were direct jobs. All of these direct jobs were to have been created by 2005 at the seven companies involved.

According to the official "MEGA Credits" spreadsheet received by the authors in December 2004 (and on which the figures in this study are generally based), four of the seven companies have not claimed the tax credits they would have been entitled to if they created the jobs stipulated in their MEGA agreement. One of these four, Webvan, went bankrupt, losing most of its value in the 12 months after its MEGA deal had been approved.[58]

Of the three companies that have received credits — Shape Corp., National Tech Team and Case System — none directly created the number of jobs that were forecast in the time frame expected. National Tech Team qualified for about $180,000 worth of MEGA credit through 1998 before stumbling and temporarily losing access to credits.

Thus, as of December 2004, these seven companies appeared to have created a total of 514 direct jobs through tax year 2003 — or about 15 percent of what state officials had said would be created.[59]

In fairness to MEGA and the companies involved, MEGA’s February data, received shortly before this study’s publication date, indicate a somewhat better result. Two of the seven companies have improved their job performance. National Tech Team has received MEGA credits for tax years 1999 through 2003, and in 2003, the company’s employment stood at 115 at the facility for which it received the MEGA package. Also, Delphi Automotive was awarded tax credits for 600 jobs created at its facilities in 2002 and 2003.

Including this new information about National Tech Team and Delphi raises the jobs total for all seven companies mentioned in the three news releases to 1,229. This represents about 36 percent of the total jobs that were projected originally.

The February data shows that MEGA’s job figures can improve with time. Still, it is worth noting that these figures can decline again, as well. For instance, according to published reports, Delphi Corp. is expecting losses of $350 million in 2005, and the company’s stock has tumbled from $17 in February 1999 to a low of $4.15 in late March 2005.[60]

Kmart Corp.

Kmart was twice awarded MEGA deals by the state of Michigan. The total value of these two deals, including MEGA’s state tax credits and local incentives, exceeded $34 million.[61]

The first MEGA deal for Kmart occurred in May 1998 and included an offer of MEGA state tax credits valued at as much as $14.3 million in total over 20 years; job training subsidies worth as much as $297,500; and a local commitment from Troy worth $450,000 in "public improvements" and other favors.[62] The second deal was approved in August 2000, less than 17 months before the corporation declared bankruptcy.[63] Its MEGA credit was worth as much as $15.9 million in total over 14 years; job training subsidies of up to $450,000; and local infrastructure assistance of $2.6 million to "add a third lane to Kmart’s entrance and … improve traffic flow to and from the project site."[64]

In exchange for these incentives, Kmart promised not to let its base employment levels drop below 3,637 in the 1998 deal[65] and 4,084 in the 2000 deal.[66] By February 2003, however, employment levels had dropped to about 3,500, which was below the conditions of both MEGA agreements. A November 2004 Detroit News article suggested that the job count is now as low as 2,000;[67] another Detroit News report indicated that Kmart Corp. was tentatively offered a third package of incentives estimated to be worth at least $40 million if it promised to maintain just 1,500 jobs in the state.[68]

Given Kmart’s declining job numbers, the firm was unable to claim all of the credits it was originally eligible for under its MEGA agreements. Nevertheless, before Kmart’s new jobs disappeared, it did receive $6.1 million[69] in state tax relief, as well as job training and road improvements.

Covisint Inc.

Covisint was born in December 2000, the child of several automotive companies, including Ford Motor Co., DaimlerChrysler AG, General Motors Corp., Renault SA and Nissan Motor Company Ltd.[70] The firm was operating out of Southfield, but apparently had not settled on a permanent headquarters. Covisint was going to be an online automotive supply electronic auction site.

Industry experts and others had high hopes for Covisint, and the company was expected by some to broker more than $300 billion[71] in annual sales, while producing $5 billion in annual revenue for the company.[72] Officials from other states, such as Georgia, were wooing the company in hope of landing Covisint’s new headquarters.

Official "Meeting Minutes" of the MEGA board indicate that MEGA officials thought that by 2021, the Covisint project would bring 1,000 direct new jobs and 966 indirect new jobs statewide.[73] As part of its deal the firm needed only to maintain a base employment staff of 169.[74] In April 2001, Covisint announced that it had chosen Michigan for its permanent headquarters.

Unfortunately, by the end of 2002 Covisint was struggling due to unforeseen challenges, such as competition from other business-to-business auction sites, and the fear of suppliers that fake auctions were posted on the site in order to get a glimpse at what tier-two suppliers might offer.[75] Less than three years after it received its MEGA deal, Covisint’s prospects had plummeted, and its approximate value in 2003 was $25 million.[76] By October 2004, parts of the company were reportedly sold to FreeMarkets, an auction site, and Compuware Corp. (the latter portion for about $7 million).[77]

As of Jan. 2005, total employment at Covisint (under Compuware) stands at 122.[78] We have found no evidence that the firm met its job creation goals and or claimed its MEGA credits.

Other Examples

These are not the only cases where widely publicized MEGA projections did not come to pass.[79] With Aspen Bay, for instance, MEGA officials offered nearly $22 million in MEGA credits and other incentives for construction of a new pulp plant, certifying that the company was "financially sound and that its plans for the expansion or location are economically sound." But the company was unable to find private financing for construction of the plant after it had received approval of its MEGA package.[80]

Of course, MEGA has picked some winners, as well. Shape Corp., one of the seven companies mentioned above under "Three Major News Events," has apparently prospered. While it’s true that the company failed to achieve the original projection of 400 new direct jobs by 1999, by 2003 it had created 462, exceeding their expected job creation total by 62.

Similarly, Lacks and Quicken Loans have managed to meet and exceed their expected job output (by 56 and 193 jobs, respectively). Magnesium Products, Meridian and Robert Bosch could also be seen as MEGA investments that have done well so far (though Robert Bosch has stumbled recently).[81]

Still, MEGA’s success rate, as we found earlier in "MEGA Job and Project Performance," is not very high. The cases above indicate that MEGA’s miscalls have included some of the better known projects that might have sent positive signals about Michigan’s business climate if they had proved successful.

Michigan’s Economic Climate Under MEGA

MEGA’s broader goal in stimulating job development is to improve Michigan’s economy. Michigan’s broader economic record since 1995, however, has not provided clear evidence of the program’s success.

From December 1995 through December 2004, Michigan finished 50th out of 50 states in percentage employment growth.[82] Even focusing only on private-sector employment growth from December 1995 to December 2004 (thereby excluding public sector employment which MEGA does not directly affect), Michigan placed 50th in the nation.[83] (Michigan ranked 50th in the same category from 2000 to 2003.)[84]

Other economic measures seemed little better. From 1993 to 1997, Michigan’s percentage increase in per-capita gross state product was 18th in the nation, but from 1998 to 2003, it had fallen to 44th (a discontinuity in the methodology of this federal metric between 1997 and 1998 necessitates this temporal division of the data).[85] From 1995 to 2003 (the most recent data available), Michigan’s per-capita personal income growth was 43rd in the United States.[86]

Nor have Michigan’s recent job figures been encouraging. In December 2004, Michigan’s unemployment rate was 7.3 percent, tied with Alaska for the worst in the nation.[87] Michigan and Ohio were the only two states to lose jobs in 2004, and unlike Ohio, Michigan lost a significant number — 46,500, as opposed to Ohio’s 200, according to the U.S. Department of Labor.[88]

A January 2005 United Van Lines study further suggests that Michigan is experiencing a net emigration.[89] The company’s annual survey of moving figures found that in 2004, Michigan was one of only 11 states in the continental United States that qualified as "high outbound" — i.e., a state in which more than 55 percent of the moves handled by United represented an exit, rather than an entrance. Michigan’s outbound traffic was 61 percent of its total, the highest percentage in the Great Lakes State since 1982.

Summary of Findings

The evidence suggests that the MEGA program has fallen well short of its stated goals on several levels.

As noted earlier, about 44 percent of its eligible projects have claimed tax credits since the authority’s inception. In only 10 cases — about 8 percent of the total — did MEGA projects achieve their estimated job totals on schedule.

At the same time, direct job creation in the MEGA program appears to have lagged, reaching only 38 percent of MEGA’s original projections. This 38 percent represents 13,541 jobs, or about 0.3 percent of Michigan’s overall job count. MEGA’s underperformance in job creation is mirrored by the finding that only one-third of the dollar value of the originally expected SBT tax credits granted has actually been claimed, and by the fact that the projected rate at which these credits are expected to be claimed has dropped in recent years.

Direct job figures do not account for all of the jobs that can be attributed to MEGA packages; indirect jobs have probably been created, as well. Still, the low success rate in MEGA’s direct job creation suggests a similarly low success rate for indirect job growth, since spin-off job growth is driven in part by the activities of employees in the jobs created directly.

The case studies we discussed also suggest that there are two sides to the issue of the publicity generated by MEGA deals. While successes in the case studies described above possibly could have encouraged other businesses to consider new investment in Michigan (at least with the aid of a MEGA package), the failure of MEGA’s deals could likewise send the signal that Michigan is not a good place to do business. If firms cannot create jobs even when they are offered tax credits and other state and local incentives, the implicit public message about the state’s business climate is probably negative.

Another interesting observation arises from the case studies. State officials often justify the granting of tax incentives by noting that a MEGA recipient must achieve its job goals in order to actually receive its MEGA credits; if the company fails, the state grants no credits and forgoes no revenue. The Kmart deal, however, shows a wrinkle in that view: Kmart received $6.1 million[90] in state tax relief for temporarily creating jobs that now no longer exist. It was also offered subsidies to train workers that may no longer be employed at the corporation, and it obtained infrastructure improvements to widen roads that probably won’t have the projected traffic. There was a cost to MEGA’s investment in Kmart, and it is not obvious that this cost was worth the temporary jobs that were promoted by the plan.

Moreover, even in cases where a firm never manages to receive state tax credits, it often receives the local incentives anyway. (R.J. Tower in Delta Township is one example of this dynamic, having begun to collect a local property tax abatement, even though the firm’s poor jobs record means it has not claimed MEGA SBT credits.) This fact, together with observations in later sections of the study (including "The Problem of Ensuring MEGA Credits Are Necessary") suggests that MEGA is not as "cost-free" as it is sometimes described.

Michigan’s economy has not shown obvious signs of strength in response to 10 years of MEGA investment. In fact, all major indicators suggest slow growth, including state employment growth. It would seem that MEGA’s 127 projects should have been able to influence the state’s economic growth during this period if the assumption on which the program is based were sound.

Of course, it is conceivable that Michigan’s jobs and economic performance during these years would have been worse without the MEGA program. We thus undertook a more detailed econometric investigation in order to determine whether MEGA might have buffered the state (and its counties) during an economic downturn. This investigation appears in the next section of the study, "Econometric Evaluation of MEGA’s Effectiveness."

Analysis of the role of tax policy on economic growth enjoys an extensive treatment by economists. A 1997 Federal Reserve Bank review of research findings cited over 90 studies that evaluated the role of fiscal policy in economic growth in the United States (see, for example, the research of Michael Wasylenko in the New England Economic Review).[91] If anything, the past few years have seen an acceleration of this analysis accompanied by the development and widespread application of more robust statistical techniques that enable analysts to evaluate impacts.

Many of these papers attempt to explain differences in growth, wages and industrial composition through analysis of interstate tax policy. An equally large number of studies also evaluate whether expenditures (as evidenced by infrastructure) influence growth (see, for instance, the research of William Fox and Sanela Porca in 2002).

A considerably smaller number of studies have attempted to evaluate the influence of individual targeted tax policies on economic growth. A number of these have been reviewed in a study in 2002 by Timothy Bartik, senior economist at the Upjohn Institute and co-editor of Economic Development Quarterly, a scholarly journal on economic revitalization.

Despite extensive analysis of fiscal incentives in general, the literature does not yet suggest a consensus on their impact on local economic conditions. Many studies find no impact on some important policy variables (e.g. income, employment) while those that do find impacts report rather modest taxation elasticities on growth, in the range of ‑0.1 to ‑0.4.[92] These figures mean that for every 1 percent decrease in taxes, we would see between a 0.1 percent and 0.4 percent increase in economic activity.

Scholarship on business tax incentive programs is mixed, but generally negative as to the impact of government economic development efforts to create jobs and additional wealth or other announced economic goals of these programs. For instance, Todd Gabe of the University of Maine and David Kraybill of The Ohio State University examined state economic development incentives on 366 Ohio manufacturing and nonmanufacturing establishments that began large expansions between 1993 and 1995. They found empirical evidence to suggest that the incentives offered these firms had little if any actual impact on expected employment growth. The small impact that was seen suggested a slightly negative effect on actual growth.[93]

In a February 2001 review of more than 300 scholarly papers on economic development programs, Terry Buss, then a professor of public management at Suffolk University in Boston, found that "studies of specific taxes are split over whether incentives are effective, although most report negative results."[94]

These findings of questionable and even negative economic impact would not surprise many scholars. In their 2004 paper "The Failures of Economic Development Incentives," University of Iowa economists Peter Fisher and Alan Peters explain the findings of their metareview of academic literature. (A metareview is simply a review and summation of many literature reviews; literature reviews are themselves summations of the research of fellow scholars on particular subjects.)

Fisher and Peters examined three questions surrounding government business development programs. First, do incentives improve growth and development where offered more than would occur on its own? Second, is this development directed to low-income populations? Third, they ask, "How costly to government is the provision of these incentives compared to alternative policies?"[95]

Their conclusion was also mixed, as are many literature reviews, but on balance Fisher and Peters surmise that these programs are either ineffective or carry costs that exceed the alleged benefits derived from them. As to their first question, they conclude that:

The upshot of all of this is that on this most basic question of all — whether incentives induce significant new investment or jobs — we simply do not know the answer. Since these programs probably cost state and local governments about $40-$50 billion a year, one would expect some clear and undisputed evidence of their success. This is not the case. In fact, there are very good reasons — theoretical, empirical and practical — to believe that economic development incentives have little or no impact on firm location and investment decisions.[96]

The two economists think there may still be a role for government to play in economic development, but it should focus more on the fundamentals, such as infrastructure and education, as well as worker training. That said, Fisher and Peters conclude: "(T)he most fundamental problem is that many public officials appear to believe that they can influence the course of their state economies through incentives and subsidies to a degree far beyond anything supported by even the most optimistic evidence."[97]

In addition to the presence of a range of findings in the literature, policy recommendations are further challenged by the absence of findings extrapolated to a benefit-cost framework. Even if a robust econometric finding of a positive impact of targeted fiscal incentives were to occur, it would not necessarily translate into a clear policy recommendation in favor of such incentives. For instance, if a study of a state or region concluded that there were a statistically significant link between targeted tax incentives and new jobs, the tax incentives might still be bad policy if each new entry-level job was purchased at the cost of a million dollar state tax investment.

Further, as mentioned earlier, evaluation of targeted incentives on local economic activity has been more sporadic than analysis of general fiscal policy. Also, the analytical methods employed by state economic development agencies are better suited to managing programs than to evaluating economic growth. In particular, the use of firm-specific reports of gross job flows may be a useful management tool, but it is particularly ill-suited to economic analysis. Thus, a review of findings regarding targeted tax incentives will leave an unbiased reader hungry for more substantive analysis.

Timothy Bartik’s 2002 study[98] provides an admirable survey of methods for evaluating targeted incentive policies. The estimation provided in this study is a direct result of Bartik’s recommendations and conforms to the multiple methods of econometric estimation reviewed in his paper.

Before we review our model, there are some additional considerations that direct the research.

First, a major challenge in many of the fiscal incentive studies is the holistic treatment of state fiscal policy. Clearly, firms and individuals both respond to incentives in choosing their place of residence through both taxes and amenities. The latter of these two variables includes government expenditures on such things as parks, roads and police. An econometric comparison of regions that does not account for the fullness of tax policy differences runs the great risk of misestimating the role a particular incentive plays.

For example, in a nationwide study of targeted tax incentives, any analysis that does not estimate effective tax rates (distinct from the targeted incentive policy) will not properly specify the causative relationship between taxes and firm location decision. A similar argument regarding infrastructure may be offered. Thus international or interstate studies of fiscal policy impacts will necessarily require a comprehensive estimate of tax burdens — not simply expenditures or credits in a targeted incentive program.[99] Fortunately, the intrastate study we conduct here largely avoids this concern, since the bulk of fiscal differences will occur at the state, not local, level.

In addition to fiscal considerations, a number of studies have cast doubt upon the magnitude of the regional economic impact of large firms, which are the most likely to receive fiscal incentives. These studies include papers published in 2004 by Kelly Edmiston,[100] William Fox and Mathew Murray[101] and Michael Hicks.[102]

Edmiston finds that the impact of new large firms is almost always overstated, with multipliers often less than one. He further finds that expansion of existing firms generates substantial effects. Fox and Murray test the local impacts of large firm relocation, finding no significant net impacts in the communities in which the firms locate. Using a quasi-experimental approach, Hicks finds that large gambling and wholesale-retail facilities locating generate no net employment or income gains in the counties in which they locate. In these studies it is not only the effectiveness, but the very potential for effectiveness — the "efficacy" — of targeted business incentives that are cast into doubt.

In evaluating the impact of the MEGA program, this analysis is aided by the fact that only the state of Michigan will be investigated. While Michigan is one of the most geographically difficult U.S. states to model (due to the physical split between the upper and lower peninsulas), the commonality of the federal and state tax instruments suggests that a relatively simple model may be effectively employed to test the impact of the MEGA credits upon the state’s economic growth, incomes and employment.

The analysis presented below will evaluate a rather limited, but important question: Did the MEGA credits influence either aggregate or business-sector growth in Michigan’s counties through 2002? Since this study is confined to a single state, the overall fiscal condition of the state is not analyzed. This makes the analysis more limited, but more tractable in scope. It also offers the potential for results to change if overall policy were to be modified. For example, our findings are conditioned upon the policies in place before and during the MEGA credit period. A change in labor market or fiscal policy in the coming years may render our findings inappropriate as a forecast. We can only speak to what has happened.

Other considerations beyond the scope of econometric analysis matter. For example, any targeted incentive will inevitably treat firms differently. There is a considerable potential range of noneconomic impacts that can result from a policy that permits elected officials to distribute public funds to individual firms. In the upcoming analysis, we can only estimate whether the MEGA credits have changed Michigan’s economic landscape, not whether they are an appropriate policy, even if they do improve incomes and employment. Such concerns are discussed elsewhere in this report.

In order to assess the impact of the MEGA Credits, we have constructed an econometric model of the type recommended by Bartik (2002) as an advanced statistical measure of economic development credits. The full technical details and modeling considerations are contained in "Appendix A: The Model of MEGA’s Economic Impacts" and have been subject to peer review. Here, we briefly summarize the method.

Econometric analysis of each of Michigan’s counties from 1990 through 2002 provides a basis for assessing whether or not the MEGA credits actually influenced economic activity, either in aggregate, or within specific industries. The time period was selected to allow five years of modeling of Michigan’s economy prior to the implementation of MEGA. We extend our analysis to 2002, since it is the most recent year for which county-level data on income and employment have been published by the Bureau of Economic Analysis at the U.S. Department of Commerce and the Bureau of Labor Statistics at the U.S. Department of Labor. This allowed us to investigate the impact of the first seven years of the program.

We are most interested in changes to income, employment and the unemployment rate in counties where firms received specific MEGA credits. The econometric method we use in this effort is designed specifically to account for the impact of MEGA credits.

As we selected the model, we were aware of the problem of identifying the actual MEGA credit amount and date of impact. Also, we are aware that despite the selection criterion, some attempt to target more distressed areas may also influence the decision to offer a firm a MEGA credit. Further, we are aware that the impact of surrounding counties or regions and regional trends may influence the impact of the MEGA credits, or more generally economic growth as measured by incomes and employment. Each of these characteristics of the MEGA credit program were considered and empirically tested when we chose both the type of model and its specific form. Again, the details of the model are contained in Appendix A.

It was not possible to directly test the disaggregated impact of the MEGA credits to either high technology firms or offices, since there is no data series that treat either offices or high technology activities differently from other firms within their respective industries. Thus, we tested aggregate incomes and employment impacts in three major sectors potentially affected by MEGA: manufacturing, wholesale and construction.[103]

We were able to test the aggregate impact of these MEGA credits. The major strength of our model is that it evaluates what actually occurred, not what was hypothesized to occur, subsequent to the awarding of a MEGA credit.

County-Level Results

Our first tests were on the impact of county-level employment, incomes and the unemployment rate during the period 1990-2002. Our model worked very well, proving sufficiently flexible to accommodate the data that we have available and performing similarly to a number of other regional growth models.

In the case of county-level changes to per-capita income, employment and the unemployment rate, the impact of MEGA credits is unambiguously nonpositive. County-level changes to these economic measures range from zero (the most common result) to modestly negative. The results clearly and strongly suggest that, as a charitable interpretation, in aggregate, the MEGA credits have been unsuccessful in improving per-capita income, employment and the unemployment rate.

Two objections could be raised in response to these results. One is that the data end in 2002, while the local impacts may require a longer period to materialize.

It is true that the lag in local impact could be large. Still, the data would reflect the impact of MEGA credits implemented in 1995, and these have not produced a net positive impact on county-level employment or incomes. If the failure to detect an economic impact is due to a lag, the lag is at least seven years.

A second issue is the period being studied, which included periods of recession and a weak economy. Some might wonder if MEGA might have prevented local economic conditions from being worse, even if it didn’t produce the intended economic growth.

This does not appear to have happened. The many Michigan counties whose companies did not receive MEGA credits fared no worse than the counties whose businesses did receive MEGA credits. The evidence clearly suggests no benefit to a Michigan county from a private facility in that county receiving MEGA incentives.[104]

State-Level Results

The failure of MEGA credits at the county level has an important corollary: The state of Michigan as a whole has not received an economic benefit in per-capita income, employment or the unemployment rate from the MEGA program.[105]

Business-Sector Results: Manufacturing, Warehousing and Construction

It is possible that MEGA credits fail to improve economic growth, but nevertheless shift economic activity between business sectors. We therefore investigated, as mentioned earlier, the impact of MEGA credits on wages and employment in three different business sectors: the industrial sectors of manufacturing and warehousing activities, and the construction industry.

With manufacturing and warehousing activities, there were no impacts from MEGA credits on employment that came close to being economically or statistically significant. There was similarly no statistically significant impact on warehousing-related wages. In contrast, there was a statistically significant reduction in manufacturing wages, but it was so small as to be economically insignificant.

Only when we assessed the impact of the MEGA credit on construction employment in a county did we find that under certain circumstances MEGA credits had an impact. This impact was positive: One new construction job was created for each $123,000 in MEGA credits approved in a county.

Unsurprisingly, however, these jobs were temporary, and we found that 75 percent of the net MEGA credit impact on construction employment disappeared in the first year the project started, and the full net increase in construction employment was gone by the end of the second year. The new jobs also carried lower wages than those already in existence — although, as with the decline in manufacturing wages, the resulting decline in average construction wages was so small as to be virtually economically meaningless. (Specifically, for each $1,000,000 MEGA credit, the average construction worker sees his total annual wages drop by less than 25 cents.). Finally, we would add that even the interpretation of construction job growth should be made with caution, as the model’s estimates did not generate typical levels of statistical significance.

The transience of the construction jobs is consistent with most findings of construction employment dynamics. The findings are also consistent with the economic challenges in Michigan for significant portions of the period being analyzed. Recessions reduce wages, and the lower wages were likely the product of a reduction in hours worked (a common business cycle result).

Other findings from the model involving variables other than the MEGA credits are discussed briefly in Appendix A. The results relevant to MEGA, however, appear above, and they clearly indicate that the MEGA credit program has failed to increase either employment or incomes, although it has shifted business activity towards the creation of some temporary construction jobs.[106]

Our empirical analysis of MEGA credits from the beginning of the program through 2002 suggests that the largest impact of MEGA credits was a transient increase in construction employment that lasted about two years. This increase represented a shift in economic activity toward construction, with the cost per new construction job being approximately $123,000 in MEGA credits (plus MEGA program costs and other opportunity costs).[107]

The analysis suggests no net economic benefit to the counties that hosted firms receiving MEGA grants. MEGA credits had no effect on a county’s per-capita income, employment and unemployment rate. Similarly, the MEGA credits had no measurable impact on the state’s per-capita income, employment and unemployment rate.

To a casual observer, the findings of the study so far might be hard to understand. MEGA may strike many people as a program that should work. After all, the State of Michigan has invested a great deal of financial and human capital in the authority. Moreover, MEGA is not an unusual program; other states have instituted similar authorities and regularly deploy them in an attempt to lure new business investment.

Yet a review of MEGA’s track record is not encouraging, with many of its results falling far short of initial projections. And while scholarly findings do not flatly deny the possibility of the effectiveness of tax incentive programs like MEGA, neither do they encourage hope that programs like MEGA will have a significant economic impact.