This summer, President Bush's commission on reforming Social Security issued an interim report stating that the program will run out of money in just 15 years. The report warns that deep benefit cuts, tax increases, or the acceptance of massive federal debt are necessary—unless there is fundamental reform of the system.

According to a report by Henry Aaron of the Brookings Institution in Washington, D.C., Social Security as currently constituted offers individuals, on average, an amount of money that is just 10 percent above the line the U.S. government defines as "poverty." The report also points out that Social Security is an especially bad deal for women, blacks, Hispanics, and the poor in general. Social Security expert William Beach of the Heritage Foundation has found that many young black males working today will pay more into the system in their lifetimes than they will receive in benefits—a negative return.

Due primarily to the fact that it is a heavily urbanized state with a relatively high percentage of lower-wage workers, Michigan ranks 40th or below in expected Social Security returns among the 50 states. The lower returns—when compared with what, on average, a typical two-worker family could earn by investing that money—amounts to a net loss of almost $580,000 per family in retirement income.

For these reasons—and for many positive ones as well—it is gratifying to me, as a senior citizen, to know that America is approaching the day when it will pass a fundamental reform of Social Security; one that will probably allow people to own a portion of their payroll taxes now devoted to the program, and invest that portion on their own.

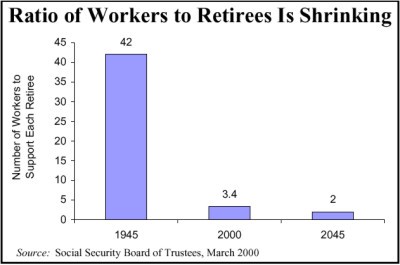

Many of my fellow senior citizens are worried about tampering with a government program that has been in place for most of their lives. But what must be said repeatedly and with no apology is that the system enacted in 1935 was always unsustainable under a particular circumstance: if the ratio of workers to retirees ever became so low that a reasonable level of benefits could no longer be maintained.

What many Americans still don't understand is that that ratio is being reached, and quickly. That's why the calls for reform are finally being heard. Social Security initially had over 50 people paying in per retiree. Today, that ratio is around 3:1 and will drop to 2:1 in the next few decades.

People are living much longer and retiring earlier, many even before Social Security starts paying them benefits. Retirement at age 55 is now a common, and growing, phenomenon. The only way people can retire early is if personal savings and pensions are available to sustain a desirable lifestyle in retirement, the more the better. Millions of Americans already have accumulated tax-sheltered assets in accounts such as IRAs and 401(k)s.

Unfortunately, low-income workers lack the discretionary income necessary to fund such accounts. A Social Security system that allows private investment would give these workers the leg up they need to retire with a nest egg big enough to live a comfortable lifestyle. By investing in government bonds over a working lifetime, a person can get a 3-4 percent return which, through the magic of compound interest, doubles monthly retirement income. A broader mix of stocks and bonds, with historical yields of 5-6 percent, effectively triples retirement income.

And here's something else most Americans don't know: Other countries have made precisely the same change America is contemplating. For example, Great Britain gives workers the option of placing a portion of their payroll taxes in a private investment account. More than two-thirds of British workers have chosen the private option. The result: Private pensions are generating a 10-percent real return on their pension investments. British pension funds are currently greater than the pension funds of the rest of the European countries combined.

But seniors should rest assured: No one is talking about "doing away with Social Security." No one is suggesting that the current level of benefits be reduced, nor are they proposing that the new reform be anything but voluntary. Should a partial privatization of Social Security occur, you will not be forced to participate.

But if you want the highest possible return on your investment of a lifetime of hard work, you should.

#####

(Kent Davis, a retiree with over 35 years of managerial experience, is a senior policy advisor to the Mackinac Center for Public Policy. Permission to reprint in whole or in part is hereby granted, provided the author and his affiliation are cited.)

The Mackinac Center for Public Policy is a nonprofit research and educational institute that advances the principles of free markets and limited government. Through our research and education programs, we challenge government overreach and advocate for a free-market approach to public policy that frees people to realize their potential and dreams.

Please consider contributing to our work to advance a freer and more prosperous state.