Baseline Assumptions

The baseline assumptions for SEV, millage rates, new construction rates, and some other variables were taken from the SFA study by Jay Wortley and George Towne, Property Tax Reform Proposals in Michigan, along with some additional nonpublished data supplied by the authors. These key assumptions include:

Baseline SEV growing 10.8% in 1993, and 6.5% afterwards;

New construction accounting for 2% of SEV growth annually; and

Millage rates which grow under current law, but grow higher under Cut and Cap.

Other assumptions and features of the model were:

Turnover (sales of property) of 10% a year – a faster rate than in the SFA study;

For HJR H, directly calculated 1993 millage rates, based on application of the Headlee amendment, and using a conservative 7.5% inflation rate for 1991 and 1992 combined;

A Capitalization Ratio of 8, equivalent to about an 12% cap rate, which is quite conservative; and

Tax multipliers of 7.6% for the General Fund, 14% for the Homestead Income Tax Credit, 3.35% for Other Funds; and (1%) for Outlays. These are described below.

Dynamic Effects

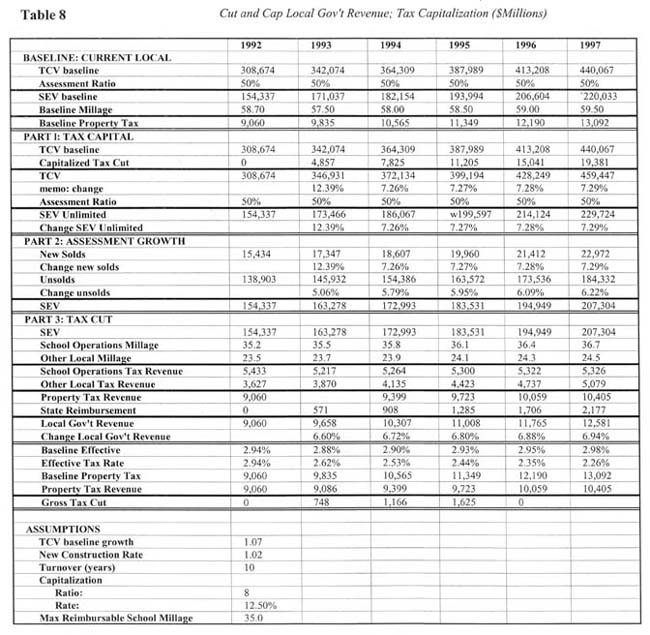

The model used for revenue analysis of Cut and Cap attempts to incorporate some dynamic effects normally left out of revenue models. The first is tax capitalization. A provisional tax cut is calculated, using a simple static analysis. In the case of Cut and Cap, the provisional tax cut in 1997 would be 30% of the school operating tax, based on the baseline estimates of school millage and SEV. The provisional tax cut is then capitalized, by multiplying it by the capitalization ratio. This capitalized tax cut is then added to the baseline True Cash Value (TCV), and, multiplied by the assessment ratio, becomes the (unlimited) SEV for the Cut and Cap projection. This SEV will be larger than for current law, so the gross tax cut – the difference between current law and projected tax revenue – will be smaller than a straight 30% share.

A second area of dynamic influence is the projection of additional tax revenue from other taxes. This is simply a factor multiplied by the gross tax cut. In addition, a reduction in outlays for social programs is also incorporated, driven by a simple factor.

The capitalization ratio and other dynamic factors used in the model are extremely conservative. A true, full dynamic model would attempt to include changes in employment, investment, and other factors. The modest effects in this model indicate the direction of dynamic change more than its magnitude.

SEV Algorithm

The assessment growth cap presents a difficult modeling problem. The algorithm used here to project SEV under the assessment cap works as follows:

An unlimited SEV series is created, based on the True Cash Value, as augmented by tax capitalization.

A share of the current year SEV, equal to 1/T where T = the turnover period, is calculated as equal to the same share of unlimited SEV. This accounts for the newly sold parcels.

The remaining (T-1)/T share is projected from last year's SEV, by adding new construction and increasing it at the limited (3%) rate.

Since we have no experience with an assessment growth cap in Michigan, actual results may prove quite different.

School Reimbursement

School Reimbursement was calculated using a limiting factor of 35 mills, the approximate average school operating millage in 1992.

Aggregation Problem

This, and all models, suffers from the fact that averages and totals were used, rather than truly aggregating all the various local units of government. This will always introduce some error.

Comparison With Other Revenue Analyses

One methodological difference between this study and those by Treasury and SFA is the inclusion of tax capitalization and larger state tax revenues from the additional disposable income of Michigan property owners. These factors did not cause the estimates of gross tax, school reimbursement, or net impact on the general fund to be significantly different, for the following reasons:

The assessment growth cap allows increases in property values to affect SEV only as property is sold, delaying its effect on property tax revenue; and

The additional revenue from other taxes was offset by larger estimates of income tax credits in the SFA and Treasury studies.

However, these studies did not incorporate tax capitalization.

A summary of the different revenue projections is given in Table Five on page 23.