(Note: The following was adapted from a 2003 essay by Lawrence W. Reed.)

Should Michigan extend its sales tax to services as a way to close the state’s budget deficit? According to Gov. Jennifer Granholm, who has proposed a 2 percent sales tax on services, the answer is a resounding "yes." But to many struggling people and businesses in the state, the prospect of higher taxes is unsettling.

Expanding the sales tax base to include services is a tempting plum for legislators longing for those heady days when money flowed into Lansing like water. There are more than 100 services that could be newly taxed under this plan. Haircuts, tax return preparation, dating services, veterinary care and financial planning are among the long list of services that would be taxed.

A new tax on any number of those services would almost surely become a permanent stream of new revenue that would be used for more than just budget balancing in the near-term. In fact, if the governor gets her 2 percent now, and if past experience is any guide, Michiganians can count on her or some future governor coming back for more. Gov. Granholm is not asking for the new tax just to plug a revenue hole — she also wants to spend a billion dollars more than the state spent last year.

Even if revenue from taxing services went to deficit reduction dollar for dollar, this is still an idea that carries substantial baggage. When Florida in 1987 extended its 5 percent sales levy to most services, 240 new full-time government enforcement jobs had to be created. Massive and expensive "education" programs were planned to dispel confusion and raise the expected first-year compliance rate of only 65 percent.

But the unworkable tax never made it to its first anniversary. It was killed by an outraged citizenry, a chastened legislature and a thoroughly embarrassed governor. That experience is a major reason why you can count on one hand the number of states which levy a broad-based and comprehensive sales tax on services.

Taxing services in Michigan would have especially detrimental effects on small businesses, which routinely contract out for bookkeeping, accounting, office equipment repair, janitorial, legal, computer and a host of other service activities. A large competitor can often provide such things in-house, thereby avoiding a sales tax. This should concern us, since the lion’s share of new jobs are created by small businesses.

Economists have shown that sales tax collection and compliance costs rise as the size of the business decreases. Small, family-run firms experience compliance costs that can be four to five times greater than those incurred by their big competitors.

A 1987 study by the American Legislative Exchange Council pointed out that the regressive impact of the sales tax on low-income people would be further magnified with its application to services. It would show up in their medical, dental and legal bills, for instance. Taxes on construction services would surely price some of them out of the housing market.

Adding Michigan’s service firms to the sales tax rolls would dramatically boost the state’s own administrative costs. Florida’s short-lived tax instantly increased the total number of registered vendors by 75 percent. In Iowa, the figure was 60 percent. Inevitably, the normally high rate of delinquency and audit costs that all states incur when they deal with smaller firms would only worsen.

Across Michigan, residents are coping with the challenges of an ailing economy. And they are coping by re-examining their spending. They are prioritizing and doing without some things they’d love to have. They are hiring less, spending less, taking fewer and shorter vacations closer to home. They are stretching further the dollars they have, and generally exerting the discipline necessary to weather the storm. Why should state government do otherwise?

When asked in a recent radio interview why she proposed so many new expansions of government in her February State of the State address, Gov. Granholm quickly snapped, "It is exactly the time to do it." She referred to her billion-dollar spending spree as "investments." Many cash-strapped, job-hunting Michiganians probably wondered what planet she was broadcasting from. Her remarks reminded me of something then-Arkansas Gov. Bill Clinton said back in 1988: "There’s a lot of evidence that you can sell people on tax increases if they think it’s an investment."

If state government refuses to adjust its priorities and raises taxes to balance its budget, it should be incumbent on every lawmaker to tell Michigan residents where to cut their own budgets to make ends meet.

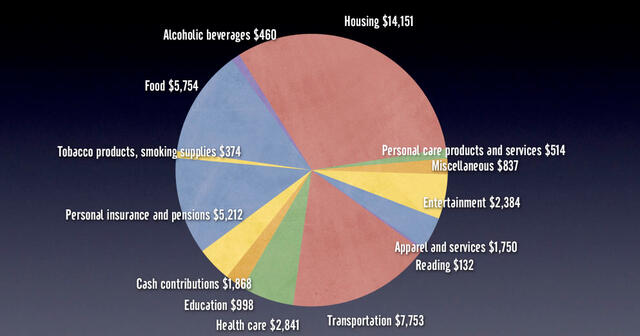

Where does the government expect families to sacrifice so the state doesn’t have to? Should they buy less food? Should they purchase less health care? Michigan taxpayers simply do not need to be taxed further. There are further efficiencies to be wrung from the state budget.

Gov. Granholm’s tax hike proposal comes right from the playbook of the Michigan Education Association, which led a coalition calling for a sales tax on services in 2003. The MEA also doesn’t want reforms to its Rolls Royce employee health insurance scheme, which is lucrative for the MEA’s political coffers, but monstrously expensive to struggling school districts. None of the state’s unions support repeal of the archaic Prevailing Wage Act, which inflates construction and renovation costs to state and local governments in Michigan by at least $200 million annually. Rather than finding savings within government, the governor would prefer to soak taxpayers even more, assuring them it will be good for the economy.

Extending the sales tax to services is a bad idea. It’s an evasion of responsibility. It’s utterly unnecessary and will likely result in greater job losses in, and migration from, the Great Lake State. Here’s a novel alternative: How about some leadership instead of tax hikes?

#####

Lawrence W. Reed is president of the Mackinac Center for Public Policy, a research and educational institute headquartered in Midland, Mich. Permission to reprint in whole or in part is hereby granted, provided that the author and the Center are properly cited.

The Mackinac Center for Public Policy is a nonprofit research and educational institute that advances the principles of free markets and limited government. Through our research and education programs, we challenge government overreach and advocate for a free-market approach to public policy that frees people to realize their potential and dreams.

Please consider contributing to our work to advance a freer and more prosperous state.