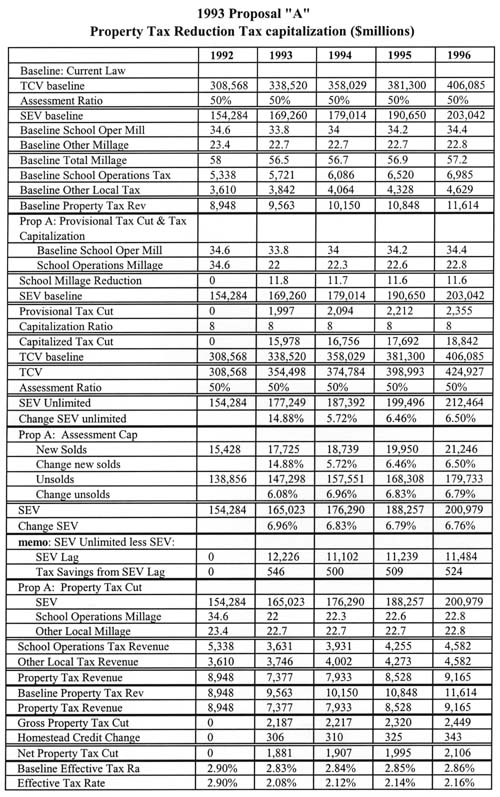

Baseline Assumptions

The revenue projections were generated by an economic model developed by the author for the Mackinac Center for Public Policy. The model differs from the standard, "static" models commonly used in government agencies, in that it attempts to estimate the actual dynamic behavior of individuals when confronted by changes in tax rates.

The baseline assumptions [48] for current law include:

SEV growing 9.7% in 1993 (coming off the "freeze" during 1992), 5.8% in 1994, and 6.5% annually in the succeeding years;

New construction accounting for 2% of SEV growth annually;

Millage rates which continue to grow under current law; and

An assumed state reduction in "Homestead" or "Circuit Breaker" Income Tax Credits of 14% of the gross property tax reduction.

Legislative and Local Government Assumptions

The model does not assume that any other companion tax reduction legislation will pass, beyond that necessary to implement "A." In particular, it does not include Senate Bill 146, which would create a one-year lag in assessments in 1994. This is a key difference between this independent study and the "consensus" revenue estimates adopted by the staffs of the Department of Treasury, Senate Fiscal Agency, and House Tax Committee.

School millage rates have been increasing under current law and indeed are a major justification for the proposal. As discussed in the text. the proposal would probably result in more taxpayer control of school finances, and slower-growing millage rates. Nonetheless, to make the tax-reduction projections more conservative, school millage rates were assumed to grow at 3/10 a mill each year through 1995 under the proposal, 50% faster than the 2/10 a year rate assumed under current law.

Dynamic Effects

There are three explicit dynamic effects in the model. The first is tax capitalization, discussed at length in Appendix II. A provisional tax cut is calculated, using a simple static analysis. The provisional tax cut is then capitalized, by multiplying it by the capitalization ratio. This capitalizedtax cut is then added to the baseline True Cash Value (TCV), and, multiplied by the assessment ratio, becomes the (unlimited) SEV for the "A" projection. This SEV will be larger than for current law, so the gross tax cut – the difference between current law and projected tax revenue – will be smaller than a static analysis would indicate.

The second area of dynamic influence is the projection of additional tax revenue from other taxes, on additional disposable income left from the property tax cut. A fraction of this is assumed to be taxed, after incorporating the avoidance factor for the sales and use taxes. The third dynamic effect is the tax avoidance behavior of consumers.

Assumptions for dynamic effects in the model include:

Turnover (sales of property) of 10% a year.

School millage rates which grow faster under "A" than under current law for the first few years, both because of fewer "Headlee" rollbacks, and the possibility that school districts would attempt to regain some of the reduction in millage.

Tax avoidance by Michigan taxpayers, who are assumed to reduce their tax payments by 1/10th the proportional increase in the sales and use tax rates. This "elasticity" is assumed to the 2/10 in 1993, when consumers could easily accelerate purchases of big-ticket items to avoid the sales and use tax increases.

A Capitalization Ratio of 8, equivalent to about an 12% cap rate.

The capitalization ratio, tax elasticity, and other dynamic factors used in the model are conservative. A full dynamic model would attempt to include changes in employment, investment, and other factors, and would likely generate larger dynamic changes than those indicated here.

SEV Algorithm

The assessment growth cap presents a difficult modeling problem. The algorithm used here to project SEV under the assessment cap works as follows:

An unlimited SEV series is created, based on the True Cash Value, as augmented by tax capitalization.

A share of the current year SEV, equal to 1/T where T = the turnover period, is calculated as equal to the same share of unlimited SEV. This accounts for the newly sold parcels.

The remaining (T-1)/T share is projected from last year's SEV, by adding new construction and increasing it at the limited rate.

Aggregation Problem

This, and all models, suffers from the fact that averages and totals were used. rather than truly aggregating all the various local units of government. This will always introduce some error.