Discussions about school funding can create more confusion than clarity. Each state has its own intricacies and peculiarities. Michigan is no exception. Funding flows down from different sources, often based on different formulas and intended for different purposes. There’s no one unified system that controls school funding — rather, schools rely on a number of systems layered on top of each to supply them with resources.

This publication presents a brief overview of some of the key components of Michigan’s school funding system, if it can be called that. The goal is to provide a general understanding of how tax dollars reach schools and what they are intended for.

Discussions about school funding can create more confusion than clarity. Each state has its own intricacies and peculiarities. Michigan is no exception. Funding flows down from different sources, often based on different formulas and intended for different purposes. There’s no one unified system that controls school funding — rather, schools rely on a number of systems layered on top of each to supply them with resources.

This publication presents a brief overview of some of the key components of Michigan’s school funding system, if it can be called that. The goal is to provide a general understanding of how tax dollars reach schools and what they are intended for.

Each chapter focuses on a different funding component, including the foundation allowance, state funding through categorical grants, the financing and role of intermediate school districts, special education funding, revenue for building construction and maintenance, and, finally, how federal funds work.

While the Michigan Legislature debates how much funds to devote to schools every year and certain components may change over time, a lot of the key elements mostly stay the same. So, even though the figures might change from year to year, the concepts described in what follows will remain useful into the future.

Michigan’s school finance system has not been designed for the sake of simplicity. One of the most common points of misunderstanding relates to the state’s use of a “foundation allowance,” which is a revenue stream that comprises the bulk of operating money for the state’s 540 conventional school districts and 300 public charter schools.

The foundation allowance was created after voters approved Proposal A in 1994. Previously, most education dollars derived from local property taxes. But this produced large geographically based funding disparities: districts containing valuable property could raise lots of money for their schools, those with less valuable property not as much.

Proposal A changed all of this. Instead of letting local property values determine funding levels for districts, the foundation allowance is allocated based on the number of enrolled students, with districts receiving a set amount for each student. The foundation allowance is the minimum amount of money per student that the state Legislature guarantees each district will receive. As such, the disparities in the value of local property among districts has no impact on this portion of school funding.

Proposal A was not designed to bring perfect funding equity for all school districts, however. Rather, the plan was to gradually reduce disparities by providing lower-funded districts with larger increases so they could eventually catch up with their higher-funded peers. And over the last two decades, the foundation allowance gap has closed significantly. The highest-funded district in 1994 received a foundation allowance 3.7 times greater than the lowest-funded district. Today, the highest-funded district’s foundation allowance is only about 60 percent larger than the minimum received by most districts.

About three-fourths of districts and all charter schools received the minimum foundation allowance of $7,511 per pupil in 2017. That amount is nearly $3,000 more than the lowest-funded districts received before Proposal A, adjusted to today’s dollars. Meanwhile, today’s largest foundation allowance of $12,064 is over $4,000 less than the largest foundation allowance in 1994, if increases had kept pace with inflation.

Two student counts — one in October and one in February — are used to determine the actual amount the state must pay each district through the foundation allowance. A district’s final enrollment is calculated by adding 90 percent of the October count to 10 percent of the previous year’s February count.

Although the Legislature sets its level and the foundation allowance is considered “state funding,” it is actually financed through a mix of state and local revenues. The local revenue comes from a tax on all “nonhomestead property” in a district — commercial and industrial property or houses that are not a person’s primary residence. Most every school district levies the maximum allowable rate of 18 mills on nonhomestead property to fund a portion of their foundation allowance revenue.

The remaining state-based revenue needed for the foundation allowance comes from the School Aid Fund, which is financed by numerous state taxes. The sales and income taxes and the State Education Tax — 6 mills levied on all property, including primary residences — make up the bulk of the revenue for the School Aid Fund. Lottery revenues also contribute, but make up only 7 percent of these revenues. Other sources include the use tax, tobacco tax and real estate transfer tax.

Graphic 1: Michigan’s Shrinking Foundation Allowance Gap (in 2016 dollars)

- click to enlarge")

Source: Michigan Senate Fiscal Agency

The amount that the state contributes to each district’s foundation allowance varies district to district. It works like this: The state calculates how much local revenue a district will get from its nonhomestead tax and then fills in whatever is required to fully fund its foundation allowance. For example, if a district’s local revenue provides $5,000 per student, the state would contribute $2,511, so the district would receive a total of $7,511 per student through the foundation allowance.

Because there’s still wide variation in how much local revenue school districts can raise, the amount that the state contributes to each district can vary considerably. In fact, in a small number of cases, school districts can raise enough money to fund their foundation allowance themselves without the state kicking in any funds. These are sometimes called “out-of-formula districts.”

Other districts rely heavily on the state to finance their foundation allowance. And, one final wrinkle, all public charter schools, because they cannot levy any taxes of their own, rely entirely on the state to fund their foundation allowances.

There are additional nuances. For example, some school districts are assigned a foundation allowance that exceeds the minimum. And some districts are allowed to levy an additional local tax to supplement their foundation allowance. When Proposal A was passed in 1994, these districts had relatively higher funding levels, and the rationale for letting them remain at these higher levels was to hold them “harmless” from the funding reform.

A final important point about the foundation allowance is that it is only one revenue source for school districts. Most districts receive significant amounts of money from other local, state and federal sources. Including these other sources finds that Michigan schools on average collected $14,307 in revenue for every full-time student enrolled in 2016. Nevertheless, the foundation allowance is schools’ most important funding mechanism, because it is the primary source of revenue schools use for their core operations, such as employing teachers, purchasing instructional materials and keeping the lights on.

If asked how much funding Michigan schools receive on average, a reasonably well-read observer might guess between $7,000 and $8,000 per student. This is not entirely off base: news stories commonly report how much districts get through the state’s foundation allowance, which typically falls in that range. But schools receive a lot more money than that, and a good chunk of this additional revenue comes from the more than 50 “categorical grants,” created by the Legislature and funded by over $3 billion in state tax dollars annually.

A sizable portion of these categorical grants go to local and intermediate school districts based on certain student or district characteristics. For instance, a categorical grant worth nearly $380 million is allocated to districts based on the number of enrolled students who are deemed “at-risk” of academic failure. Other smaller outlays are paid out to geographically “isolated” districts, to provide services to non-English language speakers and to help districts provide free and reduced-price lunches to low-income students.

The largest single categorical grant is used to hold districts harmless from the growing costs of the state’s massively underfunded school employee pension system. Just over $1 billion per year is spent for this purpose. Since most of this spending is dedicated to “catching up” on the state’s $29.1 billion school pension debt, today’s taxpayers are paying the costs of yesterday’s classrooms through this categorical. One example of a categorical grant is support for certain districts to purchase “locally-grown fruits and vegetables.”

One example of a categorical grant is support for certain districts to purchase “locally-grown fruits and vegetables.”

Categorical grants are used to pay the costs of other school-related debt, too. About $130 million is paid out annually to service the debt on money the state borrows to help districts make payments on money they’ve borrowed. This is how the state’s School Bond Loan Fund program works, which only benefits the minority of districts that borrow through it.

Other uses of categorical grants are for very specific purposes and also only aid a small number of districts. These include paying districts extra funds to serve students who have transferred from recently dissolved districts and reimbursing districts some of the “transition costs” of merging with another district. Other grants refund districts that lose expected property tax revenue from designated, tax-free Renaissance Zones or land owned by the Michigan Department of Natural Resources. These add up to another $30 million in state funding to districts.

Additional categorical money is set aside to operate some of the state programs that service school districts. For instance, a handful of grants fund Michigan Virtual University, which develops and provides online courses; the Michigan College Access Network, which informs students of postsecondary options; and the Center for Educational Performance and Innovation, which collects, organizes and disseminates financial data about schools. Similarly, the state directs other grants to districts to help them cover the costs of administering the state’s standardized test and for the “collection, maintenance, and reporting of data to the state.”

Some categorical grants are handed out on a competitive basis. The 2016-17 state budget features bonuses for districts implementing year-round school or for participating in science and technology-focused student programs. Districts in western Michigan are eligible to apply for a grant that supports the purchase of “locally-grown fruits and vegetables.”

The Legislature also uses these funds to create incentives for districts to meet certain goals. For instance, districts can receive up to $60 for each student who completes a college dual-enrollment course and get grants to cover the costs for low-income students taking Advanced Placement and International Baccalaureate tests.

These are just some of the highlights of the various programs and initiatives that are funded through categorical grants. Other funding flows to districts through these grants for things like career and technical training, special education, early literacy programs, adult education and more.

The state’s foundation allowance represents just the beginning of state taxpayers’ financial commitment to public schools. Unlike the foundation allowance, categorical grants will come and go, and their budgeted amounts vary year to year, according to legislative priorities. But with a steady upward trend in their use, they form a key part of the comprehensive picture of how Michigan funds public schools.

Created more than 50 years ago, Michigan’s 56 intermediate school districts are an entrenched part of the K-12 public education landscape. But few people really understand what ISDs do, how they are funded and what value they provide taxpayers and students.

ISD responsibilities vary and their statutory role is broadly defined. Nevertheless, there are some common functions that ISDs perform across the state. Most ISDs, for instance, provide back-office support for local school districts, deliver or finance special education services and operate alternative and career education programs. Many also facilitate shared services among districts, such as technological needs, transportation, professional development and more.

ISDs are funded differently than local school districts and public charter schools. The primary difference is that ISDs do not receive the normal foundation allowance, the main per-pupil funding mechanism used to distribute revenues to school districts. Instead, ISDs are funded by a combination of local property taxes, a per-pupil special education foundation allowance, state categorical funds and federal grants. Reported ISD revenues totaled $2.77 billion in 2016.

ISDs have five different types of local property taxes to draw from. To pay for general operations, all ISDs collect funds from a voter-approved “operating millage.” There are designated local millages for special and vocational education services too. The rates for each of these three millages are capped based on what their rates were in 1993, before Proposal A took effect.

A small number of ISDs levy a “regional enhancement millage” of three mills or fewer, but it is actually revenue for each of the conventional school districts within an ISD’s boundaries and distributed on a per-student basis. The final type of local property tax ISDs can levy is for debt services — allowing them to finance building, remodeling and furnishing their facilities. Combined, these five local sources of taxes bring in nearly half of ISD revenues.

Another significant source of ISD revenue — amounting to about 30 percent of all their revenues — comes from the state treasury. While some of the dollars are distributed within various state budget line items, several distinct pieces are set aside for the 56 regional educational agencies.

First, the state supplements ISD revenue for special and vocational education in an effort to create more funding parity among ISDs. Using complex formulas, this money benefits ISDs that raise the least amount of revenue from their local property base. These “equalization” dollars guarantee that all ISDs will receive a minimum amount of revenue to fund these services — at least 75 percent of what they had received the previous year. These payments cost the state almost $50 million annually.

Graphic 2: Michigan ISD Revenue Breakdown: 2015-16

Source: National Public Education Finance Survey, 2015-16 data

A large chunk of state revenue for ISDs is a reimbursement for approved costs for special education services. This revenue is court-ordered: the Michigan Supreme Court ruled that the state needs to provide a certain portion of the funding for the mandates it creates for school districts to educate special needs students. ISDs collected more than $270 million for this purpose in 2016.

The current state budget allocates an additional $67.1 million to ISDs for complying with any other state requirements and providing “technical assistance to districts.”

The last piece of ISD funding is federal money, which makes up nearly one-fifth of ISD revenue. Some of this money is received by the state and then distributed to ISDs while other amounts are received directly by ISDs themselves. Federal money often comes in the form of grants for specific purposes, programs or services. Among them are funds designated to cover special education costs, to help homeless students or non-native English speakers, and to underwrite early childhood or community health programs.

ISD funding growth has outstripped that of local school districts and public charter schools. Between 2006 and 2016, the number of students enrolled in ISD programs has not changed much, increasing by just 2.6 percent. Meanwhile, total ISD operational spending has increased over the same period by 39 percent. Today, nearly 10 percent of K-12 operating dollars are spent by ISDs.

As demonstrated, ISD funding is complex, with revenue coming from a variety of different sources and targeted for a variety of different services. Although they are not often the first thing that pops into people’s head when they think of Michigan’s schools, ISDs consume a sizable chunk of taxpayers’ support for public education in Michigan.

A thorough review of how special education funding works in Michigan reveals the challenge of consistently and effectively providing these services. Like many other elements of school finance, special education funding is complex — revenues come from a variety of sources and are purposed for a variety of targeted programs. Altogether though, spending on these services comprise a large but difficult to measure portion of what Michigan taxpayers spend on public education.

The state’s recent $400,000 education finance study, or “adequacy study,” could not completely account for special education spending among districts, and recommended a better tracking system. Although an incomplete figure, the state reports that local districts spent $2.7 billion in 2016 providing special education services. This figure does not include certain expenses, including those already covered by federal dollars.

More than 197,000 Michigan students — about 13 percent of total public school enrollment — were classified as having special needs in 2016. The need for special services is determined by a student’s Individualized Education Plan. Most students with identified learning disabilities still spend a significant part of their time in a general classroom setting.

School districts receive a foundation allowance on behalf of each special needs student they enroll, just like they do for every other student. The foundation allowance provides schools with a minimum, per-pupil funding amount. Additional dollars help fund the special education services prescribed by a student’s IEP. But providing enough funds to cover all the special services called for by the plans for these 197,000 students is a challenge.

The bulk of the funding comes from local property taxes collected by one of Michigan’s 56 intermediate school districts. These entities are charged with overseeing and standardizing special education services among their constituent districts, and they also directly serve some special needs students. ISDs levy special education millages, one of the five types of millages they can levy on local property, to pay for the special education services they provide directly or that they pay other school districts to provide.

There is a cap on what ISDs can levy for their special education millage — it cannot exceed 1.75 times their 1993 rate, as approved by local residents. Since the amount ISDs raise through these millages depends on the value of the property in their district and these values differ greatly from ISD to ISD, there can be significant disparities in special education per-pupil spending among ISDs.

State funding helps alleviate some of these disparities, yet another layer of special education funding. Supplementing ISD millage revenues, a $37.8 million categorical provides lower-funded ISDs with extra funds. ISDs receive greater payments for having less valuable property to tax and higher local tax rates.

The state makes additional payments to fund special education as a result of a Michigan Supreme Court decision in the 1990s. The court order requires the state to pay local districts and ISDs for about 70 percent of transportation-related expenses and 29 percent of all other approved, special education expenses. The state has set aside about $910 million to ensure all public schools are reimbursed at these court-ordered levels.

However, for a tiny fraction of special education students — typically those placed in an institution by a court or state agency — the state reimburses districts for 100 percent of approved expenses. This cost the state about $10 million in 2016.

A handful of districts receive another layer of funding: so-called “hold-harmless” payments. These payments guarantee that these districts’ special education funding doesn’t fall below their 1997 levels. The total hold-harmless obligation budgeted by the state for 2017 is a little more than a million dollars.

While the combination of state and local allocations outlined above represent most special education funding, federal funds support these services too. The lion’s share of federal funds for special education come from the Individuals with Disabilities Education Act and the Medicaid-funded School Based Services. Michigan’s total federal allocations for these two programs were $370 million and $110 million in 2017, respectively.

Any remaining special education costs are covered out of the general fund of a local district, charter school or ISD. Previous research has estimated that general fund dollars finance between 20 and 25 percent of these expenses. Much of the difficulty in providing a precise determination or comparison of total special education spending results from this “cross subsidy” of general-use dollars.

The complete picture of Michigan special education financing remains difficult to assess. Since these programs are largely administered and funded locally, a thorough review would require investigating each of the 56 ISDs individually and perhaps each of the 540 districts and 300 charter schools as well. Nevertheless, the many pieces of funding that can be observed highlight the difficulty of matching dollars to student needs.

Though the number of students attending public schools in Michigan has steadily declined, many schools still face a challenge financing facilities that ensure students are served in a safe and effective environment. Unlike funding the operational costs of running a school, the state plays only a small role in financing school buildings and amenities. Instead, the onus falls largely on school districts’ local taxpayers to provide for capital needs.

While Michigan law allows school districts to use up to 20 percent of the funds they receive through the state’s foundation allowance to finance capital projects, it is very rare for districts to use their main operational funding source for these purposes. Instead, school districts typically borrow money to pay for building and remodeling facilities. According to the U.S. Department of Education’s latest tally, Michigan school districts owed a combined total of $17.8 billion in long-term debt as of June 30, 2014.

(It should be noted that public charter schools do and must use their foundation allowance revenue to finance their facilities costs. This is because, unlike conventional school districts, charter schools cannot levy taxes on local property to finance borrowing through bonds. Therefore, the discussion that follows applies only to conventional school districts.)

Local school boards are legally authorized to take out debt through resolution bonds. The way it works is that districts sell bonds and then levy a tax on local property to pay off the principal and interest owed on the bonds over time. There are limits on how much districts may borrow without asking voters: A district’s combined debt cannot exceed 5 percent of the total “state equalized value” of property located within the district. SEV typically refers to half the assessed market value of a home or business.

In order to raise taxes to pay for construction debt, a school district must receive majority approval from local voters. State law mandates the information and type of language that school districts must use when asking voters to approve of their borrowing and taxing. More than 85 percent of Michigan school districts actively charge taxpayers to pay down various outstanding debts, according to an April 2016 report.

Most states offer school districts some sort of direct aid for facility expenses through reimbursements, matching grants or other appropriations. Michigan is somewhat unique in not offering direct financial aid for capital expenditures. But the state does provide aid to districts for financing their facilities in other ways.

Michigan allows districts to have their debt “qualified” by the state. A qualified loan is one that can use the state’s credit rating, which is almost always more favorable than the rating an individual school district could get and usually translates to lower interest rates and borrowing costs. Essentially, the state guarantees its “faith and credit” that if the district fails to make its payments, the state will come in and bail it out.

This is accomplished through the state’s School Bond Qualification and Loan Program. In addition to using the state’s credit rating, districts can borrow from this program to make bond payments, if their local millage is not sufficient to cover these costs. In order to be eligible for borrowing through this program, school districts must levy at least a seven-mill property tax and agree to complete repayment within six years of having paid off their original bond.

Perhaps because the costs of this program steadily increased over the years, the Legislature enacted reforms in 2012. These capped the amount the state would lend out in qualified debt to $1.8 billion and tightened repayment deadlines, among other things. As of July 2016, 132 school districts owed the state a combined $924.4 million, down from $1.7 billion in the two years previous.

Districts that don’t want to fill out the paperwork or abide by the state’s terms for qualified borrowing can gain voter approval to issue “nonqualified” bonds for capital projects instead. However, the total debt for those voter-approved bonds is limited to 15 percent of SEV, or three times more than can be issued by a simple school board vote. The total debt limits do not apply to state-qualified bonds.

An additional tool available to school districts to fund capital projects is a so-called sinking fund. These were originally established as separate “savings accounts” for certain projected facility costs. Sinking fund levies cannot exceed three mills or last more than 10 years (prior to 2016, these limits were five mills and 20 years). These funds can be used to buy land, build or repair facilities, install infrastructure for technology and security as well as purchase computer equipment and software. About 30 percent of school districts use voter-approved sinking funds, most of them at a rate lower than three mills.

A key distinction to remember about financing school construction is that it operates differently than most all other funds districts have available to them. Instead of flowing from a variety of sources and appropriated annually, money for capital costs is borrowed by school districts and paid back with funds raised from local taxes, with the state playing only a supporting role for these projects.

The primary source of public school operating revenue used to be local property taxes. Over the past several decades, however, funding formulas have been rewritten and now schools in Michigan get a majority of their funds — about 60 percent — from the state. In addition, a larger portion of school revenue comes from federal sources than used to: Almost 10 percent of total funds today come from Washington, D.C. Despite this, federal dollars are often overlooked in discussions of school funding.

Federal allocations for public schools tend to fluctuate more than state or local revenues. In recent years, though, Michigan’s annual share of K-12 education dollars from D.C. has hovered around $1.8 billion.

The lion’s share of federal funds is distributed through the state of Michigan, though local schools can receive money directly from the nation’s capital. Funds appropriated via Lansing are easier to tabulate because the expected sums are factored into the state’s budgeting process. Most of Michigan’s state-appropriated federal K-12 dollars fit into one of three major buckets.

The first major share of federal funds comes through Part A of the federal Title I program, designed to provide financial assistance to schools serving low-income students. These grants, totaling nearly a half billion dollars in 2017, are given to local districts and charter schools, based on a series of formulas aimed at providing extra dollars to schools with high concentrations of students in poverty. They are intended to supplement local and state dollars targeted for the same purpose.

Next, more than $500 million a year in federal funds are used to finance the National School Lunch Program. While designated state dollars cover a small share, the U.S. Department of Agriculture reimburses the bulk of Michigan schools’ costs for providing low-income students with free or reduced-price meals.

Third, the Individuals with Disabilities Education Act sets federal standards for serving students with recognized special learning needs. Though state and local dollars cover a majority of these costs, the U.S. Department of Education contributed $370 million in 2017 for this purpose. Michigan’s intermediate school districts also take in $110 million from the federal Medicaid program to help finance health-related services for low-income, special needs students.

Michigan schools also receive federal funding for about a dozen other purposes. This combined remaining share is smaller than the three major buckets. Dollars to enhance teacher preparation and recruitment, commonly known as Title II funds, reach all local school districts and charter schools, but are divvyed up to give extra support for schools serving students in poverty. More than $80 million of federal money allocated through the Michigan Department of Education can be used for educator professional development and mentoring, recruitment incentives or merit-based awards for teachers.

Federal money is also directed through the state in the form of School Improvement Grants which are aimed at fixing failing schools. Smaller amounts of federal funds support the learning needs of English language learners, migrant students and homeless students. Special programs focused on math and science, as well as career and technical education, are also beneficiaries of federal money.

Other federally funded grants underwrite some of the compliance costs of mandated standardized tests, as well as school-based substance abuse and violence prevention programs. A modest per-student federal subsidy is also provided to 93 rural and low-income districts and charter schools.

Federal funds have an impact on school budgets and programs. Using restricted support and targeted grants, the federal government supports programs that serve certain types of students. While federal monies still represent a small portion of total school revenue, they yield a growing impact on how schools operate.

The complexity of Michigan’s school funding system, relying on a variety of revenue streams, multiple funding formulas and statutorily defined and targeted grants and programs, has been the focus of this series. Stepping back and looking at how all of these pieces work, one can make a good case that there is not one system that funds public schools in Michigan, but rather a number of different programs created over time that have been layered on top of each other.

School funding in Michigan is a result of many different policy decisions made at different levels of government. As a result, there’s no unifying strategy used to fund schools, although certain types of funds have very specific purposes. This makes understanding (let alone improving!) school funding in Michigan a significant challenge for parents, taxpayers and policymakers.

Debates over the adequate level of K-12 funding levels should be informed with meaningful and valid information. A 2016 poll of more than 4,000 American adults found that support for increased funding of “public schools in your district” dropped from 61 to 45 percent when respondents were told how much their district was spending.

The average Michigander struggles with keeping up with how much their local school district is spending, too. The most detailed, comprehensive and accessible accounting of how much money Michigan schools take in and spend comes from the U.S. Census Bureau’s National Public Education Finance Survey.

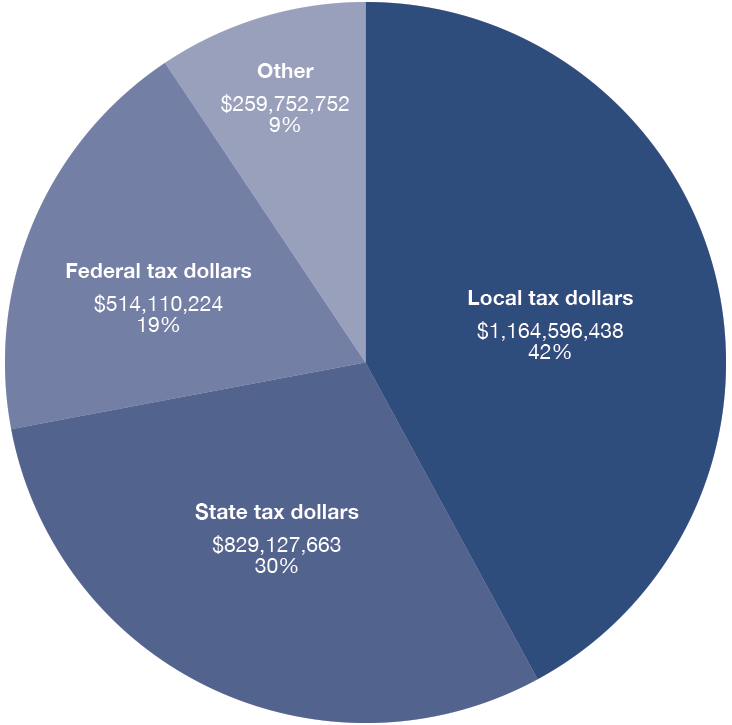

There are several ways to measure the overall financial picture of Michigan public schools. First, the total dollar intake, which in 2016 was $19.84 billion, or $14,307 for each full-time-equivalent student. These revenues roughly break down as follows:

The second vital measurement is total dollars spent during a given school year. In 2016 traditional school districts, intermediate school districts and public charter schools combined to spend $18.5 billion, or $13,333 per FTE pupil.

A more meaningful way to compare spending changes over time is a look at total current expenditures. These figures reflect primary operational costs and exclude money spent on capital construction projects and interest payments on borrowed funds, as well as adult education and community programs.

Current expenditures in 2016 totaled $16.98 billion, a rate of $12,243 for each full-time student. About 75 percent of traditional districts and 45 percent of charters spend more than $10,000 per student.

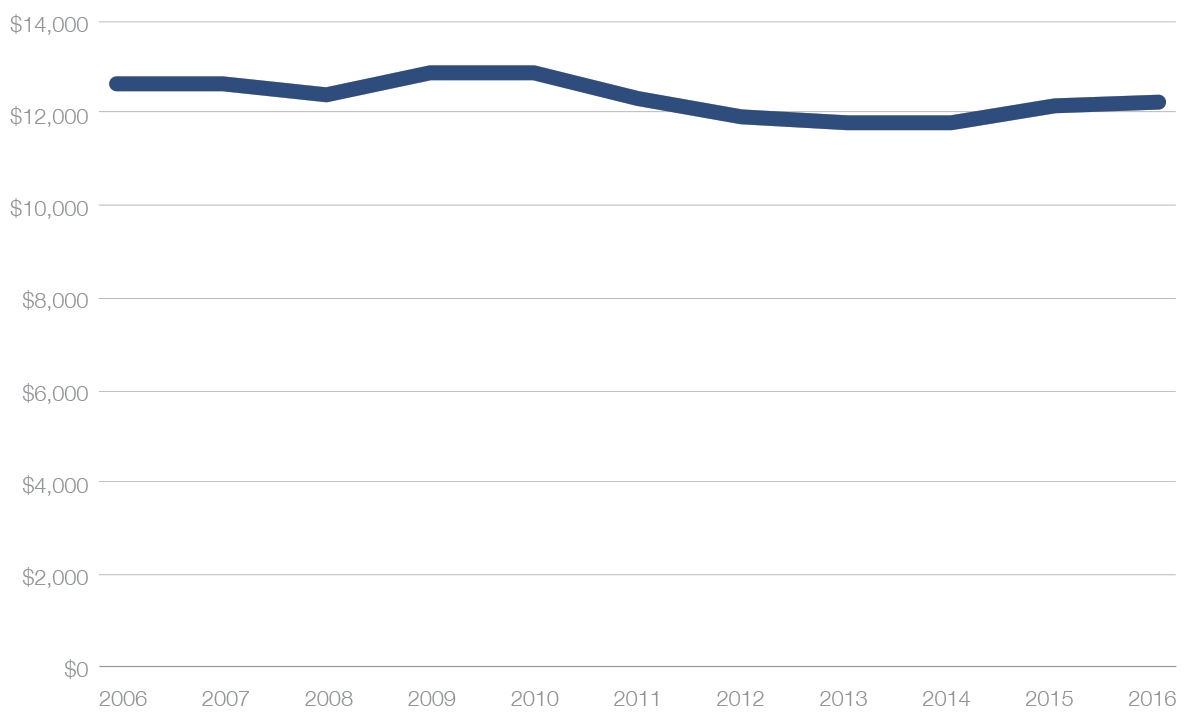

Graphic 3: Michigan: Current Expenditures Per FTE Student, 2006-2016 (in 2016 dollars)

Source: Bureau of Labor Statistics, Michigan Department of Education

Adjusted for inflation, Michigan K-12 current per-pupil spending has not changed much over the past decade. Expenditures edged up to their peak in 2009 and 2010, before losing some ground following the recession and the reduction of extra federal “stimulus” funding. From 2014 to 2016, per-pupil spending increased by 3.3 percent in real dollars, approaching 2011 levels of purchasing power.

Michigan public school enrollment also declined by nearly 12 percent over the last decade. The foundation allowance, which provides the majority of resources for school districts and charter schools, is distributed based on how many students a school enrolls. Many districts struggle to manage their fixed costs in these times of declining enrollment. But for each student served, the overall level of funds available has been mostly steady.

Money clearly matters in education, but probably only up until to a point. Resources are needed to retain the services of great teachers and support systems. And certainly, some students will require more resources to educate than others. But most education research suggests that just adding more money to the existing system is unlikely to boost student achievement in any meaningful way.

Part of the reason for this is that it’s hard to prescribe the optimal way schools should spend additional dollars. For instance, they might need to spend it on just meeting the burdens of certain state and federal regulations or on providing their current employees with more generous salaries and benefits. These certainly increase costs, but they don’t necessarily improve instructional quality.

Perhaps additional funds would be used to hire more teachers or other staff, update textbooks and other materials, or provide additional services. Any one of these may help produce better results for students, especially if there is a current deficiency in these areas. But just giving schools more money is unlikely to improve the state’s academic performance. A 2016 Mackinac Center multiyear analysis of building-level data found no connection between higher spending levels and better results on 27 of 28 different tests and other academic measures.

Even the state’s $400,000 Education Finance Study, better known as the “adequacy study,” claimed to have found a modest connection between additional spending and higher test scores. But given the current achievement levels, boosting spending with no other changes wouldn’t amount to much. For example, according to the study, an additional $6 billion would only improve scores so that just half of Michigan third graders are on grade level in reading and just one-third of high school juniors are proficient in math. That’s a hefty bill just to meet these low bars.

Even so, finding $6 billion to generate modest learning gains would require some combination of repurposed state budget dollars and additional taxes on Michigan residents and workers. And even if we did have that extra money, our complex, multilayered, patchwork funding system would make it difficult to figure out the optimal funnel to sink that money into.

A glimpse at the full picture of the state’s school finances should adjust the focus from arguing about the right amount of money to spend on schools to instead figuring out how best to use the resources that are already available. It’s a lot harder to determine how to optimize resources compared to just dumping more money into the system, but a necessary first step is understanding the system as it exists. Only then can we work to figure out how to improve it for the betterment of schools’ number one priority: student achievement.