|

City |

Monthly Rate 1991 |

Rate Per Channel 1991 |

Monthly Rate 2006 |

Rate Per Channel 2006 |

Nominal Increase |

Real Increase |

|

Royal Oak |

$20.25 |

$0.30 |

$43.49 |

$0.65 |

114.8 % |

47.8 % |

|

Detroit |

$17.00 |

$0.31 |

$48.99 |

$0.65 |

111.3 % |

45.4 % |

|

Troy |

$20.25 |

$0.29 |

$43.49 |

$0.61 |

108.7 % |

43.6 % |

|

Berkley |

$20.25 |

$0.30 |

$43.49 |

$0.61 |

103.3 % |

39.9 % |

|

Southfield |

$18.50 |

$0.40 |

$48.99 |

$0.71 |

76.5 % |

21.5 % |

|

Taylor |

$16.50 |

$0.38 |

$43.49 |

$0.63 |

68.1 % |

15.7 % |

|

Pontiac |

$19.95 |

$0.45 |

$48.99 |

$0.74 |

63.7 % |

12.7 % |

|

Bloomfield Hills |

$19.68 |

$0.44 |

$48.99 |

$0.70 |

60.0 % |

10.1 % |

|

Livonia |

$16.95 |

$0.35 |

$43.95 |

$0.55 |

55.6 % |

7.1 % |

|

Birmingham |

$19.68 |

$0.44 |

$48.25 |

$0.67 |

53.2 % |

5.4 % |

|

Dearborn |

$18.90 |

$0.40 |

$43.49 |

$0.61 |

52.3 % |

4.8 % |

|

Farmington Hills |

$16.95 |

$0.39 |

$43.95 |

$0.55 |

39.4 % |

- 4.1 % |

|

Warren |

$21.75 |

$0.49 |

$43.49 |

$0.66 |

33.3 % |

- 8.3 % |

|

Plymouth |

$19.95 |

$0.49 |

$43.49 |

$0.64 |

31.4 % |

- 9.6 % |

|

Inkster |

$16.95 |

$0.51 |

$48.99 |

$0.67 |

30.7 % |

- 10.1 % |

|

AVERAGE |

$18.97 |

$0.41 |

$45.70 |

$0.64 |

66.8 % |

14.8 % |

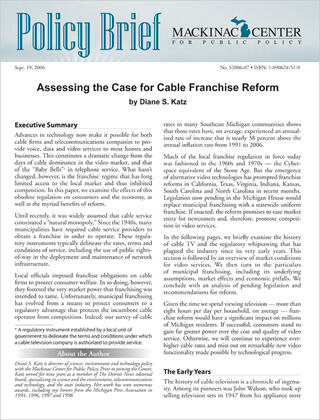

Sources: 1991 Data from Tim Kiska and The Detroit News; 2006 data from Comcast and Bright House.

As noted earlier, the technology to deliver competing video services does exist, but few consumers actually have access to the range of service options. The principle culprit is local franchising, which, according to numerous studies, restricts competitors’ entry into the local market.

The number of municipal franchising authorities nationwide exceeds 33,000, and there are some 1,200 in Michigan alone.[27] Internet-based video services are not explicitly compelled by law to obtain a local franchise from a municipality, as is cable. Nonetheless, under the guise of "a level playing field," most municipalities as well as cable industry executives demand that newcomers obtain a franchise with provisions identical to that of the incumbent before launching service. But having to secure agreements from every community in which it hopes to operate presents to newcomers an insurmountable barrier to market entry.

Municipal officials promise to negotiate in good faith with prospective competitors, and no doubt many would. But even if a municipal franchise were to be issued quickly, the regulatory requirements therein would be economically unsustainable — and nonsensical. As economist Thomas Hazlett points out, the argument for a so-called level-playing field "serves to justify franchise obligations for entrants even as the original rationales — natural monopoly and rate regulation — have disappeared. The premise of regulation has flipped from consumer protection to incumbent protection."[28]

It is important to remember that incumbent cable firms were granted a monopoly in exchange for conceding to rate regulations, service giveaways and "build-out" requirements that mandate service to all residents irrespective of consumer demand or infrastructure costs. New competitors, however, can only expect to garner a slice of a market already dominated by a cable service provider and where satellite services have likewise existed for years. As Thomas Hazlett explains: "(I)dentical franchise obligations are typically far more economically burdensome for competitive entrants."[29]

Consequently, legacy franchise requirements dissuade investment in competing video services.

Local officials say they must maintain franchise control in order to regulate the use of public property on which network infrastructure is located. However, municipalities would retain this authority even if lawmakers established statewide franchising, as has occurred elsewhere. Moreover, most broadband service providers already pay municipalities for the use of local rights of way.

Build-out requirements are among the most egregious provisions of municipal franchises with respect to stifling competition. Build-out requirements force companies to offer services regardless of population density and the cost to deploy service — all of which runs counter to a rational business plan and which dissuades investors from entering the market. Like other businesses, video firms understandably seek to establish new service where demand is likely to be greatest (cities) and, therefore, where returns will be maximized. Positive returns enable expansion, which would fuel expanded deployment into less populated areas.

"The financial investment undertaken by cable systems embeds a projection of future returns that is fundamentally altered when the pattern of network construction is controlled by external political agents," said Hazlett.[30] "Congress, in the Cable Consumer Protection and Competition Act of 1992, explicitly advised local governments to waive strict build-out requirements that discouraged competitive entry. Unfortunately, there was no enforcement mechanism included."

Far from leveling the playing field between incumbent and competitor, build-out requirements actually undermine the newcomer. The incumbent’s build-out occurred in the past, and has long been absorbed by its rate structure. But the cost of build-out to rivals is fully in the present, when the pressure to keep rates low is far greater than when the incumbent entered the market without rivals.[31]

Build-out requirements are simply unnecessary because telecommunications firms have every incentive to increase market share, not rebuff customers. Low-income households, in particular, are heavy consumers of video services, and constitute the fastest growing segment of the broadband market.

Further obstacles to competition are the municipal franchise provisions that require free video services for schools and colleges, all manner of government facilities, as well as for "public access." Aside from the sheer audacity of forcing a business to give government free service, there is the potential conflict of interest in having office holders wielding control of TV content.

As illustration, consider the case of a suburban Detroit mayor who pulled a tape of a forum sponsored by the League of Women Voters because the mayor apparently disagreed with the views expressed on the program. The forum had been organized to discuss whether the charter should be amended to move the city from a strong-mayor form of government to a city manager form. Or consider the member of a city council who stalled a vote on franchise renewal over a cable company’s resistance to providing free service to residents.

According to a study by the Phoenix Center for Advanced Legal & Economic Public Policy Studies, a one-year delay in competitive entry due to franchise agreements costs consumers $8.2 billion in benefits.[32] That makes the barriers to competitive entry caused by local franchising far in excess of the revenue generated by the franchise fees paid to the municipalities.