Corporate Welfare Summary

The state of Michigan operates a variety of select business subsidy programs that intend to create jobs and economic growth. Research shows, however, that most such corporate welfare programs are ineffective. And they come at a cost: the next best alternatives for that money — fixing roads or cutting taxes, for instance — are far more likely to create jobs and generate a positive return on investment for taxpayers. This in addition to the fact that it’s just plain unfair to take money from everyone and hand it out to a favored few through the force of government.

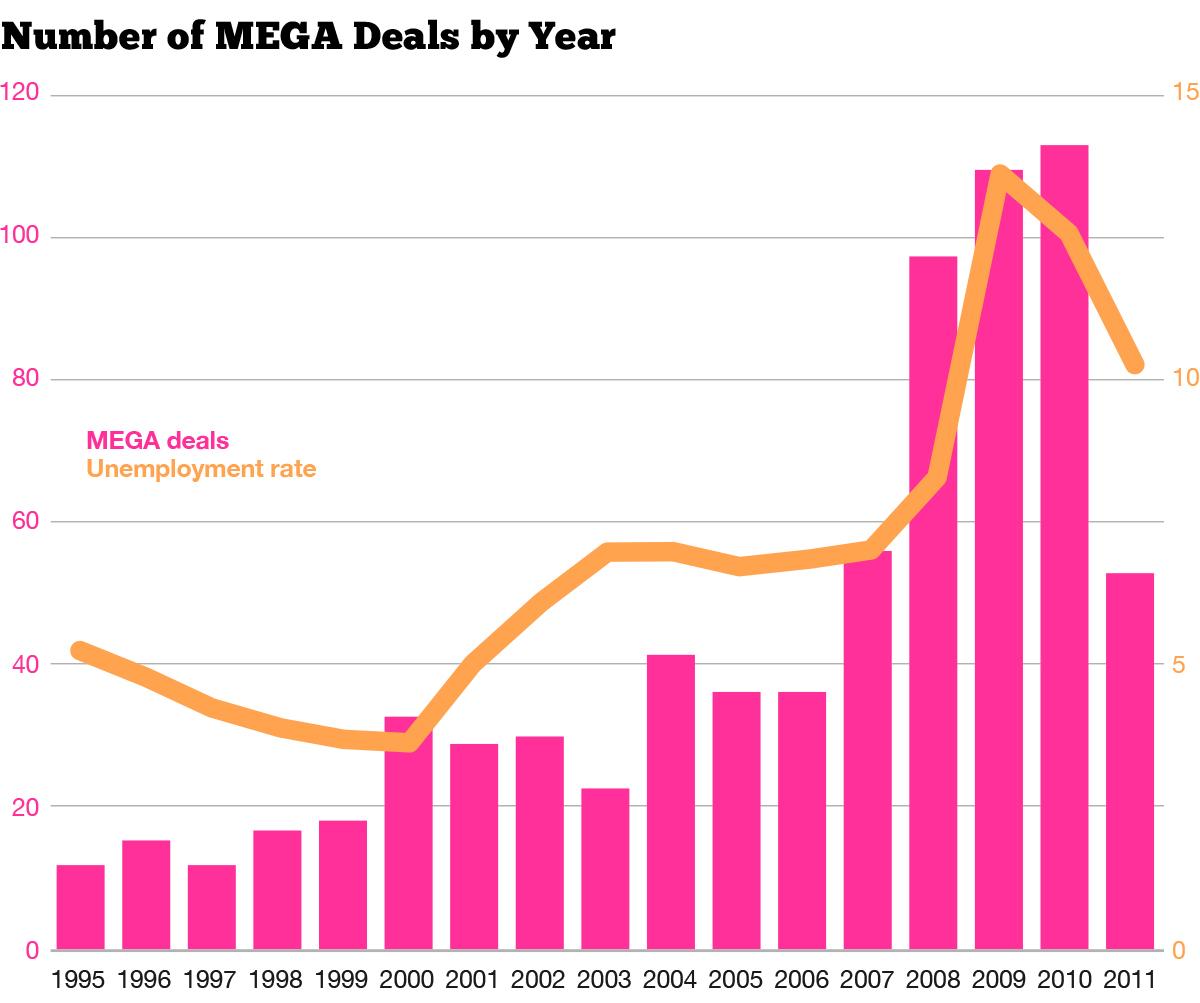

Michigan has a history of corporate welfare failure. The state offered $14 billion to select companies through its Michigan Economic Growth Authority tax credit program between 1995 and 2011. Four of five scholarly studies of the program found it had no effect or even a negative effect. Even though the program was shuttered, the state is still paying out more than $750 million in 2017-18 for tax credits promised through MEGA.

From 2008 to 2015, the state dished out $500 million for film incentives, but could show no new growth in film jobs for it. An empirical analysis of the state’s Michigan Business Development Program found that the $157 million in subsidies and loans disbursed from 2012 to 2016 was associated with a decline in jobs. Also, by the authors’ count, as many as one-third of the companies approved for support by the program had been or were in some sort of default or had been dismissed.

In the 2018 fiscal year, the state appropriated $268 million to the Michigan Strategic Fund for staff and program support. The MSF is in charge of most state economic development programs, with an assist from the Michigan Economic Development Corporation. In addition, payments from Indian gaming revenues to the Michigan Strategic Fund totaled more than $57 million in 2017. These revenues are not appropriated by the Legislature.

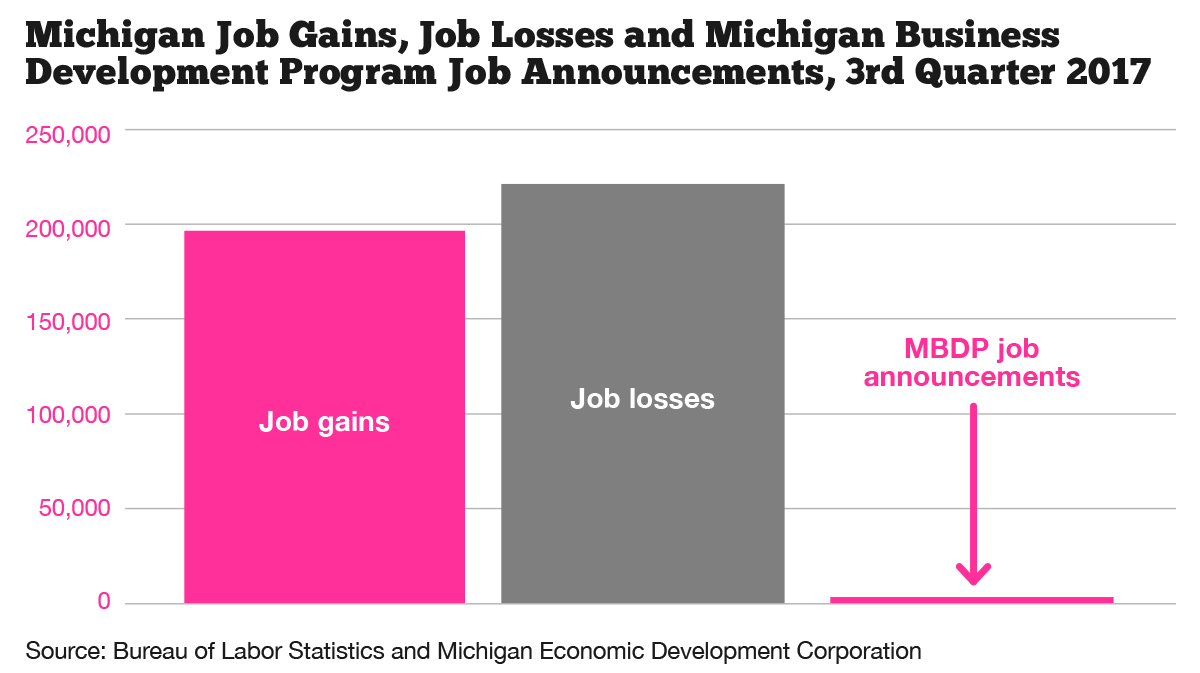

Even if all of the spending done by the state in the name of economic development was as effective as the state claims, it would not make much of a dent in the state’s vast economy. Data from the U.S. Bureau of Labor Statistics showed, for example, that in the third quarter of 2017 Michigan’s economy created 196,700 jobs. During that same time frame another 221,400 jobs were lost. During that quarter, the state announced that its Michigan Business Development Program may someday create 3,700 jobs at 23 of its state subsidized projects, only a tiny fraction of all the jobs created without any specialized treatment.

Income Tax Summary

In contrast to state bureaucrats trying to pick economic winners and losers, cutting taxes across the board could really spur Michigan’s economy. This reform would save citizens money and make Michigan an opportunity state.

The economic research demonstrating a link between taxes and growth is strong. A review of studies, published by the John Locke Foundation, indicated that lower taxes tend to lead to stronger economic growth at the state and local levels. Their review, titled “Lower Taxes, Higher Growth,” was a review of 681 academic, peer-reviewed journal articles, 115 of which involved state and local taxation. Of the 115 studies, 63 percent show “tax burdens were negatively associated with economic performance.” That is, most studies found that higher taxes harmed state and local economic growth. Only 3 percent of the studies showed a positive outcome.

The American Legislative Exchange Council publishes “Rich States, Poor States” each year, which includes economic performance and economic outlook rankings of the states. These rankings include 15 policy variables such as tax and minimum wage rates as well as a state’s debt service burden and workers’ compensation costs, to name a few.

The report compares the nine states that have no earned income tax to both the 50-state average and those states with the highest earned income taxes. They found that states with no income tax outperformed the 50-state average and the states with the highest income taxes, in terms of population growth, employment growth and personal income growth from 2006 to 2016. The only area in which the states with no income tax lagged the 50-state average or high earned income tax states was in gross state product, the value of all the goods and services produced within a state’s geographical borders.

Elected officials face pressure to “do something” to improve the economy. Instead of taking money from everyone to give to a politically favored few, the state should take a “fair field and no favors” approach to economic development. By eliminating Michigan’s corporate welfare apparatus and dedicating its revenues — and perhaps others — to tax cuts, we can give everyone a chance to create jobs and invest more, not just the people that get special treatment from Lansing.

What department or agency is responsible for the state’s economic development programs?

The Michigan Strategic Fund is responsible for the state’s economic development programs, with the cooperative efforts of the Michigan Economic Development Corporation. As one example of their cooperation, it is the MSF board that approves subsidies for Michigan Business Development Program projects. It is the MEDC, however, that recommends the projects to the board.

Is the Michigan Economic Growth Authority program still approving tax credit deals?

No. But the deals signed with companies in the past are still costing Michigan taxpayers a princely sum. In 2016, legacy costs associated with MEGA deals alone cost the state treasury $924 million. To put that in perspective, the entire Corporate Income Tax revenue for the year was $930 million. In other words, MEGA cost the state nearly all of its business tax revenue.

Why do lawmakers continue to run business subsidy programs if they’ve been ineffective?

Politicians are expected to “do something” to create jobs and improve the economy. Business subsidy programs enable lawmakers to point to a concrete example — the programs themselves and subsequent ribbon-cutting ceremonies — of heeding this demand. Attaching their names to new job announcements, business expansions and all the media hype that goes along with these developments entices many politicians to support these programs. And, of course, voters back home won’t really know if the program actually succeeded at improving the economy — but they might remember the politician at the front of the ribbon-cutting ceremony. But there is a lot of evidence — and from scholars with no dog in Michigan’s fight — to show these programs are typically not effective. Indeed, the programs may even retard economic growth.

Since other states offer business subsidies mustn’t Michigan too?

Proponents of select business subsidy programs say that if we stop corporate welfare, Michigan will find itself at a competitive disadvantage compared to other states. But this is only true if the programs actually work. They don’t, on net, and ending them will have little effect on the state’s economic well-being. Academics often disagree about the efficacy of particular policies, but the majority of scholarship seems pretty clear about state and local corporate welfare programs. Handouts designed to improve job or economic growth are largely ineffective.

Are taxpayers owed a tax cut?

In 2007, during 11th-hour negotiations to fill a budget gap, politicians increased income tax rates “temporarily” by 11.5 percent, bumping the rate from 3.9 to 4.35 percent. Part of the deal was to gradually roll back the tax to 3.9 percent. That never happened. After permitting a 0.1 percentage point cut, the state income tax rate was frozen at 4.25 percent, effective on January 1, 2013. Taxpayers would be justified in claiming this was a form of “bait n’ switch” and that income tax rates should be rolled back to at least 3.9 percent.

Has any attempt been made to roll this back?

Yes. In 2017, a bill was introduced to roll back taxes by 0.1 percentage points in 2018 and again in 2019 and then possibly more, depending on revenues flowing into the state treasury. The bill was defeated.

Can the state afford an income tax cut?

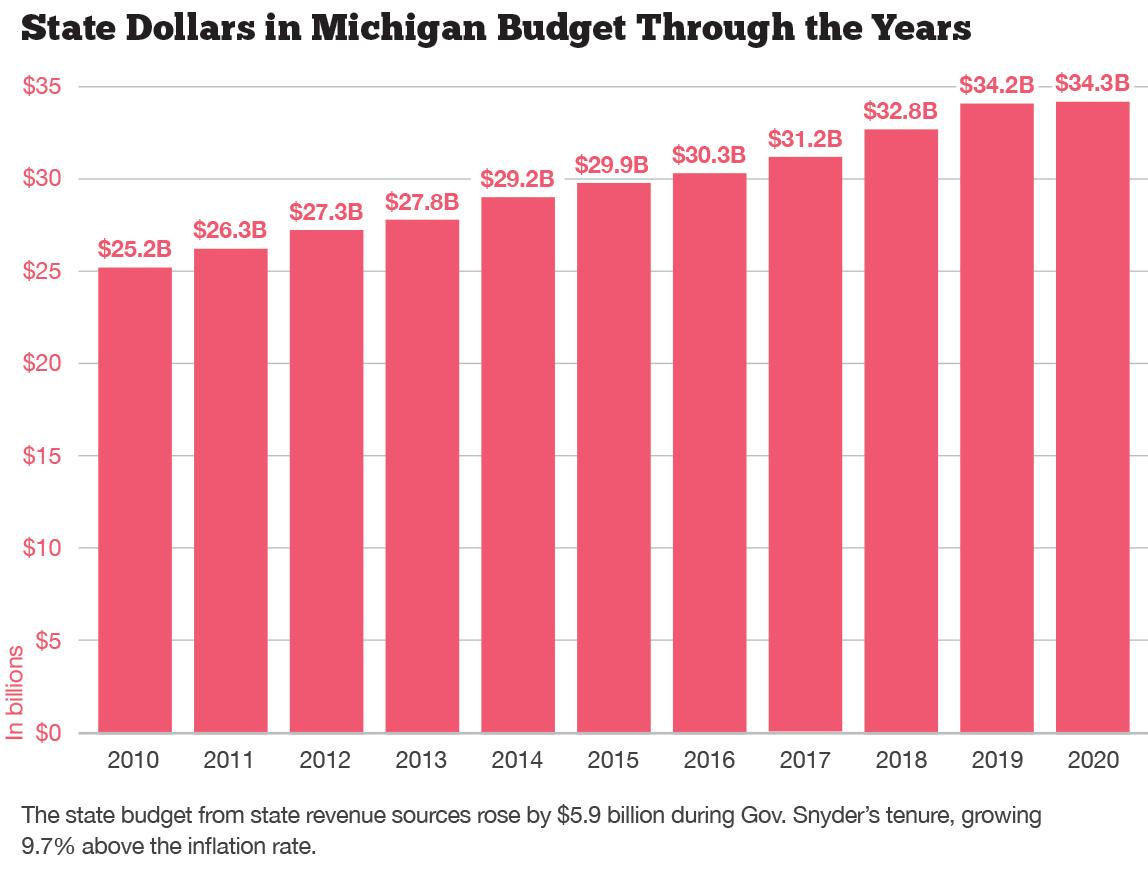

Yes. The fiscal 2018 budget contains $32.1 billion in revenues from state sources, up $5.9 billion since fiscal 2011. This growth is above the inflation rate during that period.

Where should the state trim its budget to pay for an income tax cut?

The first thing to go should be ineffective business subsidy programs and perhaps other line items in the Michigan Strategic Fund budget. This could ultimately free up about $200 million. That won’t finance a personal income tax cut from 4.25 percent to 3.9 percent, but it is a good start. The Mackinac Center for Public Policy and other organizations have recommended billions worth of budget reforms in the past. Those ideas could be plumbed for savings. In addition, if the economy continues to grow, the state may end up with more revenue even at a lower income tax rate.

The failures of the state to effectively subsidize individual companies or industries are numerous.

The film studios of Hangar 42 in West Michigan and Unity Studios in Allen Park both ended in scandal. A123 Systems and LG Chem were subsidized battery companies that went bankrupt. Renewable energy projects featuring the old Ford Wixom Plant, GlobalWatt, Dow Kokam and Suniva all flopped.

More recently, under the current Michigan Business Development Program, Cherry Growers, a company near Traverse City, was approved for millions of subsidies through the state’s Michigan Business Development Program and projected to create 72 jobs. Instead, it went bankrupt and is being liquidated.

Spiech Farms, another MBDP recipient in West Michigan, was approved for $220,000; it filed for bankruptcy less than a year later.

RNFL Acquisition, Inc. also received a MBDP subsidy and was expected to create 27 new jobs. It ultimately laid off its employees in 2016 and its assets were sold off in a proceeding similar to a Chapter 7 bankruptcy. An MEDC spokeswoman told the Mackinac Center that the company’s subsidy would not be paid back, despite its failure. “We have not received any repayment, and at this point don’t expect that we will. The asset sale was not sufficient to cover all of the creditors, including MSF,” she said via email. And these are just a few of the examples of the state’s failure to invest taxpayer dollars wisely, and from just one program.

These stories underscore the inability of state employees to accurately place bets on the right horses. But even when companies that get state aid add jobs and expand, this may very well have happened without state support. There is just no direct, real way to tell, so state bureaucrats get to claim that they were responsible for this new economic activity even if they were simply doling out favors to a company that was going to expand anyway. One analysis of state and local incentives suggests that as few as 6 percent of deals “might tip the location decision” of businesses.

The list is long of companies that the state has given incentives to that have failed to create the jobs they promised. This is true for many different economic development programs. Indeed, the list of promises made but not kept goes beyond the scope of this document, but many — from the Michigan Pre-Seed Capital Fund to the Brownfield Redevelopment Financing Program and Michigan Economic Growth Authority — can be found on the Mackinac Center’s website at www.mackinac.org.

Even when state programs and the companies they incentivize perform as good as or better than projected, they remain an unfair use of state resources. One egregious example of this that the Mackinac Center profiled in 2000 involves Koegel Meats. This family-owned business has been in Flint for more than a century — through good times and very bad ones — and without incentive deals. Imagine the owners’ surprise then when they learned that the state offered a competitor — Boar’s Head Meat Provision — a $5.1 million incentive package to expand its operations into Michigan. It is fundamentally unfair of state bureaucrats to effectively take money from Koegel Meats and give it Boar’s Head, but that was the practical effect.

The government has nothing to offer these companies that it doesn’t first take from someone else. This is an expensive transfer from the many to the few. There are more than 200,000 business establishments in Michigan. Lansing bureaucrats simply do not have the ability to pick winners from losers in the marketplace and subsidize the winners, particularly in a way that creates more wealth than would otherwise occur without their interference.

Michigan remains mired with middling ranks among competing states in current and future economic well-being, according to several measures. The good news is that our recent recovery has been a positive one but there is more to do. The state has not completely recovered economically from its one-state recession that effectively lasted from 2001 to 2010. Indeed, Michigan’s payroll numbers are down nearly 263,000 since the 2000 peak.

Michigan was the only state in the union to lose population on net balance during the 2000s. From 2000 to 2009, Michigan saw one of the worst per capita personal income drops of any state since the Great Depression. From 2006 to 2009, we led the nation in people moving out of the state as measured by the percentage of moves by United Van Lines, the nation’s largest mover of household goods and services. Outbound traffic made up a higher portion of the company’s business in Michigan than in any other state in the lower 48 states. Mackinac Center research has shown UVL data to be very highly correlated with actual Census data. The number of people receiving food assistance and other government benefits skyrocketed.

Things have improved since our economic nadir but we are still losing population to net domestic migration, just more slowly. If we want to make Michigan a destination state again, we have to make it an opportunity state again. We do that by making it less costly to work and live in Michigan. We do that by rolling back the state personal or corporate income tax and leveling the playing field for businesses.

For the first decade of the 21st century, the Michigan Legislature’s policy direction was to try to centrally plan Michigan to economic prosperity.

The Legislature took more from individuals and small businesses through higher income and business taxes, and increased excise taxes on goods such as tobacco. The state’s corporate welfare arm, the Michigan Economic Development Corporation, was expanded, transferring ever-larger sums from taxpayers to politically connected firms through tax breaks and subsidies. By nearly all measures, these programs have been a colossal failure.

But now Michigan is back from the brink. In the second decade of the 21st Century, legislators cut business taxes and scaled back some corporate welfare. Lansing eliminated project labor agreements and eliminated prevailing wage, both of which decreased the cost of government construction. Lawmakers also shored up public pensions and right-sized other government employee benefits, reducing the size and cost of government. And Michigan became the 24th right-to-work state.

While the state has improved, there’s more to do. There is general agreement among economists and public policy groups with activists on both sides of the political spectrum that lawmakers should get out of the business of subsidizing some businesses and industries at the expense of others. Michigan should eliminate all of its corporate welfare programs and get out of the business of trying to pick winners and losers.

Instead, policymakers should take a “fair field and no favors” approach to economic development, reducing taxes for everyone across the board — starting with the state income tax. This will help unleash the full potential of Michigan entrepreneurs and innovators, and they will fuel continued economic growth for the Great Lakes State.