Michigan is about to allow customer choice in the electric power market and, by doing so, end nearly a century of monopoly protection and guaranteed profits for electric utilities. How the state makes this free market transition will impact Michigan's competitiveness and cost of living. The report reviews key decisions before the legislature; analyzes the Public Service Commission proposals; shows the technical, environmental, and economic impact of deregulation; compares Michigan to other states; and recommends ten specific actions to ensure fair, timely, and comprehensive customer choice. The effects of so-called stranded cost payments to utilities are assessed in detail. A four-page glossary of technical terms is included. 33 pages.

Though choice is commonplace in most everyday goods and services, Michigan consumers have heretofore had no realistic choices in the purchase of electric power. Both technology and a national trend toward deregulation of the industry are about to change that.

Michigan’s electricity rates are among the highest in the Midwest—15 percent higher on average—and are a major economic impediment. Giving customers the power to freely choose their electricity provider, thereby ending decades of government-protected monopoly, would enhance the state’s future economic competitiveness. Enacting legal reforms to abolish exclusive franchise territories and allowing alternative power providers use of existing transmission and distribution facilities can bring about a truly competitive electricity marketplace in Michigan.

The result of bringing fair, timely, and comprehensive customer choice to the Michigan electricity market will be to:

• create a level playing field for future industry rivalry and competition, spurring new innovations;

• cut prices for residential customers by empowering them to choose their electricity provider;

• cut prices for commercial enterprises, especially small businesses;

• equalize regional differences in electricity prices;

• benefit the environment;

• increase service reliability; and finally,

• increase jobs and benefit local communities.

In January 1996, the Michigan Jobs Commission (MJC) issued a report on the electricity market in Michigan. Its nine recommendations were passed on to the Michigan Public Service Commission (MPSC), which issued an important staff report in December of that year. The MPSC staff report advanced at least two ingredients not included in that initial MJC report : It argued that all electricity customers, not merely industrial and commercial users, be granted choice (a position now embraced by the MJC), and it argued that rates under deregulation should not be increased for any customers. In a critical step toward deregulating the state’s electric industry, the MPSC approved in early June 1997 an order to phase in competition over a five-year period, with all customers given choice by 2002.

This study identifies six key deregulatory issues facing the state and in each case, makes one or more specific recommendations:

• Retail customer choice agenda and schedule: grant all customers choice immediately;

• Price/rate controls: eliminate transitional price controls on final retail prices and establish a simple, transitional transmission access pricing rule that compensates holders of the lines only for the actual cost of using those lines—sunsetting such rules once competition takes hold;

• Stranded cost recovery: disallow all stranded cost claims for compensation except in rare cases where a utility can prove beyond doubt that the investment was forced upon it by the MPSC or the legislature, and do not guarantee utilities a revenue flow (via transmission fees or customer rates) to pay back any bonds they may issue to "securitize" their losses.

A "stranded cost" is a cost incurred during the era of regulation (such as the expenses for a facility that may not be viable in a competitive market) that utilities argue should be paid for in the future by their customers or competitors. To allow for stranded cost recovery, except in the rare cases referred to above, would amount to a bailout of the industry that would hamper competition, give the less efficient utilities an unfair advantage, nullify many of the benefits of deregulation, force consumers to pay for services they do not want or may not even receive, and provide a harmful precedent for the future deregulation of other industries.

Curiously, the stranded cost question never arose when other industries were deregulated in recent years. Attempts to include such extraneous costs as employee retraining or the creation of new billing systems into a stranded cost definition should be seriously questioned.

The remaining three key deregulatory issues and related recommendations are as follows:

• Transmission operation and regulation: allow market participants to establish a regional transmission system without a preemptive mandate, and work with federal authorities to resolve interstate reciprocity concerns;

• Environmental concerns: ensure that the pro-environmental benefits of competition manifest themselves by giving all customers the choice to shop for "green power" immediately; and

• Universal service: impose no "carrier of last resort" requirements on any carriers and refrain from implementing assistance programs in ways that distort market activity.

Each month, Michigan families and business owners sit down to write out their checks to pay for their bills and budget their money for upcoming months. During this process, they may find themselves dissatisfied with the current prices they pay or the quality of service they receive. Whether it is the food they eat, the car they drive, the home they live in, the long distance company they subscribe to, or the credit card company they use, Michigan consumers have viable options in who provides them with these and other important goods and services. And, more importantly, they can switch suppliers at any time if they are dissatisfied for any reason. To summarize, Michigan consumers have choices, and lots of them.

Unfortunately, the same cannot be said when it comes to electricity. Michigan consumers have no realistic choices in selecting their electric power provider. Each month they send their checks to the same company, realizing there are simply no alternatives available to them. Electricity consumers have essentially been told that "you can have your car in any color as long as that color is black," to paraphrase Henry Ford. But this does not have to be the case. Just as the modern automotive industry offers consumers countless model, color, and style options, so too can the modern electricity market offer its customers numerous choices. There is no technological reason customers cannot be served by numerous suppliers and be offered uniquely tailored services.

The modern electric industry is sophisticated enough to handle the same sort of vigorous competition that Michigan consumers have grown accustomed to in other industries. The only thing that stands in the way of such a development in the world of electric power is a set of outdated rules and regulations that prohibit competitive interaction and customer choice.

Michigan citizens and policy makers have come to realize just how serious the lack of competition in this market is for the future of the state. Michigan rates are among the highest in the Midwest. As a consequence, Michigan families are spending a large portion of their monthly earnings paying unnecessarily high electricity bills, meaning their overall standard of living suffers simply because they cannot choose among competing providers for service.

Equally as important is the toll exacted on Michigan’s commercial and industrial sector by unnecessarily high electricity rates. As the Michigan Jobs Commission has noted, "Michigan’s commercial and industrial electric rates are on average 15% higher than our competitor states." 1 And because electricity represents a sizable portion of the overhead costs associated with the production of many goods and services, high electricity costs unnecessarily raise the cost of doing business. In turn, the state’s overall business efficiency drops and prices are artificially forced up since the costs of higher commercial and industrial electricity are eventually passed on to consumers. This forces many businesses to ponder the relocation of their plants or facilities to states with more hospitable electricity rates and service. Of course, when such drastic actions are taken, job dislocations result as well.

It is ironic that such negative economic effects could result from price differences of a mere penny or two per kilowatt hour (kWh) in electricity prices. Yet, when tens of thousands to millions of kilowatt hours of power are being purchased, a penny or two can make all the difference in the world. Therefore, when examining Michigan’s rates relative to the rest of the Midwest region and to the nation as a whole, Michigan citizens and policy makers should be aware that the penny or two difference in per kWh prices is what causes their monthly bills to be so much higher than other states. As indicated by Chart 1, Michigan’s electricity rates are among the highest in the region and significantly higher than national averages for commercial and industrial users.

If this situation is not remedied, the results could be serious for Michigan citizens. As Governor John Engler has noted, "Given Michigan’s disproportionate share of energy intensive industries, actions to reduce energy costs must be undertaken to ensure our State’s future economic competitiveness." 2 If such actions are not pursued, all customer classes will continue to pay unnecessarily power prices and the economic and employment base of the state may be placed at risk.

Michigan policy makers must give consumers the power to freely choose their power provider if this situation is to be remedied. Customer choice can be guaranteed by undertaking two types of reforms:

1. Legal reform: All laws which currently prohibit the free interaction of buyers and sellers must end. In particular, exclusive franchise territories, which give certain utilities monopolies over different service areas, must be forever eliminated as an uncompetitive restraint of trade. Any company, from any region (including outside the state) must be given the right to sell power to any customer that requests service.

2. Technical / structural reform: Technological and structural impediments to customer choice must also be eliminated. Specifically, alternative power providers must be allowed to use the transmission and distribution facilities, which all customers contributed to constructing, to provide final customers with power. Such an "open access" approach will require that policy makers ensure that the prices utilities charge for access to those poles and lines are fair and non-discriminatory. Once this is accomplished, all other price and rate controls can be eliminated.

These legal and technical/structural reforms are almost all that are required to unleash the forces of competition. At the request of Governor Engler, the Michigan Public Service Commission (MPSC) has recently released a blueprint to reform the Michigan electricity marketplace that proposes to get this process moving quite rapidly. While the MPSC’s blueprint represents a sound foundation for the creation of a more competitive electricity sector, some important changes will be required before the plan can be sure to guarantee Michigan citizens the full benefits of choice.

Michigan’s electricity consumers stand to benefit in many important ways once customer choice and free markets are substituted for the old command-and-control methods of the regulated monopoly model. Just as consumers, shareholders, and industry have benefited greatly from deregulatory initiatives in the fields of aviation, natural gas, telecommunications, and transportation, deregulation of the electricity marketplace promises to reap similar rich rewards. 3 For example, deregulation will

• create a level playing field for future industry rivalry and competition by ensuring that all companies have an equal chance to provide service to electricity consumers. Regulators will no longer be allowed to determine which firms will be given the privilege to serve consumers via exclusive franchising arrangements and other barriers to entry. Furthermore, regulators will no longer be allowed to ensure incumbent firms have their turf protected via generous returns on their investment which are guaranteed by regulatory fiat. In other words, deregulation means consumers, not regulators, will now be calling the shots in the electricity market. Jonathan Marshall, an economics and energy reporter for the San Francisco Chronicle, notes that the future looks bright for competition since, "High-voltage transmission lines, veritable electron superhighways, carry power thousands of miles with low losses, expanding the scope of regional markets. With more computer power and intelligent metering, nothing stands in the way of extending retail competition down to the household level." 4

• lower prices for residential consumers by empowering them to choose their electricity supplier. The current regulatory system forces consumers to pay artificially high prices for service. Although there has been a steady decline in the cost of electricity over the past decade, it does not mean prices cannot fall even further. A recent study by Clemson University professors Michael T. Maloney, Robert E. McCormick, and Robert D. Sauer for the Washington, D.C.-based Citizens for a Sound Economy revealed that in the long run the average monthly electricity bill for a typical residential customer who now pays $69 per month could fall by approximately $30—a 43 percent savings—if consumers had a real choice in who served them. 5 Short-run savings would also be significant. The authors estimate the same customer would experience an average short-term drop of $18—a 26 percent savings—per month. According to the study, consumers would save almost $107.6 billion annually if a truly competitive market developed. 6

Such cost savings would come not only from the direct competition posed by new firms entering the market, but would also develop as a result of the higher quality of service competition would foster. Wake Forest University Professor of Economics John C. Moorhouse notes, "[T]he variety of generating equipment and the large number of independent producers adds diversity to the system, lowering the probability of widespread equipment failure, and, thereby, reducing the amount of excess capacity required to provide a given level of service reliability." 7 Moorhead also argues that competition will mean a broadening of choices for electricity consumers and an overall increase in innovation within the industry. "Under competitive electricity generation, he argues, "[T]he market will provide an array of service standards that more closely match the mosaic of consumer preferences." 8 Furthermore, "Competition not only leads firms to be more responsive to consumer demands, monitor costs more closely, and compete on the basis of price, it provides an incentive to be innovative because that may be the only way to get a temporary jump on rivals. Developing a new consumer service, a better method of reducing costs, or a faster way of dealing with problems promises the innovator a competitive edge." 9

• lower prices for commercial businesses, especially small businesses. Just as residential consumers will reap the rewards of competitive choice, business of all shapes and sizes will also benefit greatly from deregulation. Electricity represents a substantial portion of many firms’ costs of doing business. Unfortunately, these high power costs do not disappear inside companies; they are factored into the final cost of the goods or services businesses sell. Because businesses cannot shop for better electricity bargains, higher electricity prices are often passed on to their customers. For example, according to the Food Marketing Institute, grocery stores spent approximately 4% of net sales on electricity expenses in 1994. Likewise, roughly $700 of the sticker price of every new General Motors automobile purchased in America annually is attributed to electricity expenses. 10 Other industries witness comparable portions of their profits devoured by large monthly electricity bills. Such ‘pass-through’ costs, which ultimately raise the prices consumers pay for goods and services, could be greatly reduced if America’s corporate sector could shop for competitively priced electricity.

Although opponents of change will argue that calls for deregulation are coming exclusively from large, corporate users of electricity that pay the largest power bills, it is actually small business owners and their customers who stand to gain the most from reform. This is because the electricity bills of small businesses often represent a much more substantial burden as a percentage of overall costs than those of large businesses. Smaller firms (especially retail stores with low profit margins) often struggle month-to-month to pay their utility bills. Competition will give them the right to search out more cost-competitive plans and alternatives that will then allow them to keep their doors open and pass on any savings they accrue to their customers.

• equalize unjustifiable regional differences in electricity prices. Wayne Crews, an economist with the Washington, D.C.-based Competitive Enterprise Institute also notes that while the average price of electricity in America is about 7 cents per kilowatt-hour (kWh), it varies widely from state-to-state, from roughly 5 cents to 10 cents per kWh. He argues, therefore, "This points to extraordinary inefficiencies. If customers could bypass their local utilities and gain access to power generators located elsewhere, billions could be saved." Consequently, he notes, "A mere one-cent-per-kWh drop in the average cost of 7 cents would save industrial, commercial, and residential customers $28 billion per year." 11

Deregulatory initiatives underway in many states foreshadow the benefits under nationwide deregulation. For example, New Hampshire instituted a pilot project in electricity competition in May, 1996, that allowed an unlimited number of companies to enter a small portion of the market and serve customers. Many companies involved in the New Hampshire experiment offered unique billing incentives and programs to encourage customers to switch providers, including free bird feeders for customers’ yards and the opportunity to dedicate a certain portion of their monthly bills to the environmental group or program of their choice. Illinois, Massachusetts, and New York have also initiated successful pilot projects.

These pilot programs have proved two important points. First, many companies desire to serve customers and many more are likely to emerge if open entry is allowed. Just as the long-distance telephone market flourished once rivals had access to networks, these state-by-state experiments illustrate the desire of electric entrepreneurs to offer new and innovative services directly to customers. Secondly, these experiments have already shown signs that electricity consumers of all sizes can expect cost savings if the market is deregulated. The Illinois program has yielded average savings of 15 to 20 percent for residential customers, 20 to 25 percent for small businesses, and 25 to 35 percent for large commercial customers. 12 The New Hampshire experiment has resulted in savings of 15 to 20 percent for non-industrial customers and 20 to 30 percent for industrial customers. Similar savings have been realized in the New York and Massachusetts pilot programs.

• increase jobs and benefit local communities. Many large, monopolistic utilities that do not want consumers to have the ability to choose alternative providers have used scare tactics, intense lobbying, lavish campaign donations and outright deception to convince many local communities that deregulation will hurt them. Nothing could be further from the truth. Most of the large workforce cutbacks these firms warn of have already taken place as a natural reaction to general downsizing in this industry. If anything, competition is likely to increase employment in the industry or at least allow it to level off as new firms enter the market or existing firms look to innovate in the face of increased rivalry.

• benefit the environment by empowering electricity consumers to be smarter, more demanding shoppers. This will, in turn, mean that power companies will be held to higher standards of efficiency and cleanliness to ensure communities are provided the power they want without increased pollution or other negative side effects. Again, competition will breed innovative solutions and new alternatives to the less efficient production methods used today, benefiting the environment in the long run.

• increase service reliability. Increased innovation is also likely to bolster service reliability as firms begin to realize their profits and markets are no longer protected in the case of business failure. Under the regulated monopoly model, consumers cannot switch to a new provider when their current provider proves unreliable. Under competitive conditions, service failures will be met with consumer rebellion and, consequently, profit loss, thus strengthening the incentive to maintain high service standards. Claims that competition is already stretching the limits of the current networks’ reliability, or soon will force major outages, are patently absurd scare tactics used by proponents of the status quo to derail reform legislation. Just as deregulation and competition in other industries have resulted in improved safety and reliability, so too will electricity markets benefit when liberalization occurs.

Before discussing the details of the Michigan Public Service Commission plan and the changes needed to achieve the desired effects, it is worth briefly examining the current structure and behavior of the Michigan electricity marketplace to understand the nature of the problems the PSC hopes to overcome.

Michigan consumers are served by nine investor-owned utilities (IOUs), just over a dozen rural cooperatives (COOPs) and over 40 municipal electric utilities (MUNIs). While municipally owned utilities are not subject to regulation by the Michigan Public Service Commission (MPSC), all COOPs and IOUs are regulated by the agency.

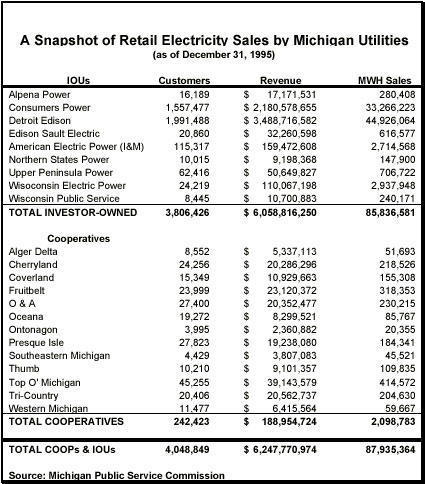

Michigan’s private IOUs control the vast majority of the electric marketplace with 3.8 million customers and just over $6 billion in revenues relative to the 242,000 customers and $189 million controlled by the COOPs. Appendix A lists complete 1995 data 1995 for Michigan’s IOUs and COOPs, including total customers, revenues, and MWH sales (See Chart 3.)

Yet, in reality, when discussing deregulation and who will be the primary industry players in the debate, it should be clear to all parties involved that the Detroit Edison Company and Consumers Energy (a division of the CMS Energy Corporation) are the proverbial kings of the hill. (Note: Consumers Energy was formerly known as Consumers Power and is still often referred to as such in reports and studies). As Chart 2 illustrates, Detroit Edison and Consumers Energy together hold almost 90 percent of the market. In terms of both revenues and geographic coverage (the size of their territorial monopoly), Detroit Edison and Consumers Energy are often thought of as the Michigan electricity market.

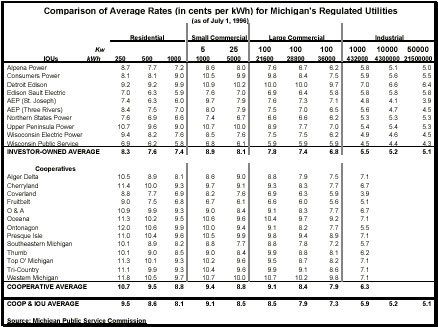

As mentioned above, Michigan’s electricity rates are among the highest in the Midwestern region and are also above the national average. Appendix B summarizes the average price per kWh charged by Michigan’s regulated utilities for all customers classes.

Chart 4 dramatically illustrates the true impact higher electricity rates have on the Michigan marketplace. While Michigan’s average electricity rate of 7.1 cents per kWh does not sound that much higher than the national average of 6.9 cents per kWh, it is important to discuss the rates Michigan’s different customer classes are charged relative to other states—especially those which compete with the state for industrial and commercial job opportunities.

Within the Midwest region, Michigan’s overall electricity rates are higher than those of Indiana, Wisconsin, and Minnesota, and its industrial rates are higher than those of Illinois and Ohio. Average commercial and industrial rates are particularly important to Michigan since artificially high electricity prices can discourage industries from settling in Michigan or even staying there. Because a great number of energy-intensive businesses currently reside in the state, it is vital that policy makers remove barriers that keep electricity costs artificially high for these firms. Without action, many firms might relocate to other states.

Consider automobile manufacturing. When an automaker is considering expansion plans, it first looks for an appropriate location for the plant. Of the many considerations (including labor costs, environmental regulations, tax incentives, and others), one of the most important will be how the region may affect the firm’s cost of goods sold (including effects on raw material and overhead costs). One of the most important costs will be electricity, since auto production demands large energy inputs.

Holding all other factors equal, consider the choice a firm’s board of directors has if the field has been narrowed to Michigan, Ohio, Kentucky, and South Carolina. Michigan’s industrial rates hover around 5.2 cents per kWh. Ohio, Kentucky, and South Carolina’s rates are all roughly 4 cents or lower. Clearly, if the decision came down to such a consideration, Michigan might lose a potential source of good jobs and income. While the state might attempt to find ways to get around this problem via tax breaks or other special incentives, history has proven that other states will be willing to engage in a "race to the bottom" in terms of special preferences. If Michigan policy makers have to engage in such an economic war of special preferences to compensate for artificially high electricity rates, Michigan taxpayers will end up footing the bill in one way or another.

The same scenario could play out across many other commercial industries as well, such as large retail stores or grocery chains. Higher electricity prices affect the decisions businesses make and can have a negative impact on the future economic competitiveness of the state. A study by Wayne Crews shows just how much Michigan’s commercial, and industrial consumers have to gain under competitive conditions. Assuming a 5 percent to 45 percent price cut, Crews estimates commercial customers could save anywhere from $293 to $2,641 annually. For the average industrial customer, the savings are even more impressive, ranging from $6,831 to $61,481 annually. 13 For very large industrial companies that consume more electricity, the savings would be even higher.

Savings of this magnitude will lower the overall costs for Michigan’s industrial and commercial customers, which in turn will improve business efficiency and productivity. A more competitive economy and an improved job market will result from such savings.

Customer choice and competition will also have direct benefits for Michigan’s residential consumers. Electricity choice will lower rates for families and senior citizens on fixed incomes, resulting in an immediate improvement in their standard of living. And while those who support the uncompetitive status quo will argue that residential consumers will not have the knowledge or information available to them to "shop around" for service, history certainly points to the opposite conclusion. Airline transportation, rail and truck shipping services, and long-distance telephone service—all once heavily regulated industries—are now extremely competitive thanks largely to the vigorous efforts of consumers to constantly shop around for the best deal.

It is likely that competition will greatly increase marketing and advertising efforts by companies seeking to attract the allegiance of Michigan’s overcharged electricity consumers. Newspaper, magazine, and television reports will undoubtedly make consumers aware of the options available to them. Consumers will become savvy electricity shoppers with the sort of information shown in Chart 5.

What will be the end result for residential consumers in terms of reduced rates and overall savings? Economist Wayne Crews estimates substantial savings. Even a small 5 percent drop in prices would yield $29 in annual savings. A more substantial cut of 45 percent would yield estimated savings of $265. 14 Regardless of the magnitude of the savings, residential customers will have more disposable income available once choice becomes a reality.

A competitive electricity market will increase service quality and reliability while introducing more innovative service options into the marketplace. For example, more environmental options—such as so-called green power from hydroelectric, solar, and wind sources—will be available. Likewise, consumers will be able to bid as a group for reduced rate bulk power. For example, a senior citizens’ organization may be able to arrange special deals on behalf of its members.

This will be extremely important since, as shown by Chart 6 and Chart 7, residential consumers and small commercial businesses actually get hit very hard by electricity prices. In fact, residential and small commercial business rates are actually much higher in per kWh terms than the rates charged to large industrial customers.

Higher residential and small commercial rates are not surprising since large industrial consumers have some bargaining power that allows them to negotiate long-term bulk purchase arrangements that help reduce their overall rates. In an environment of comprehensive choice, all rates—not just those paid by industry—would tend to be forced downward by competition.

Politically, this means policy makers must ensure that residential and small business consumers are guaranteed competitive choice on equal terms with large commercial and industrial businesses. Otherwise, residential and small business customers will rightly claim they are not being treated equitably as deregulation unfolds.

An oft-repeated criticism of deregulation made popular by defenders of the regulatory status quo—that Americans already enjoy low enough electricity rates relative to the rest of the world—must be debunked. William T. McCormick, Jr., chief executive of Consumers Energy, argues, "America’s industrial electric rates are far lower than those in countries we regard as our main industrial competitors. Japanese and German factories pay electrical rates several times higher than U.S. rates." 15

"But," as Doug Bandow, senior fellow with the Washington, D.C.-based Cato Institute responds, "being the best regulated monopolist is no longer enough." 16 The fact that the rest of the world suffers the adverse effects of centralized regulatory planning should not serve as an excuse for denying American consumers the benefits of competition and customer choice. Technologically, there is nothing preventing such a development from occurring. All that remains is the political will to take action to ensure that a fair and competitive future develops.

On January 8, 1996, the Michigan Jobs Commission (MJC) issued a concise but controversial "Framework for Electric and Gas Utility Reform." 17 In the report, the MJC argued that power rates for Michigan’s industrial and commercial businesses must fall if the economic competitiveness of the state is to be sustained well into the future.

The MJC report contained six important near-term recommendations as well as three additional immediate and long-term recommendations. Near-term recommendations were as follows:

(1) Direct retail access to power generators for new industrial and commercial purchases;

(2) address "stranded costs" to ensure incumbent utilities are ready for competition;

(3) study the replacement of rate of return regulation with rate cap regulation;

(4) allow immediate "file and use" tariffs for non-wheeled power;

(5) eliminate unnecessary environmental programs and other regulatory measures; and,

(6) reorganize the Michigan PSC into three smaller divisions.

The MJC’s longer-term recommendations were as follows:

(7) Create an independent wholesale power pool for electricity sales;

(8) demand retail access for industrial and commercial buyers by January 1, 2001; and,

(9) allow for freedom for mergers and acquisition to take place.

MJC’s nine recommendations were provided to Governor John Engler, who in turn passed them along to the Michigan Public Service Commission with the mandate to "work to refine and act upon the . . . blueprint for competition in a timely manner." Eleven months later, on December 19, 1996, the Michigan Public Service Commission released its "Staff Report on Electric Industry Restructuring" (MPSC Staff Report). 18 Although the MPSC Staff Report discusses all nine recommendations contained in the Michigan Jobs Commission blueprint, the Staff Report proposed that the entire electricity reform effort should be driven by two fundamental principles:

(1) all customers should be eligible to participate in the emerging competitive market;

(2) rates should not be increased for any customers and should be reduced where possible.

Although seemingly simplistic, the MPSC’s guiding principles advanced two additional recommendations not contained in initial MJC blueprint. First, all electricity customers, not merely industrial and commercial users, are to be granted choice in who provides them with electric service. This means residential customers must be given the ability to switch providers as they desire on the same timetable as industrial and commercial customers.

This recommendation represents a genuine improvement over the initial MJC report, which ignored the residential consumer sector of Michigan’s economy. (The MJC has since publicly embraced choice for residential electricity consumers.) Clearly, no class of customers can be ignored if a coalition for reform of Michigan’s electricity market is to develop. Although the state’s business sector is right to complain that its electricity costs are too high, residential consumers can also rightly claim their monthly utility bills place too great a burden on them and their families. Therefore, the MPSC is to be commended for ensuring residential consumers are treated on equal terms in the deregulatory process.

The second major MPSC recommendation sounds even better than the first, but may present some problems as deregulation unfolds. By arguing that rates should not be increased for any customers, and that they should be reduced where possible, the MPSC appears to have made a fairly noncontroversial recommendation. After all, with rates being so much higher for Michigan consumers, it is unlikely rates could go up for anyone in any customer class in the competitive future. However, by taking a hard-line stance against any rate increases, it begs the question about what the MPSC will do if a small handful of customers experience small rate increases in the future, for one reason or another. Is the MPSC saying it will not allow the free fluctuation of rates in the competitive future? If so, such price control efforts may actually distort beneficial pricing signals and distort competitive entry decision making.

The 46-page MPSC Staff Report goes into much greater detail on several key issues involved in the restructuring and deregulation of the electricity sector, each of which is worth examining in detail.

MPSC Key Issues

|

The MPSC Staff Report wisely speeds up the Jobs Commission’s direct access deployment schedule by demanding that a much greater amount of new load be available to customers on a competitive basis. Starting this year, Michigan utilities would be required to make at least 2.5 percent of their load available for direct access competition. For Detroit Edison and Consumers Energy Company, this would equal 225MW and 150MW blocks of load, respectively. Finally, under the original MPSC draft plan, by 2001, all commercial and industrial customers would be given full competitive access while residential customers would be phased in at a rate of 2.5 percent per year. By 2004, all residential customers would be guaranteed choice as well.

Although the direct access schedule contained in the original MPSC Staff Report is a clear improvement over the much less ambitious Jobs Commission report, it still fails to take these crucial steps rapidly enough. There is simply no reason to delay the immediate transition to competition for all customers. Denying residential customers full competitive choice while industrial and commercial users enjoy the fruits of competition will lead to calls of an uneven playing field or corporate favoritism. As Michigan Attorney General Frank Kelley aptly argued in testimony before the MPSC on January 14:

"I am dismayed that the plan continues to contain a divisive dichotomy between business customers and residential customers. . . . I cannot support a plan that does not permit all customers to have equal access to power suppliers. Commercial and industrial customers must not be permitted to lock up available low-cost power from 2001 to 2004, leaving only higher priced power for residential customers. The goal of restructuring must be to bring the benefits of a competitive generation market to all customers, not just a few." 19

Luckily, when the Commission handed down its final Opinion and Order on June 5, part of this problem had been corrected. The Commission conceded that asymmetrical treatment of customers would be unfair, and therefore, the phase-in schedule for direct access will now apply to all customer classes equally.

Unfortunately, however, the gradual phase-in itself remains unaltered. The Commission apparently remains committed to a staggered transition to full customer choice. This is unfortunate and unnecessary. All customers could be granted choice much earlier than the Commission’s planned timetable allows. Indeed, if Michigan policy makers want to remain in line with, or ahead of, the timetables established by other states, this timetable must be accelerated so that all customer classes are guaranteed choice long before the current 2002 date set by the Commission.

Recommended Action #1: Grant all consumers choice immediately.

The MPSC Staff Report recommends that a number of pricing safeguards be included in the plan to open the market to retail access. These protections include (1) a base rate freeze, (2) alternative power supply cost recovery treatment, and (3) limited performance-based regulation.

The MPSC argues these safeguards are necessary since, "Customers not participating in the direct access program need to be protected from potential cost increases that might otherwise result from the transition to direct access. Such protection is especially important during the period when direct access opportunities are necessarily limited." 20

This begs the question: Would such price protections and rate controls be necessary in an environment of full-blown competitive retail choice? It is only because the MPSC Staff Report recommends a staggered phasing-in of retail access that such protections must be considered. If Recommendation #1 is followed and all customers are provided choice on equal terms immediately, there is no need for convoluted price controls to be in place as Michigan moves toward a more competitive future.

The only legitimate pricing issue the MPSC should be concerned with is the price utilities charge alternative providers for access to transmission and distribution lines used to reach customers. Because alternative power providers will need to use these lines to "wheel" their power to customers across Michigan during the transition to a fully competitive market, the MPSC may have a role in making sure access prices are not well above the actual cost of providing such service. If utilities controlling these lines are allowed to include many other costs in the transmission access price (such as a stranded cost recovery tax discussed below) then competition may fail to develop and overall power prices may not fall.

As long as the MPSC stipulates that alternative power providers deliver service to all Michigan consumers across existing transmission and distribution lines at reasonable rates, there should be no need to regulate final retail power prices since the competitive interplay of buyers and sellers in the marketplace will work to reduce prices. Furthermore, even the regulations governing the pricing of transmission access should end at some point in the near future—perhaps after five years.

Recommended Action #2: Eliminate transitional price controls on final retail prices.

Recommended Action #3: Establish a simple, transitional transmission access pricing rule that compensates holders of the lines only for the actual cost of using those lines. Sunset such transitional rules once competition takes hold and the market power of the current monopolists has dissipated.

There is no more controversial topic or issue central to the outcome of the debate over electricity restructuring than that of transitional or "stranded" cost recovery. 21

The MPSC defines stranded costs as "(1) costs that were incurred during the regulated era that will be above market prices during competition, and (2) costs that are incurred to facilitate the transition from regulated monopoly status to competitive market status." 22 What does this mean in plain English? It means that some utilities made investments in the past that they might lose money on in the future. In other words, "stranded" costs are nothing more than future monetary losses. 23 And utilities want their customers, or new competitors, to pay for them—which means they want to force tens of billions of dollars of costs on consumers.

These potential future utility losses could be brought about by a number of factors. The largest category of stranded costs will be created by nuclear energy investments, especially nuclear facilities that are nonoperational for one reason or another. Another factor that could bring about future losses are contracts that utilities were forced to enter into under the Public Utilities Regulatory Policy Act of 1978 (PURPA). PURPA required utilities to purchase power produced from independent power producers (such as solar, wind, geothermal, and cogenerators) who became known as "qualifying facilities" (QFs) under the law. Utilities were forced to purchase QF-produced electricity at the same cost they would have incurred producing it themselves or purchasing it from another comparable provider. Many utilities remain locked into long-term QF-contracts, most of which they entered into only because PURPA required them to.

Utilities argue that their captive customer base has a duty to pay off any losses they sustain in the future since they always have in the past. One of the reasons Michigan power rates have been so high in the past is that Michigan has allowed the utilities to pass along the costs associated with inefficient investments to ratepayers in the form of artificially higher prices. Despite the fact that these customers did not demand that many of these inefficient investments be made, they simply had nowhere else to turn for service since they were served by a single monopolist. The utilities argue this arrangement was, and still is, the equivalent of a "regulatory contract" between them, their captive customers, and regulators. Essentially, they argue, an implicit deal was struck between these parties that they would serve all customers within their service territory at a fair and reasonable rate in exchange for freedom from competition and a guaranteed stream of revenues. In the future, however, when rates are freed to fluctuate and the profits utilities earn are not guaranteed by regulators, some utilities may lose money. The "regulatory contract" notion argues that someone besides utility monopolists and their shareholders should pay the price of their inefficient investments since that is the way things used to work.

No matter how one describes the "regulatory contract" arrangement among regulators, utilities, and the public, it should be obvious it turned out to be a bad deal for consumers overall. They have been held hostage to a system that has provided them with a relatively undifferentiated service at a price they simply had to settle for no matter how outrageous. Only the largest of industrial customers have had any real negotiating power since they could threaten to leave the state or go so far, as many of them have, as to construct their own power plants adjacent to their manufacturing facilities.

This begs the question: Even if a "regulatory contract" really existed, would not customers have the right to opt out of it at some point? Or, even if they did not, would not the contract have been of limited duration and have expired at some point in the past, or at least be open for renegotiation? But such questions need not be raised since the so-called "regulatory contract" is really only as good as the paper it is written on—which is to say it is worthless since no such literal contract exists.

Michigan regulators and policy makers must realize the stakes of forcing captive customers to pay for a massive, multi-billion dollar bailout of the utility industry based on the unsupportable legal foundation of regulatory contract theory. A bailout of this magnitude will

• destroy competition in its cradle. If every new rival that wants to enter a new service region and offer competing service is forced to pay a hefty stranded cost recovery tax to the incumbent utility, fewer firms facing the prospect of such a high entry fee will be likely to look to enter that market;

• give less efficient utilities an unfair advantage. If inefficient incumbent monopolists are bailed out, their cost of capital (or the cost of raising or borrowing money for firms) would likely be artificially lowered, meaning new rivals would have a tougher time raising the money needed to face off against incumbent utilities. More importantly, if they are granted lavish loss recovery early in the process through a securitization plan (discussed below), then they will leave the starting gate of competition with an insurmountable advantage in terms of new cash flow with which to make investments. Finally, with fewer firms facing off against inefficient incumbents, the incentive to offer innovative services decreases and quality is unlikely to improve;

• nullify the benefits of competition and prevent serious price competition. If fewer competitors choose to enter the market and compete, or if captive customers are forced to pay large ‘exit’ fees to their current provider before they are allowed to shop for service, prices are unlikely to fall significantly any time soon. While regulators might try to freeze prices or demand rate reductions by utilities, this is a poor surrogate for genuine price competition and ultimately may discourage competitive entry;

• force consumers to pay for services they do not demand or may not ever receive. If existing customers are forced to pay off utilities before they can choose alternative suppliers, this will force many of them to continue to purchase power from their current supplier against their wishes since they will not be able to afford the switching costs. In effect, consumers will be stuck paying for losses incurred by multi-billion dollar corporations who never provided these customers with any benefits for the money;

• represent "corporate welfare" of an unprecedented level. Bailing out utilities would constitute a massive transfer of wealth. And, amazingly, this wealth transfer would be going from the pockets of average Americans to wealthy utility companies who have already benefited from years of generous, guaranteed profits on the backs of captive customers. In this sense, stranded cost recovery is just another example of "corporate welfare." As Attorney General Kelley has argued, "[T]he proposal put forward in the staff report will not, in my judgment, [bring about a more competitive electricity market]. Instead, this plan, which was developed primarily by our state’s two largest utilities, amounts to a massive giveaway to . . . Detroit Edison Company and Consumers Power;" 24 and

• provide a frightening and disastrous precedent for the future. Granting electric utilities stranded cost compensation of billions or hundreds of millions of dollars as they move into a competitive environment would set a disastrous and disruptive precedent. If every industry or organization that is even tangentially regulated by the government is allowed to claim compensation once deregulation or reform occurs, it could result in a financial nightmare and a stifling of deregulation.

A bailout of the utility industry is not warranted. There is no historical precedent for such a move. Other regulated industries such as telecommunications, trucking, railroads, and aviation did not receive compensation for real or imagined deregulatory losses; neither should electric utilities. In fact, the very term "stranded costs" is of recent invention. Electricity industry officials coined the term in an attempt to shelter themselves from the onset of competition. The term has never been heard in any other previous deregulatory deliberations including last year’s contentious debate over telecommunications reform. Why might policy makers take seriously the "stranded cost" arguments raised by electric utility officials?

First, regulators are more attached to the utility industry and are more concerned about its future than that of other industries. 25 In fact, although the MPSC officials claim to have developed their recommendations on this subject after meeting with numerous parties, on the third page of their Staff Report they note that, "The specific details in this Report were developed primarily through discussion with Consumers Power Company and Detroit Edison. . . ." 26 It is likely these two large monopolies had a shaping influence on the MPSC’s thought process as the agency developed its recommendations.

When firms of this size, which have historically controlled such a considerable percentage of market share, warn that the sky will fall in the absence of a generous bailout, it is not surprising to see government officials buckle under the pressure and recommend such a move. As Barry Cargill, vice president for government relations at the Small Business Association of Michigan, argues, "The Public Service Commission plan seems to give the regulated utilities all that they want rather than requiring them to prove what they deserve." 27 Jack Mason, a 15-year veteran economist still with the MPSC, appears to agree, referring to the nearly $10 billion in stranded cost loss recovery requested by Detroit Edison and Consumers Energy alone as "gross overestimates." 28 In an internal MPSC memo dated January 22 nd that was obtained by The Detroit News, Mason argues that "it is difficult to be too critical" of the MPSC Staff Report since "Consumer interests are compromised completely or almost so." 29 He adds that, "Michigan’s effort on electric restructuring appears to show less balance, being completely favorable to utility interests, than in any other major state considering restructuring." 30

The second reason the MPSC is seriously considering a stranded cost bailout has to do with its fears about the continuous future supply of power. The Commission is concerned that the future provision of electric power to consumers would be placed at risk if the financial health of the firms it regulates was not guaranteed. This is a legitimate concern, but one based upon a misunderstanding of how a competitive market might work. First, it is unlikely any firm will be forced to declare bankruptcy if full stranded cost recovery is denied. Most firms will be able to divest many unwanted or less efficient assets, restructure their business operations or creatively use mergers or acquisitions to retain market share and customers; continue to amortize debts as part of their regular depreciation schedules; and, pass along some costs to shareholders over time.

Even in the extreme case that a utility is forced into bankruptcy, it is important to note that this does not mean it will forever close its doors, close its plants, and cut off power to the communities it serves. Bankruptcy is a legal proceeding that allows many firms to reorganize their debts and their business operations while they get back on sound financial footing, albeit with strict court-imposed operating restraints. In the meantime, customers would continue to receive power. Frederick H. Abrew, CEO of Pittsburgh-based Equitable Resources Inc. recently told Business Week, "There have probably been a half-dozen bankruptcies in the last 10 to 15 years. I don’t know of any customer that failed to get energy." 31

Furthermore, in a competitive future with open retail access, power could be sent to consumers from competing companies far away. Many of these companies could assume control of assets that other utilities could not afford to operate, thereby ensuring that service was continued. Despite the ‘Chicken Little’ fears utilities have placed in many people’s heads, predictions of loss of electric power service are greatly exaggerated.

What is the proper way to handle the difficult and controversial issue of stranded cost recovery and a utility industry bailout? The first recommendation is simple: Do not under any circumstances follow the California model. California legislators, who claim they have found the perfect model for deregulating electrical markets, plan to provide their monopolistic utilities with a $28.5 billion bailout. Amazingly, the total size of the market is only $23 billion. 32 This means California utilities will be getting a cash handout at the starting gate of competition that is larger than the aggregate size of the entire market! 33

But what is most dangerous about the California plan is its use of a so-called market mechanism known as securitization to allow monopolistic utilities to recover stranded costs. Under securitization, utilities calculate their estimated future losses and then offer bonds on the open market equal to the amount of stranded costs they want to recover. This allows utilities to immediately collect the amount of compensation they desire and then pay back these new bond holders over a number of years. These stranded cost bonds are backed by the utilities’ promise that they will be able to collect on-going transition taxes from customers until the bonds are completely paid off.

The MPSC Staff Report recommends the use of securitization to recover future utility losses. These so-called stranded costs are nothing more than potential future losses. There is no way to determine the exact present value of a future loss. If utilities are given the ability to estimate their potential future losses up-front, as securitization would allow, they will have a strong incentive to greatly exaggerate these costs. It is unlikely these large utilities will actually lose as much as they currently estimate. The idea of preemptively providing these utilities compensation for losses they will not incur for some time makes little sense. If any recovery is provided, it must be done as the losses are incurred, not beforehand.

How much would stranded cost compensation raise electricity prices? The MPSC Staff Report estimates that the sum of the transition charge and securitization charge for Consumers Energy and Detroit Edison would be in the range of 1.2¢ to 1.3¢ per kWh. Although this additional expense sounds trivial, this securitization tax would place a substantial burden on customers when they are ordering thousands to millions of kilowatt hours of electric power. Conversely, the Commission predicts that securitization would actually help reduce rates slightly in the short term by arguing that utility losses would be paid for via the issuance of bonds.

This is illogical. Consumers would be offered much lower rates in a competitive market free of any utility bailout. In other words, if Michigan policy makers put their stamp of approval on a securitization plan today, they will be unable to do anything to alter their policy in the future since the money will flow to the utilities once the bonds are issued and ratepayers will be stuck paying off the holders of those securities over the long haul.

A recently released study of securitization by the Indianapolis-based utility IPALCO Enterprises, Inc. notes, "Under the promise of minimal rate reduction, securitization establishes, for the first time in history, a long-term, irrevocable consumer obligation to pay, in advance, for future business losses of the utility. Whether characterized as a consumer subsidy of inefficient and uneconomic utilities or as a massive corporate welfare program dwarfing all historical analogues, securitization of electric utility stranded costs promises to be the greatest swindle ever perpetrated on the American consumer." 34 "Moreover," the report states, " . . . the adverse effects of securitization on infant competitive power markets will be profound" 35 since inefficient utilities that receive such a generous bailout will be able to use their infusions of billions of dollars to buy out smaller competitors.

While policy makers or regulators can probably not stop utilities from issuing new debt securities independently, they can and should make it clear to these utilities that the repayment of these new bonds will not be guaranteed via transitional taxes and fees on captive customers. This would effectively end any attempt by the utilities to securitize their debt since they would no longer have the force of regulatory coercion behind them with which they could require the public to pay off their newly issued bonds.

The bottom line on this divisive issue is that stranded cost compensation is almost never justified. Even in the case of uneconomical nuclear assets, California State University Economics Professor Robert Michaels has argued, "Any utility that claims a nuclear stranding should show that regulators gave it no choice but to build or complete the plant despite the utility’s preference for an alternative." 36 If such a claim is made and proven by a utility, then some recovery may be justified. But, if the utility went along with a plan to build a nuclear plant, or any other plant or facility for that matter, it would be very difficult to argue they should not now be responsible for losses associated with the plants.

The only legitimate category of stranded cost recovery may be the PURPA contracts that were forced by regulators upon utilities against their strong resistance. One possible solution to this problem is to encourage renegotiation of above-cost PURPA contracts to bring them in line with more reasonable market prices for power. This would lessen the burden of the contracts on utilities while ensuring consumers or competitors are not stuck footing the bill for losses associated with the contracts. Still, some small amount of recovery may be justified where these mandated contracts have forced utilities to incur costs against their will and cannot be renegotiated.

A good test that regulators can employ to determine if any compensation should be considered is the following: If a utility can show that it made an investment at the insistence of regulators, and resisted the action but was forced to move forward anyway, then it has a better case for compensation. In a recent study advising Pennsylvania regulators, Dr. Jake Haulk, research director for the Pittsburgh-based Allegheny Institute for Public Policy, concurs but adds important qualifications to this simple test that are applicable for all state and federal regulators.

"Any utility which can show that it was ordered to make expenditures that it would not have undertaken on its own, and which other utilities were not ordered to make, should be given some opportunity to recover those outlays. The guiding principle here must be this; to what extent has the utility been uniquely disadvantaged by regulators or government agencies? If all utilities have been treated the same by regulators, the playing field will remain level after competition is introduced and hence there is no reason to allow stranded cost recovery.

This exception will require very careful language in legislation and scrutiny in practice at the PUC. This exception should not be allowed to develop into a loophole that results in endless clamoring for special treatment. We would rather not allow this very narrow recovery opportunity than have a situation in which movement toward true deregulation and competition is slowed or thwarted." 37

Rarely have utilities fought proposals by regulators to mandate the construction of new facilities or requirements to undertake other activities. If utilities showed no reluctance to move forward with the projects regulators urged them to pursue, then they clearly have no grounds for recovery. And even in those few cases where limited recovery might be approved by policy makers, utilities should be asked to do everything in their power to mitigate these costs before they are absorbed by third parties. Regulators might even want to encourage utilities to divest themselves of certain assets for which they are claiming compensation. This would at least allow the utility to recoup some of the costs associated with the asset and would simultaneously ensure that customers or new competitors are not stuck footing an unnecessarily large bill.

Finally, no other costs associated with deregulation or restructuring, such as employee retraining or the creation of new billing systems or metering technologies, should be included in the definition of a stranded cost. These are future investments that will be made by existing and new market players in the future on their own. There is simply no need to mandate that incumbent firms be granted special compensation today to pay for such transitional items or investments.

Recommended Action #4: Disallow all stranded cost claims for compensation except in the rare cases where a utility can prove beyond doubt that the investment was forced upon them by the PSC or the legislature.

Recommended Action #5: Allow utilities to securitize their losses if they want, but do not guarantee them a revenue flow to pay back the bonds via additional transmission fees or charges on captive ratepayers.

The MPSC Staff Report discusses many transmission operation and regulation issues at length. Two issues in particular are worthy of focused discussion—the establishment of an Independent System Operator (ISO) and the question of how to deal with reciprocity concerns.

The MPSC Staff Report is to be commended for recommending, but not mandating, the establishment of an Independent System Operator (ISO) for the state of Michigan. An ISO would be an independent entity that manages the electrical transmission system in a given region in a nondiscriminatory manner. An ISO would also be responsible for the reliability and quality of its regional power grid.

The ISO model is attracting the support of many industry officials and experts who are recommending such a mechanism as the solution to the many grid management concerns. While it is certainly a viable option, it would be a mistake for the MPSC or any regulatory body to preemptively mandate a single transmission system or structure. Instead, regulators should allow market participants to voluntarily work together to establish efficient regional transmission systems, and merely provide assistance when it is deemed appropriate. It is important to note, however, that most ISOs would be regional in scope, meaning they would be beyond the jurisdiction of the Michigan PSC.

A closely related transmission issue which the Commission deals with is that of reciprocity. Reciprocity in the delivery of electrical service essentially means carriers operating in different geographical regions should have comparable opportunities to compete in each other’s territory. Essentially, the MPSC wants to make sure that as the regulatory walls surrounding Michigan’s monopolistic service territories fall and new rivals seek to enter each other’s turf, they can do so on equal terms. While the MPSC can guarantee such reciprocity on an intrastate basis, it is much more difficult to deal with interstate reciprocity concerns. In other words, what happens if Michigan’s market is opened before Ohio’s and an Ohio utility can offer service to Michigan citizens but a Michigan utility cannot provide electricity to Ohio residents?

Clearly, this a serious concern and one that requires the attention not only of Michigan policy makers, but also federal officials who have jurisdiction over such matters. If the state of Michigan attempted to resolve every reciprocity dispute on a bilateral basis, it would require far too much time and hassle and only delay the benefits of competition for in-state consumers. Instead, Michigan policy makers should work with the Federal Energy Regulatory Commission (FERC) and federal officials to establish a multilateral approach to free trade in electricity. Since the FERC has jurisdiction over such issues, this will probably occur at some point in the future as an increasing number of states plan to open their borders. Yet, Michigan should work in conjunction with the FERC and federal policy makers to resolve interstate reciprocity matters on a timely basis so a harmonious, competitive nationwide electricity market can develop more rapidly.

Recommended Action #6: Do not preemptively mandate a single transmission system or structure on the industry. Allow market participants to voluntarily work together to establish an efficient regional transmission system.

Recommended Action #7: Work in conjunction with the FERC and federal policy makers to work out interstate reciprocity concerns. Allow for some federal role in this process to ensure the harmonious development of nationwide competition.

The MPSC is also to be commended on its brief but excellent discussion of the many environmental myths that surround the debate over electricity restructuring. The MPSC Staff Report points out that an open, competitive electricity marketplace will benefit the environment in three primary ways:

1. "The direct access program will allow customers to choose from available "Green" power suppliers, thus enhancing the market for clean generation." 38

2. "[A] direct access program should promote the development of smaller gas-fired power plants, . . . [which] will be more environmentally friendly, since gas combustion produces virtually no sulfur oxides which contribute to acid rain and also produces less carbon dioxide than burning coal." 39

3. [A] program of customer choice will encourage the development of new competitive energy conservation programs. . . . Direct access will allow energy service companies to develop innovative programs tailored to meet the individual needs of their customers." 40

The MPSC is correct to argue that competition will have such beneficial environmental effects, but it is important that realize such benefits will develop only if the market is free of artificial constraints and unjustifiable stranded cost loss recovery. In particular, the staggered direct access schedule for residential consumers may discourage the development of a more environmentally friendly marketplace. This is because residential customers may actually prove to be more demanding shoppers than commercial and industrial users. A recent poll found that 66 percent of Americans surveyed, "would be willing to pay a few dollars more a month . . . to receive power that was produced using non-polluting, environmentally-friendly technology." 41 Therefore, if residential customers are not granted the ability to immediately shop around for a service provider of their choice, the pro-environmental effects of a competitive marketplace will be impeded.

More importantly, if Michigan utilities are granted recovery of supposed stranded costs associated with less efficient plants, it will encourage these firms to continue to use older and potentially more pollution-prone technologies instead of switching to modern, cleaner technologies. In this sense, stranded cost recovery is not only an anticonsumer policy, it is an anti-environmental policy as well. Recovery on such inefficient plants and assets should be denied.

Recommended Action #8: Ensure that the pro-environmental benefits of competition manifest themselves by giving all customers the choice to shop for green power immediately, and by denying stranded cost recovery for inefficient utility investments.

The MPSC Staff Report discussion of universal service issues is woefully inadequate. Essentially, the plan argues nothing will be done to alter existing support programs or endanger existing emergency power supply programs or policies. In theory, this sounds reasonable since electricity "is a fundamental component of modern day living," 42 as the Staff Report argues. But the report ignores some of the problems posed by current universal service subsidies.

Policy makers should understand that the greatest universal service program is a fully competitive marketplace that offers consumers a myriad of service options at affordable prices. While no one would disagree that electricity is vital commodity central to the lives of every citizen, so too is food—yet policy makers have never demanded command-and-control regulations and mandates to deliver it to citizens at reasonable prices. Instead, they have relied on a vigorously competitive food and grocery sector to serve the needs of average Americans. When fears arose that some citizens were in need of assistance, targeted, means-tested programs (such as food stamps) were usually used to provide support. While such programs are far from perfect, at least they do not require the establishment of convoluted regulatory mechanisms and hidden subsidy schemes that saddle the industry with uncompetitive mandates which can make it much less efficient.

Yet, in many ways this is exactly what has happened in the utility sector with both telecommunications and electricity providers. Policy makers have come to view these private firms as vehicles through which certain social policies can be achieved. This is unfortunate since it has only made these industries less competitive and done little to actually insure that those individuals who are most in need of assistance receive it. Therefore, while there certainly is no constitutional right to receive cheap electricity, policy makers will still, nonetheless, be concerned about very low-income individuals who may have problems paying their bills. In such cases, instead of forcing more mandates and requirements on private providers—such as "carrier of last resort" requirements—legislators should look to devise targeted and strictly means-tested assistance programs for individuals below the poverty level.

Recommended Action #9: Do not impose any type of "carrier of last resort" requirements on any carriers.

Recommended Action #10: Any assistance that is deemed necessary should be targeted, means-tested and delivered through more pro-competitive voucher-like mechanisms that will not greatly distort market activity.

Although the Michigan Public Service Commission is to be commended for advancing an electricity deregulation proposal before many other states have even considered a plan, the MPSC Staff Report is not without its flaws. Most of these difficulties can be corrected quite easily, but the Commission’s plan to bail out the potential future losses of the state’s utilities will need to be completely reworked if consumers are to be treated fairly. The major recommendations of this paper are as follows:

Recommended Action #1: Grant all consumers choice immediately.

Recommended Action #2: Eliminate transitional price controls on final retail prices.

Recommended Action #3: Establish a simple, transitional transmission access pricing rule that compensates holders of the lines only for the actual cost of using those lines. Sunset such transitional rules once competition takes hold and the market power of the current monopolists has dissipated.

Recommended Action #4: Disallow all stranded cost claims for compensation except in the rare cases where a utility can prove beyond doubt that the investment was forced upon them by the PSC or the legislature.

Recommended Action #5: Allow utilities to securitize their losses if they want, but do not guarantee them a revenue flow to pay back the bonds via additional transmission fees or charges on captive ratepayers.

Recommended Action #6: Do not preemptively mandate a single transmission system or structure on the industry. Allow market participants to voluntarily work together to establish an efficient regional transmission system.

Recommended Action #7: Work in conjunction with the FERC and federal policy makers to work out interstate reciprocity concerns. Allow for some federal role in this process to ensure the harmonious development of nationwide competition.

Recommended Action #8: Ensure that the pro-environmental benefits of competition manifest themselves by giving all customers the choice to shop for green power immediately, and by denying stranded cost recovery for inefficient utility investments.

Recommended Action #9: Do not impose any type of "carrier of last resort" requirements on any carriers.

Recommended Action #10: Any assistance that is deemed necessary should be targeted, means-tested and delivered through more pro-competitive voucher-like mechanisms that will not greatly distort market activity.

Other issues and recommendations not discussed in the MPSC Staff Report deserve discussion.

The Commission has ignored the issue of how municipal utilities or "MUNIs" fit in the competitive future. While the Commission argues it has no regulatory authority over such municipally owned utility monopolies, it does not follow that it cannot take action to encourage the MUNIs to come into the competitive fold. The Commission could "fence in" the municipalities if they do not allow other utilities access to the MUNIs’ captive customers. In other words, if a MUNI refuses to allow Consumers Energy, Detroit Edison, or any other power company to voluntarily interact with consumers within their municipal service territory, the MPSC could then disallow attempts by the MUNI to offer service outside their existing franchise territory. This would encourage consumers held captive to a MUNI’s territorial monopoly to demand that the municipality offer new competitors the chance to serve their homes and businesses.

Two other recommendations made by the Michigan Jobs Commission were seemingly ignored or forgotten by the MPSC. First, the MJC recommended that the state provide leeway for merger, alliance, acquisition, and joint venture activity to take place as deregulation unfolds. Since there has been a clear rise in the volume of merger and alliance activity nationwide over the past year, it would not be surprising if certain Michigan utilities soon began looking for partners as well. While some policy makers might fear such arrangements, they should allow these mergers and alliances to move forward and turn their attention to guaranteeing that all customers have the ability to shop around for service as soon as possible. This will allow beneficial mergers and alliances to develop while simultaneously keeping the overall market power of any one company in check.

The MPSC chose not to discuss another Jobs Commission recommendation—reform and restructuring of the MPSC itself. It is never easy for a regulatory body to voluntarily surrender authority or power to market forces as deregulation unfolds, but for the sake of a more competitive market, it will have to do so in the future. The MPSC should be willing to make good faith efforts to streamline its operations in the near term and prepare to make more substantial reforms in the long term. However, legislative action will probably be required to complete this task since the Commission will probably be reluctant to do so on its own.

The simplest step the legislature could require to advance this goal would be a 50 percent reduction of the Commission’s budget within five years. Eliminating redundant or obsolete regulatory functions would advance such an agenda—policy makers must learn to trust the regulatory forces of consumers and the market instead of regulators and their mandates, if a free market in electricity is ever to truly develop in Michigan. Taking such steps in conjunction with the other reforms outlined above will ensure that a brighter future lies ahead for all Michigan electricity consumers.

Access: The ability to use transmission/distribution facilities that are owned or controlled by a third party, usually a monopolistic investor-owned utility.

Access charges: Fees charged by the owner of a transmission/distribution network to independent producers that want to gain access to the grid.

Bundling: The combination of generation, transmission, and distribution services into a packaged whole that is sold at a single rate to customers. (Also see "Unbundling.")

Co-op: Industry jargon for a cooperative electric utility. A co-op is a common form of business organization owned and operated by a group of individuals, businesses, and organizations in similar occupations. Co-ops are located primarily in rural areas and are exempt from federal, state, and local taxes. Most co-ops received their initial funding from the Rural Electrification Administration.

Demand side management (DSM): Entails efforts of utilities to encourage conservation of electricity usage, including demand and consumption patterns. Many of these demand/load management measures have been required, or strongly encouraged, by regulators.

Distribution facilities: Equipment used to deliver electric power at lower voltages from the transmission system to the final user. Although considered a distinct segment of the market, distribution facilities generally can be grouped with transmission facilities because these assets perform a similar function that is wholly distinct from generating facilities.