Social Security is going bankrupt, threatening the financial security of Michigan citizens. Retiring Baby Boomers are estimated to double the number of retirees in America by 2015, when Social Security will no longer collect enough in taxes to pay the benefits promised to recipients.

Privatizing Social Security-allowing individuals to privately invest their own retirement savings-can avert the financial crisis. Countries including Chile and Great Britain have privatized all or part of their state pension programs, yielding retiree benefits much higher than the government systems, including Social Security's paltry 2.2 percent annual rate of return.

This study recommends that the Michigan Legislature call on Congress to either privatize Social Security or allow Michigan to design for its citizens a sounder and more beneficial retirement plan.

On August 14, 1935, President Franklin Roosevelt signed the Social Security Act into law, declaring it to be "a law that will take care of human needs and at the same time provide for the United States an economic structure of vastly greater soundness."

Today, politicians and citizens alike are discovering that the government-funded retirement system begun by Roosevelt is not only financially unsound, but is increasingly incapable of meeting the human needs of America’s growing elderly population.

Many Americans believe that their Social Security taxes go into an account from which they will draw when they retire. In reality, Social Security is a "pay-as-you-go" system whereby taxes on current workers are directly transferred to current retirees in the form of benefits. This system worked when there were 16 taxpaying workers to support each individual retiree. Today, however, the ratio of workers to retirees has fallen to 3-to-1 and is expected to drop to 2-to-1 by 2030.

In addition, the Social Security Trust Fund will begin paying out more money than it takes in as early as 2015, when the wave of retiring Baby Boomers is expected to double the number of retirees drawing Social Security checks.

These facts mean that the current Social Security system can be maintained only if benefits to the growing ranks of elderly retirees are slashed dramatically or payroll taxes are raised to confiscatory and immoral levels on younger workers. Fortunately, there is a third alternative to dealing with the looming Social Security crisis: opting out of the system in favor of privatizing retirement planning.

The idea of privatization—allowing individuals to privately invest their own retirement savings—is not new. Countries including Chile, Great Britain, and Australia now allow workers to invest all or part of their payroll taxes privately, and the results have been impressive. Chilean retirees, for example, now enjoy three times the benefits that they would have received under the old government system.

Here in America, three Texas counties chose to leave the Social Security system in 1981 when Congress allowed state and local governments to opt out. The alternative private investment plan designed by the counties for their employees has also yielded greater returns and increased benefits for its participants.

More than 65 million Americans now choose to supplement their retirement nest eggs with private investment instruments such as Individual Retirement Accounts (IRAs) and employer-sponsored 401(k) and 403(b) plans that also outperform Social Security.

Social Security privatization would benefit all workers, especially the bottom 20 percent of wage earners who cannot afford to invest part of their paychecks and must rely mostly on Social Security for their retirement. Workers who were allowed to invest even 2 percent of their paychecks (as opposed to the 5.26 percent of their payroll taxes that go toward retirement) could earn instead 9 to 35 percent more than what they would receive from Social Security, depending on their income level.

A number of plans to privatize all or part of the Social Security system have been proposed, but one kind of "privatization" which involves having the federal government manage retirement fund investments should be avoided. Direct government investment in the stock market versus individual private investment would lead to unprecedented politicization of the American economy. "Politically incorrect" companies and their customers and stockholders would suffer as important market decisions were made by politicians and bureaucrats, not by workers and retirees, the people with the largest stake in the investment.

Critics of Social Security privatization suggest that private investment of retirement funds is too risky. They warn that market downturns could wipe out the nest eggs of workers who are ready to retire. But this fear is unsubstantiated. Although it is true that markets experience short-term fluctuations, retirement savings are invested over a lifetime. An analysis of the performance of stocks shows that since 1800, there has never been a 20-year period in American history when stocks produced a net loss in real terms.

In May 1997, the Oregon Legislature passed a resolution urging Congress to grant waivers to let states opt out of the federal Social Security system and design their own retirement plans for both private-sector and government employees. Since then, Colorado has adopted a similar measure and six other states—Arizona, Indiana, Missouri, New Hampshire, South Carolina, and Washington—are also considering opt-out proposals. The Michigan Legislature should adopt a resolution that asks Congress to either

Partially privatize the existing Social Security program by allowing workers to shift all or part of their current 5.26 Social Security retirement payroll taxes into privately owned and managed accounts up to the allowable limit of $10,000 per year; or

Grant the state of Michigan a waiver to opt out of the federal Social Security system and design a sounder and more beneficial retirement plan for its citizens.

Many countries have already increased millions of citizens’ retirement security by turning to private investment to restore fiscal soundness and improved benefits to their pension programs. With a strong economy and government surpluses forecast for the next decade, the United States is in a solid position to move to a privatized pension program that stimulates economic growth, promotes private savings, and restores individual freedom.

Michigan should join with Oregon and Colorado to demand that Congress take the correct course and privatize the Social Security system or allow states to opt out and design their own pension plans.

On August 14, 1935, President Franklin Roosevelt signed the Social Security Act into law, declaring it to be "a law that will take care of human needs and at the same time provide for the United States an economic structure of vastly greater soundness."

Today, 63 years later, there is a growing realization among politicians and citizens alike that the government-funded retirement system begun by Roosevelt is not only financially and actuarially unsound, but is increasingly incapable of meeting the human needs of America’s growing elderly population.

Social Security operates as a pay-as-you-go system, meaning that taxes collected from current workers are used to support current retirees. Because the ratio between workers and retirees is rapidly shrinking, payroll taxes will either have to be hiked dramatically or retirement benefits cut significantly in order to keep the system afloat in the future.

Of course, neither of these options is popular with Americans. But polls show that there is broad public recognition of the fact that the future of Social Security, as it exists now, is bleak. In 1975, 88 percent of Americans were "fairly sure they could count on Social Security for retirement." Today, that figure is under 46 percent and still dropping.

As public awareness of the problem increases, what was previously untouchable as a political issue has now moved to center stage with the president and both political parties wanting to "save" Social Security.

How did Social Security come to be in such a mess? The current problems are caused not only by the original design of the program but are also the result of major changes in society over the decades since it was enacted:

Lower birth rates have resulted in a dramatically smaller ratio of people to pay benefits for the ever rising number of retirees;

Longer life expectancies have boosted the costs of providing retirement assets as benefits are now paid for significantly longer periods of time;

Increasing numbers of people are retiring before becoming eligible for Social Security benefits at age 65 due to the accumulation of private retirement assets through Individual Retirement Accounts and employer-sponsored 401(k) and 403(b) savings plans; and

Shorter average life expectancies for lower-income workers mean they get less from Social Security than others who will live longer.

A quick review of history shows how we arrived at the current state of affairs.

When Social Security was created in 1935, the average life expectancy was under the retirement age of 65. This fact ensured that comparatively few people would receive Social Security benefits and so the payroll taxes to support them were low (two percent on an annual income of $3,000, or $60 per year).

Ida Fuller was the first person to receive Social Security benefits. She retired in 1940 after paying only $44 into the system, and by the time of her death in 1975 at age 100, she had received $21,000 in benefits. Her case shows the inherent unfairness of the pay-as-you-go nature of Social Security: A savings of $44 cannot possibly pay $21,000 in benefits over 35 years, so her benefits were actually paid by taxes collected from younger workers.

Ostensibly, a trust fund collects Social Security payroll taxes from employees and employers. In reality, however, the fund is used to pay benefits to current retirees. The money is not saved or invested for the retirement benefits of each contributor. The trust fund is simply an accounting fiction, not the equivalent of a private account owned by an individual which can be invested for the future. A big first step in building support for change is broad public understanding of the pay-as-you-go design of Social Security versus accounts owned by each person.

Since the 1940s, significant shifts in birth rates and life expectancies have occurred. At the outset of Social Security, there were 16 workers paying into the system for every retiree drawing benefits. Today, the ratio is three workers for every retiree and by 2030 the ratio will fall to two workers per Social Security beneficiary, according to government estimates. At the same time, retirees are living longer than ever (average life expectancy now exceeds 75): This fact is a key reason why greater retirement resources are needed for current and future retirees.

Over the past 60 years, Congress has raised Social Security payroll taxes repeatedly in an effort to keep the benefits flowing. The current tax rate of 6.2 percent for both the employer and employee is applied to wages up to $68,400 and marks an amazing 950 percent increase from the initial $60 per year paid to Social Security by employers and employees.

Of that 6.2 percent, 0.94 percent goes toward survivor benefits in the case of death and disability benefits for people unable to work. The remaining 5.26 percent is applied primarily toward retirement benefits for current retirees. An additional uncapped 1.45-percent payroll tax is also levied for Medicare, but this report’s focus is on Social Security retirement benefits only.

Today, the Social Security trust fund is theoretically in surplus and will continue to be until about 2015—"theoretically" because all excess money above what is needed to pay benefits to current retirees is immediately borrowed for other government spending.

The real crisis will begin after 2015, when Social Security benefit payments will exceed the amount of money workers pay into the system and large numbers of baby boomers begin to retire. Changes must be made now to keep the current system from going bankrupt and leaving today’s workers and tomorrow’s retirees both out in the cold.

The problem of Social Security’s looming bankruptcy is serious. A number of proposals for "saving" Social Security have been made, many of which argue that taxes must be raised sharply on younger workers or else benefits cut to retirees. But fortunately there is a positive alternative to higher taxes and decreased benefits: opting out.

The idea of allowing individuals to opt out of a mandatory state-funded pension system in favor of privately investing their own retirement funds is not new. In 1980, Chile became one of the first countries to allow its citizens to opt out of its failing government system. In 1981, before Congress made participation in Social Security wholly mandatory, three counties in Texas opted out to design their own retirement plan. And a record number of Americans, especially younger ones, are quietly opting out themselves by building their nest eggs with employer-provided 401(k) and 403(b) pension plans.

The success of these private alternatives to Social Security led Oregon in 1997 to become the first state to pass a resolution calling on Congress to grant individual states waivers to opt out of Social Security and explore alternative pension plans. Colorado passed a similar measure in May 1998, and six other states, including Arizona, Indiana, Missouri, New Hampshire, South Carolina, and Washington, are also considering opt-out measures.

How successful have these private alternative plans been? What follows is a brief analysis of how these plans have performed or are likely to perform as well as recommendations for how Michigan can take positive steps to protect its workers and retirees from the coming Social Security crisis.

More than 65 million Americans now choose to supplement their retirement nest eggs through investing in Individual Retirement Accounts (IRAs) and employer-sponsored 401(k) and 403(b) pension plans.

Under current law, workers can invest up to $10,000 per year in their 401(k) or 403(b) accounts with a variety of investment choices such as mutual funds. Workers are thereby able to supplement their retirement assets and take responsibility for their own futures rather than depending upon Social Security to meet their retirement needs.

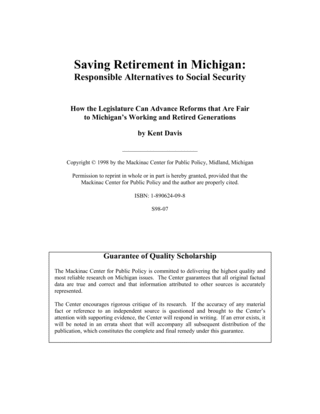

KPMG Peat Marwick, a major accounting firm, surveyed companies and individuals to determine that the rate of employee participation in 401(k) retirement plans is high and increasing (see Chart 1). The 1998 data show that 59 percent of nonhighly compensated employees and 81 percent of highly compensated employees participated (in 1998, the government considered workers making over $80,000 to be "highly compensated"). Employees contribute on average five to seven percent of their paychecks to their retirement plans, a figure roughly equivalent to what Social Security taxes take from their pay.

In many cases, employers match employee contributions to their plans at rates of 25 to 50 percent, which enhances the amount of savings employees can invest for retirement purposes. Another benefit for employees using these plans is that their contributions are pre-tax dollars, meaning the money is invested before taxes are taken out. Having this extra money to invest can add up. For example, an employee in the 15 percent tax bracket will have $150 more per year to invest for every $1000 he contributes. An employee in the 28 percent bracket would have $280 more per year, and so on. The taxes are deducted upon withdrawal of the money. Funds from IRAs and 401(k) and 403(b) plans cannot be withdrawn except for emergencies of personal hardship and are therefore working throughout an employee’s life to earn returns on the investment.

The Wall Street Journal recently reported that market forces have created low-cost retirement plans for even very small employers: 33 million people who work for companies of less than 50 employees are now becoming eligible to participate in building their own secure retirement through private plans. This will further boost the number of Americans investing in private retirement plans and likely create irresistible pressure for fundamental Social Security reform.

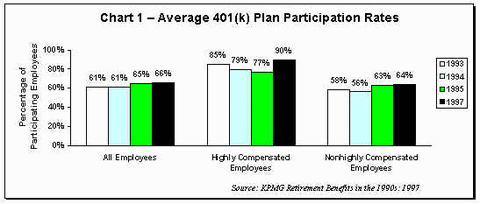

How do these 401(k) and 403(b) plans perform? Based on historical returns of at least seven percent in the stock market and four to five percent in bond markets, employees investing in these plans will far exceed anything Social Security will ever provide. The Cato Institute has documented the much higher returns generated by private investment over Social Security (see Chart 2). Cato has also established an interactive Internet feature at www.socialsecurity.org that allows users to supply their birth date and income estimates to calculate how much they can gain in future benefits through private investment.

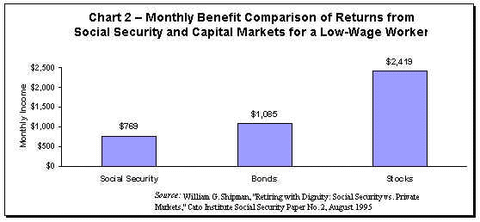

Meanwhile, however, lower-income workers remain at risk, with employees in the bottom 20 percent income group depending most heavily on Social Security benefits (see Chart 3, next page). The top 20 percent of earners are much better prepared and less dependent on Social Security. Within the next 20 years great gains can be achieved for lower-income workers by partially privatizing Social Security.

Private investment is the key to solving the impending Social Security crisis. While today’s payroll taxes are used to provide benefits to current retirees, the pre-tax funds invested in 401(k) and 403(b) accounts remain the property of each worker and will be there upon retirement. And as mentioned above, private investment offers greater returns.

(See Chart 3.)

But lower-income workers often cannot afford to invest any of their paychecks in retirement plans. They must, however, pay payroll taxes, and that is why Senators Daniel Patrick Moynihan of New York and Bob Kerrey of Nebraska have proposed partially privatizing Social Security by allowing individuals to use part of their payroll taxes to invest for retirement. Under the Moynihan-Kerrey plan, workers could shift two percent of their paychecks into privately managed accounts and expect to increase their retirement income from 9 to 35 percent more than what they would receive from Social Security if no changes were made, depending on their working income (See Table 1, below).

Net Percentage Change in Annual Retirement Income under the Moynihan-Kerrey Social Security Plan

Worker Earnings |

|||

| Estimates | Low Wage | Avg. Wage | Max. Wage |

| Without Income from Private Account | -11.0% | -11.0% | -6.0% |

| Including Income from 100% Bond Portfolio | 1.5% | 5.9% | 19.5% |

| Including Income from 50% Bonds/ 50% Equity Portfolio | 4.9% | 10.4% | 26.3% |

| Including Income from 100% Equity Portfolio | 9.4% | 16.4% | 35.3% |

Notes: Low-wage worker is assumed to earn 45% of average wage ($11,661 in 1996), average-wage worker is assumed to earn 100% of average wage ($25,914 in 1996), and maximum-wage earner is assumed to earn $62,700 in 1996. The real value of the maximum wage is scheduled to increase under the Moynihan-Kerrey plan. However, worker is assumed to invest only 2% of current law maximum taxable amount in retirement and to take the remainder as salary increase. It should be noted that although the Social Security benefit decrease for maximum wage worker under the Moynihan-Kerrey plan is smaller relative to average- and low-wage workers, this reflects a greater increase in payroll taxes for maximum-income worker as the maximum taxable threshold is substantially increased in the future above current law levels.

Source: Adapted from the Heritage Foundation Center for Data Analysis. Calculations based on projections of 1998 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds reductions are calculated on the basis of Congressional Research Service Memorandum to Representative Charles Rangel, "Benefit Analysis of Three Recent Social Security Reform Proposals," June 16, 1998. Worker is assumed to earn 10% return on equity investment (6.5% after inflation), 8.15% return on mixed bond/equity investment (4.6% after inflation), and 6.3% (2.8% after inflation) on Treasury Bonds.

If even two percent private investment could produce such gains for lower-wage workers, then allowing them to invest the 5.26 percent Social Security payroll tax deducted from their paychecks for retirement could produce even greater benefits. In fact, an official Social Security Advisory Council appointed by Department of Health and Human Services Secretary Donna Shalala has recommended completely converting half of the nation’s retirement accounts into individually owned, privately managed accounts.

The details of these various partial privatization proposals vary, but all have common threads including the private investment of a portion of the money deducted for current Social Security taxes and individual ownership of the funds. A word of warning, however, is required with regard to one category of Social Security "privatization" proposals which involves having the federal government manage the investment of retirement funds. Direct government investment in the stock market versus individually owned investment would lead to an unprecedented politicization of the American economy. Various political interests and pressures would likely negatively affect investment choices and possibly even reduce investment returns. "Politically incorrect" companies and their customers and stockholders would suffer, and all companies would likely open new wings in their lobbying departments to vie for government investment. In short, important market decisions about resource allocation and wealth development would be made by a small group of politicians and bureaucrats with an agenda, not by workers and retirees, the people with the largest stake in the investment. People’s retirement earnings should not be political footballs and American companies should not be dependent on government for the capital essential for their existence.

The major political challenge to effective Social Security reform involves managing the transition costs from a 100-percent government-funded system to some form of privatized investment. Critics argue that the reduced payroll taxes coming from workers who elect to start managing their funds privately would cause a shortfall to the Social Security trust fund that pays benefits to current retirees and those workers who do not opt out of the system. How could this shortfall be made up?

Studies conducted by the Cato Institute and other researchers have shown how transition costs to a privatized pension system can be managed. Partial privatization would allow workers to either shift a portion of the money they normally pay in Social Security taxes into a privately managed and owned account or remain in the Social Security program. In the first year of partial privatization, an estimated 50 percent of workers would elect to opt out of Social Security in favor of privatized accounts. The following year the number would increase to 75 percent and finally reach 90 percent in the third year. In less than 15 years, Social Security would begin enjoying surpluses and within 40 years, $770 billion surpluses would be created per year (Table 2 is not available in the online study. Please order the study for full content).

A variety of proposals have been made that outline how to finance the transition costs which arise when people start withdrawing a portion of their payroll taxes from Social Security and investing it in private accounts. Most of these proposals require the employer portion of the payroll taxes to continue to be paid into Social Security until the transition costs are fully paid in 20 to 30 years. As Table 2 shows, additional funds would come from expected government surpluses and sale of government bonds and assets. The exact proportion of each source of transition financing will depend on economic conditions such as growth rates, interest rates, and feasibility of asset sales.

The speed with which the United States could expect to move into a totally privatized retirement program is ultimately dependent on both economic and political factors. The advantages of partial privatization include first building public acceptance and confidence through demonstrated results and care for current beneficiaries. The experience of other countries that have already instituted privatized pensions has been that over 90 percent of the workers convert to the private program within just three to five years.

Government’s ability to raid the Social Security trust fund would be lost once the country made the switch to privatized accounts, resulting in improved fiscal discipline and a sounder economic footing for retirees. The increased saving and investment would also fuel a new boom in economic growth.

In May 1997, the Oregon Legislature approved a resolution urging Congress to grant waivers to let states opt out of the federal Social Security system and design their own retirement plans for all workers, government and private. The resolution was based on a study produced by the Cascade Policy Institute, an Oregon-based free-market research organization. Author Randall Pozdena also proposed an alternative retirement system for Oregon, if Congress granted a waiver. Key features of his plan include

Funding the transition to a private system by requiring employers to continue paying their 5.26 percent share of Social Security taxes for another 20 years;

Requiring workers to contribute their 5.26 percent share of Social Security payroll taxes into qualified investment plans of their choosing;

Shifting workers born after a certain date (perhaps 1955) from the federal Social Security system to the new state-based plan; and

Continuing retirement benefits to current Oregon retirees equal to their benefits plus inflation adjustments.

The predicted results of the Oregon plan would be that over a 20-year period the existing system would be phased out and all new retirees would be receiving improved benefits as a result of superior investment returns. These predictions are based on the fact that no 20-year period since 1800 has witnessed overall negative investment returns, despite short-term cycles and disruptions.

In May 1998, Colorado also adopted an opt-out resolution and Arizona, Indiana, Missouri, New Hampshire, South Carolina, and Washington are considering similar measures. See Appendix B on page 19 for the full text of Oregon’s original resolution.

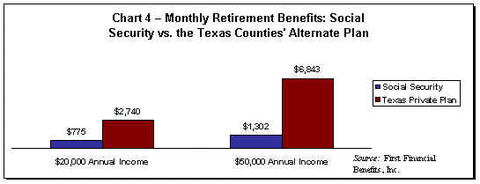

A specific example of smaller local units of government choosing to opt out of Social Security to design their own pension plans occurred in 1981, when Congress still allowed government units to make that choice. The three Texas gulf coast counties of Brazoria, Galveston, and Matagorda selected a private investment firm to manage their employees’ retirement plans with a guaranteed annual return of 6.5 percent.

By 1996 the results were in, and county employees’ retirement benefits were triple what would have been paid by Social Security for a worker who earned $20,000 per year and over five times the Social Security benefits for a worker whose pay was $50,000 (see Chart 4, next page). Congress closed the local government opt-out window in 1983 with major Social Security reform legislation that raised taxes and effectively reduced benefits by raising the eligible retirement age after 2015. (See Chart 4.)

The United States is not unique in instituting mandatory government-sponsored pension systems. Such programs were actually started in 1870s Germany by Chancellor Otto von Bismarck. He arbitrarily selected 65 as the retirement age, which is striking when one considers that life expectancies were under 50 at the time. Clearly, Bismarck and the original designers of the government retirement systems expected few benefits to be paid.

In the 20th century, government pension programs have become an important part of the "social safety net" in many developed countries. A number of countries, such as Chile in South America, started their programs before the United States created Social Security. But the inexorable dynamics of lower birth rates, longer life expectancies, and the political appeal of greater retirement benefits have put increasing burdens on government-funded pension programs in every country that has one.

In 1980, the pressures on Chile’s government system became too great and a new system was introduced which allowed Chileans to opt out in favor of private investment. Large numbers of Chileans chose to leave the failing government system, and the results have been greatly increased benefits paid out to Chilean retirees.

Other countries including Great Britain and Australia have revised their programs to include a small guaranteed government pension supplemented by a combination of employer-sponsored and personal pension plans under private management. Participation rates in the partially privatized systems are in excess of 90 percent and assets are growing at greater market return rates.

The United States already has 15 years of partial privatization experience with retirement instruments such as IRAs and 401(k) and 403(b) plans. As a result, large numbers of citizens in Michigan and across the country understand this approach, making it a politically popular—as well as sound—Social Security reform idea.

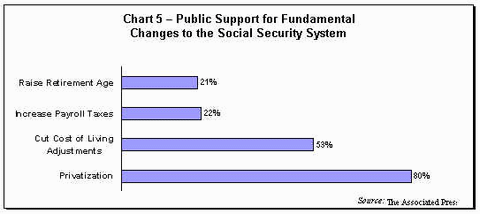

Polling evidence has been accumulating for several years that shows widespread public support for fundamental Social Security reform. Americans’ perception of Social Security has dramatically shifted in the past 10 years. Most recently, a March 1998 Associated Press poll found that 80 percent of respondents supported the concept of privatization—letting workers shift some of their Social Security taxes into personal retirement accounts that they could manage on their own (see Chart 5).

Michigan has an especially strong incentive to favor fundamental reform to the existing Social Security system. The Heritage Foundation has done a state-by-state analysis of expected returns for future retirees. Projected benefits under Social Security were compared with what could be expected if workers were allowed to invest their payroll taxes privately in bond and equity markets. Due primarily to being a heavily urbanized state with a relatively high percentage of lower-wage workers, Michigan ranks 40th or below in expected Social Security returns among the 50 states. The lower returns amount to a net loss of almost $580,000 in retirement income per Michigan worker over a lifetime (Table 3 is not available in the online study. Please order the study for full content).

Projected Lifetime Social Security Taxes and Benefits Compared with Accumulation from Private Investments for Double-Earner Couple Born in 1967 with Two Children, in 1997 Dollars

This data is not available in the online study.

The Michigan Legislature Should Ask Congress to Privatize Social Security or Grant a Waiver for the Purpose of Opting Out of the System

The Michigan Legislature should adopt a resolution similar to the one passed by Oregon in 1997 asking Congress to either

Partially privatize the existing Social Security program by allowing workers to shift all or part of their current 5.26 Social Security retirement payroll taxes into privately owned and managed accounts up to the allowable limit of $10,000 per year; or

Grant the state of Michigan a waiver to opt out of the federal Social Security system and design a sounder and more beneficial retirement plan for its citizens.

The existing federal Social Security system is streaking inevitably toward fiscal insolvency. Its financial problems can only be resolved—temporarily—by raising taxes and cutting benefits. But a fundamental and long-term solution is a system of partial privatization that allows workers to take control of their own retirement planning.

Many countries have already turned to private investment to restore fiscal soundness and improved retirement benefits to their government pension programs, increasing retirement security for millions of citizens. With a strong economy and government surpluses forecast for the next decade, the United States is in a strong position to successfully move to a privatized pension program that stimulates economic growth, promotes private savings, and restores individual freedom.

Countries including Chile, Great Britain, and Australia have had great success with their partially privatized pension programs. Nevertheless, a number of concerns have been raised against the idea of privatizing Social Security. This appendix answers some of the more common concerns about Social Security privatization.

Why does Social Security need a drastic overhaul? Can’t it just be fixed the way it has been in the past?

Past changes made to Social Security were designed to postpone the final "day of reckoning" and they included cutting benefits, hiking payroll taxes, and raising the retirement age. The trouble is that the day of reckoning is here. Longer-term trends, starting about 2012, show that Social Security will be taking in less money per year than it must pay out in benefits to retirees. Changes in demographics (there will soon only be two workers to support every one retiree, down from the 16-to-1 ratio when Social Security began in 1935) will make earlier fixes not only unpopular but also unfair and immoral. Any payroll tax increase will have to be confiscatory to meet the coming burden, and raising the retirement age still further will only cheat more workers out of ever seeing a return on their lifetime of taxes paid into the system. Dramatic and systemic change is needed.

Why is "privatization" the best alternative for Social Security reform?

There are three main reasons why privatization of pension funds is the best alternative to the failing government-funded system. The first is that market-based investment returns have historically been much higher than those of Social Security, which means that retirees can enjoy greater benefits in their golden years. The second reason is that privatization does not rely on an unstable "pay-as-you-go" pyramid scheme where current taxpayers are forced to subsidize current retirees rather than save for their own retirements. Privatization instead allows each worker to own and control his own retirement savings account. Third, increased private investment and savings will provide the economy with new sources of capital, which fuels growth and job creation.

Isn’t private investment in the stock market too risky? Wouldn’t I stand to lose my nest egg if I invested my retirement funds for myself?

Investment—whether in savings accounts or bond and equity markets—always carries with it some risk. However, the essential point regarding retirement accounts is that they are invested over an entire working lifetime, which means that short-term economic fluctuations are less important factors. Over longer periods of time, investments do well: Since 1800, there has never been a 20-year period in the United States when investment returns were not positive. For bond markets, the average 20-year return has been 3 to 4 percent while stock market returns have averaged an impressive 7 percent. Keep in mind that this century has had several major upheavals including the two World Wars, the Great Depression, and many weather-related catastrophes including earthquakes, storms, floods, and droughts. All of the long-term investment gains take these disruptions into account.

But couldn’t I lose it all during a stock market crash like in 1929?

That is unlikely. Workers are far more likely to suffer poor returns from Social Security than they are to suffer huge losses in their private investments. Over a working lifetime of 30 to 40 years there will be some ups and downs in markets as well as the economy. Recessions, wars, depressions, and economic stresses from temporary factors such as fires and floods are part of history, and neither markets nor government programs are immune from them. Lifetime planning can yield compounding growth rates of 4 to 7 percent on investment returns and provide tremendous increases despite short-term disruptions. Government-sponsored pensions, by contrast, never promise more than two percent returns, which is even less than long-term inflation rates.

How do we know privatization works?

Several countries such as Chile, Great Britain, Australia, and even Sweden have already made the change to either partially or totally privatized pension programs. The results have met or exceeded expectations, with retirees under the new plans seeing greatly increased benefits and earnings. In the United States, three counties in Texas opted out of the Social Security system in 1981 and designed their own privatized pension plan. County employees now enjoy retirement benefits three times greater than what Social Security would have paid. Likewise, private retirement savings plans such as IRAs or 401(k) and 403(b) plans routinely outperform Social Security.

Won’t poor people who can’t afford to save any money lose under privatization?

No. Lower-income people who do not have any private savings today will be the greatest beneficiaries under privatization. Here’s why: 5.26 percent of their pay is currently taken for Social Security taxes. Because that money is immediately transferred to current retirees, there is no nest egg being built up for the low-income taxpayer. If instead all or part of that 5.26 percent were privately invested on behalf of the worker, he would own and control his own retirement account and could count on greater returns for his money. Those people who have no savings would be able to accumulate funds for their own retirement without any noticeable difference in their paychecks.

How can I find out more about what privatization of Social Security would mean for myself, my family, and my retirement?

The Cato Institute, a Washington, D. C.-based public policy research institute, has studied Social Security privatization for the past several years. Research from their Project on Social Security Privatization can be found on the Internet at www.socialsecurity.org. The interactive Web site features a calculator tool that allows you to input personal data such as age and income level to calculate what you stand to gain if your Social Security taxes were invested in a privately managed retirement account under your control.

For further reading, please see Appendix C for a bibliography.

For further reading, please see the following papers on Social Security privatization, available from the Cato Institute’s Project on Social Security Privatization at www.socialsecurity.org.

William Shipman, "Retiring with Dignity: Social Security vs. Private Markets," August 14, 1995.

Michael Tanner, "Privatizing Social Security: A Big Boost for the Poor," July 26, 1996.

Michael Tanner, "Public Opinion and Social Security Privatization," August 6, 1996.

Krzysztof M. Ostaszewski, "Privatizing the Social Security Trust Fund? Don’t Let the Government Invest," January 14, 1997.

Peter J. Ferrara, "A Plan for Privatizing Social Security," April 30, 1997.

Melissa Hieger and William Shipman, "Common Objections to a Market-Based Social Security System: A Response," July 22, 1997.

The author wishes to acknowledge Mackinac Center for Public Policy Senior Vice President Joseph Overton for his help and advice in this project as well as former Mackinac Center Research Intern and current Hillsdale College student Josh Mercer, whose assistance was invaluable. Mackinac Center Policy Writer and Editor David Bardallis provided indispensable editing services.