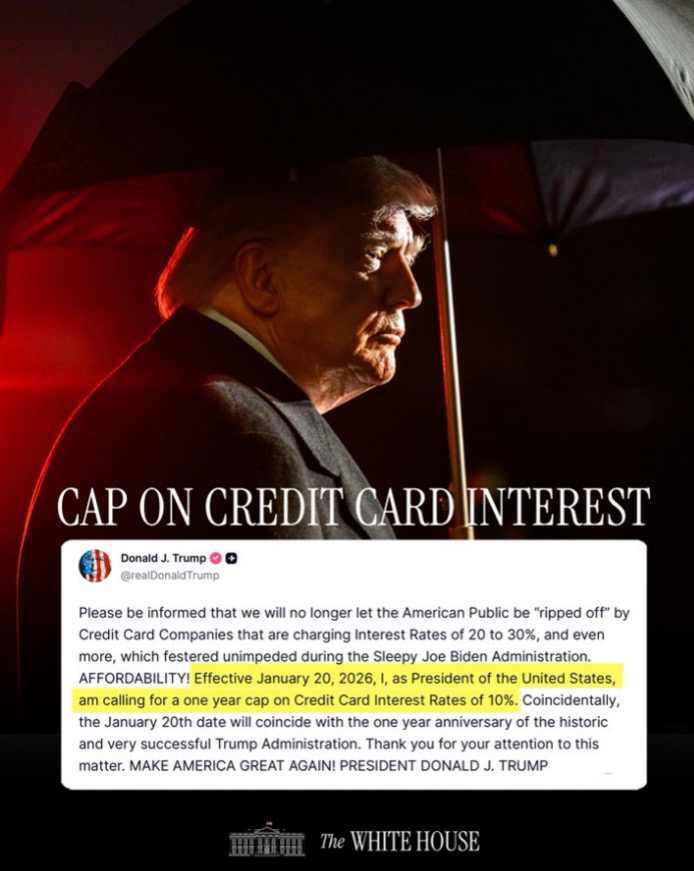

President Trump recently urged Congress to cap credit card interest rates at 10%, arguing that rates of 20% or 30% are abusive and that the government should step in to protect families.

The good news is that, at least for now, many Republicans in Congress are pushing back. Lawmakers are warning that government price controls on credit would restrict access and hurt consumers rather than help them.

That skepticism matters because this debate is bigger than one proposal. It reflects a deeper misunderstanding about how credit markets work and why controls on the price of credit consistently fail.

Credit exists because lenders take risks. Some borrowers repay on time. Some don’t. Some have stable incomes. Others don’t. Those differences are real, and they matter.

Interest rates exist to reflect that reality. They are prices, not moral judgments. They reflect the time value of money, the risk of nonpayment, inflation, and opportunity cost. Lending money today means it cannot be used elsewhere tomorrow.

Capping interest rates does not remove risk. It prevents risk from being priced. When that happens, lenders don’t lend more. They lend less, especially to those who need it the most.

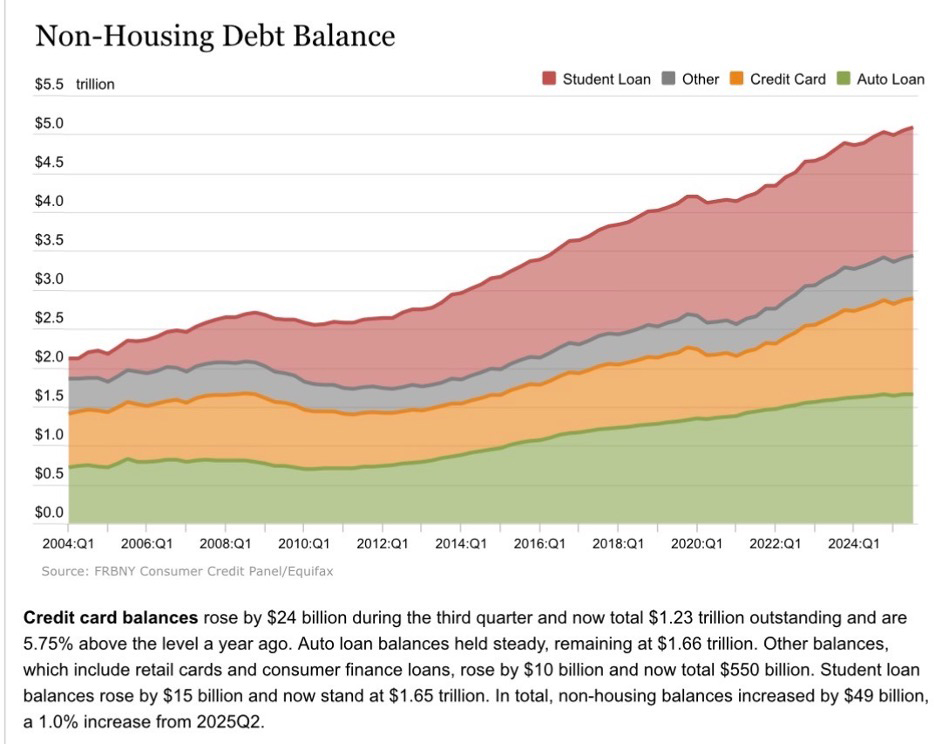

Supporters of rate caps often point to the amount of debt Americans carry. According to the Federal Reserve Bank of New York’s Household Debt and Credit data, total household debt is about $18.6 trillion, including roughly $1.2 trillion in credit card balances, which make up about 20 percent of all non-housing debt.

Source: New York Fed

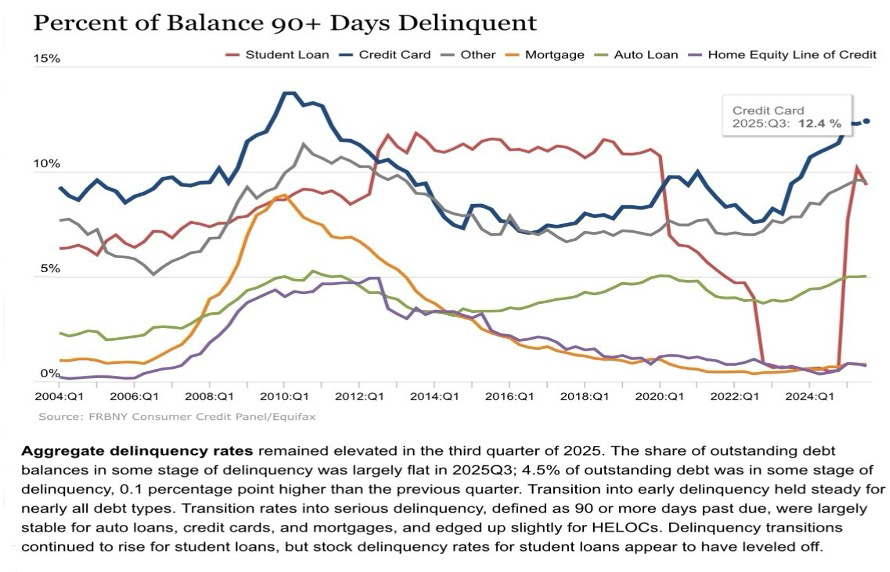

Those numbers are large, but large numbers alone don’t indicate failure. What matters is whether borrowers are defaulting at alarming rates. An increase in unpaid and overdue balances would indicate that creditors were encouraging people to take on too much debt.

On that front, the picture is serious but not catastrophic. About 12.4 percent of credit card balances are seriously delinquent, meaning they are 90 or more days past due. That’s higher than during the pandemic and near levels seen during the 2007-2009 recession.

Source: New York Fed

But here’s the key point: there were no interest-rate caps during the financial crisis or the pandemic, and the credit card market did not collapse. Lenders adjusted. Borrowers repaid over time. The system absorbed the shock without government price controls. So what market failure would a cap on interest rates correct?

Attempts to control interest rates are nothing new. For centuries, governments imposed usury laws because they viewed interest as unfair. The results were predictable: fewer loans, less access to credit, underground lending, and worse outcomes for people with the fewest alternatives.

As people better understood the time value of money, strict caps faded away. Risk-based pricing replaced them. Lending became more transparent and more widely available. Modern credit cards are a product of that evolution.

Today, more than 80% of U.S. households have at least one credit card, and 82% prefer using a credit card for purchases, according to Federal Reserve survey data. That access didn’t come from government mandates. It came from competition, innovation, and flexible pricing.

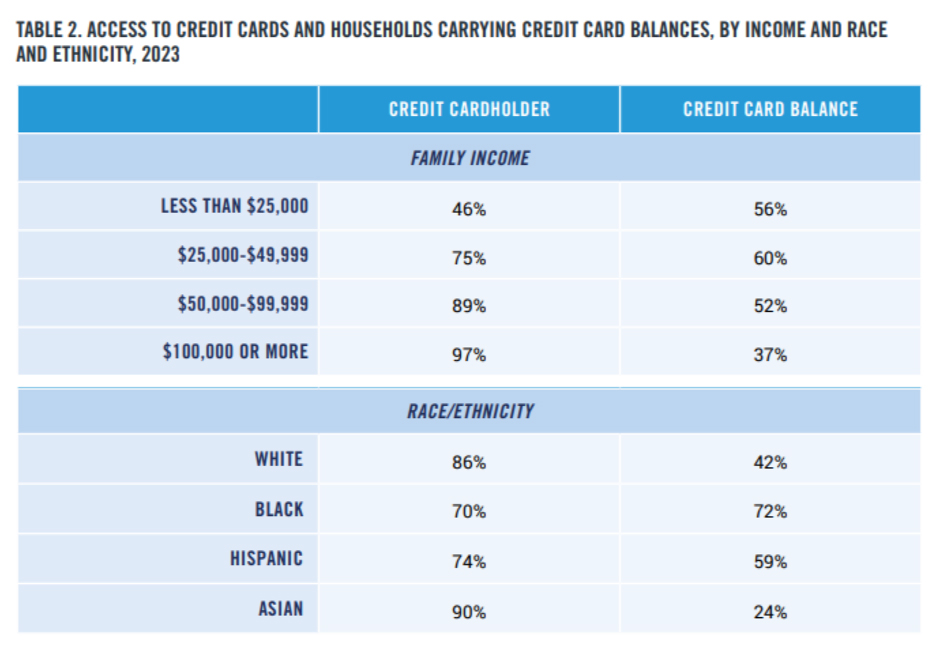

But access isn’t equal. Lower-income households are less likely to have credit cards, and when they do, they’re more likely to carry balances—especially during emergencies. These are the very consumers politicians claim to protect. Interest-rate caps would price them out of the credit market.

Source: Committee to Unleash Prosperity

Credit cards are expensive to operate. As outlined by the Committee to Unleash Prosperity, lenders face roughly 4% in capital costs, 6% in expected credit losses, and about 5% in administration and collections—more than 15% in costs before earning any return.

A 10% cap would guarantee losses.

When losses are guaranteed, lenders respond logically. They tighten credit standards. They lower limits. They close accounts with limited credit history. Credit becomes concentrated among the safest borrowers.

That isn’t punishment. It’s arithmetic.

Trump is not alone in promoting ideas that would worsen the credit market. Congress is considering the Credit Card Competition Act, which would impose government mandates on how credit card transactions are routed. Supporters claim it would lower costs. In reality, it functions as another form of price control.

These mandates would reduce the revenue lenders currently use to fund fraud protection, security, and rewards programs such as cash back and travel points. Those rewards don’t disappear evenly. They disappear first for everyday cardholders and small businesses. High-credit, high-balance users are protected the longest. Price controls don’t remove costs. They hide them and shift them.

Supporters of these policies often argue that consumers make poor decisions and need protection from themselves. But economic choices are subjective. What looks irrational from the outside may be entirely reasonable given someone’s constraints or priorities.

We cannot observe the outcome of other choices. We don’t know which option a borrower rejected. Assuming the government knows better than individuals isn’t economics. It’s paternalism.

The bottom line is that price controls don’t work. They don’t work for housing, labor, or energy —and they don’t work for credit.

Capping interest rates and dismantling payment networks won’t make credit cheaper for everyone. They will make credit scarcer, reduce benefits, and limit options — especially for the people who rely on credit the most.

We already know how this story ends. Repeating it won’t protect consumers. It will leave them with fewer choices than before.

Get insightful commentary and the most reliable research on Michigan issues sent straight to your inbox.

The Mackinac Center for Public Policy is a nonprofit research and educational institute that advances the principles of free markets and limited government. Through our research and education programs, we challenge government overreach and advocate for a free-market approach to public policy that frees people to realize their potential and dreams.

Please consider contributing to our work to advance a freer and more prosperous state.