The proposed “Stop Overspending” state constitutional amendment, which failed to gain ballot status in the November 2006 election, addressed four major areas ...

The proposed "Stop Overspending" state constitutional amendment, which failed to gain ballot status in the November 2006 election, addressed four major areas:

capping the annual increase in state spending at the percentage sum of annual inflation growth and population growth;

depositing 50 percent of any surplus state revenues into the state budget stabilization fund, up to a total fund balance of 10 percent of total state spending from state resources, and allowing withdrawals only when annual state revenues were less than the state spending cap established in the first provision above;

preventing the sale of certain types of local bonds without voter approval; providing a definition distinguishing taxes from fees; requiring that special tax assessments be subject to voter approval; extending the statute of limitations for challenging potentially unconstitutional taxes; and preventing so-called "preapproval" of property tax rollback "overrides"; and

prohibiting state legislators from receiving state-funded pensions.

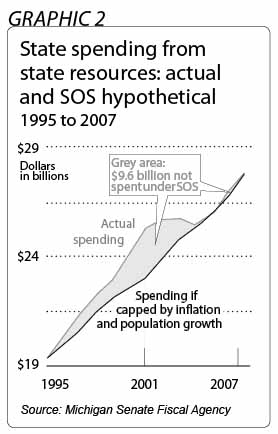

Total state spending from state resources (as opposed, for instance, to federal government resources) was about $19.3 billion in fiscal 1995 and more than $25.2 billion in fiscal 2001, a total growth of more than 30 percent.* During the same period, the sum of the inflation rate and the state’s population growth rate was less than 20 percent. If the SOS proposal had taken effect in fiscal 1995, the state budget would have been more than $2.2 billion smaller, or about 9 percent less, in fiscal 2001 than it actually was. In addition, because the SOS proposal would have precluded the rapid rise in state spending from fiscal 1995 to fiscal 2001, state government would have spent approximately $9.6 billion less from fiscal 1995 to fiscal 2007. The proposal would have required that an estimated $8 billion of this $9.6 billion be returned to taxpayers as annual income tax refunds.

Because the spending cap would have continued to rise, however, and because actual Michigan state spending declined after fiscal 2001, the spending cap and actual state spending in fiscal 2007 would have differed very little. If the SOS proposal had been in effect, fiscal 2007 state spending from state resources would have been just one-quarter of one-percent less than spending in fiscal 2007 is currently budgeted to be.

Michigan’s budget stabilization fund had a balance of almost $1.3 billion in fiscal 2000. It is effectively empty today. Under a hypothetical SOS proposal, the budget stabilization fund would have contained more than $2.2 billion by fiscal 2001 and almost $2.5 billion after a likely withdrawal from the fund in fiscal 2005. Under the SOS proposal, it appears that after 2001, state government would have had a larger budget stabilization fund and experienced diminished surpluses, rather than larger deficits.

|

* Sources for the findings cited in the executive summary are provided in endnotes to the main text of this Policy Brief. |

The Stop Overspending initiative has been compared to Colorado’s "Taxpayer’s Bill of Rights." TABOR, as the Colorado provision is commonly abbreviated, is a 1992 amendment to the Colorado Constitution that usually caps the annual percentage growth of Colorado’s state spending and revenue at the sum of the percentage rates of inflation and population growth.

TABOR and the SOS proposal are similar in two ways: Both use the inflation-and-population standard to regulate the growth of state spending, and both contain some local taxpayer provisions like those mentioned above. TABOR and SOS are also dissimilar in several ways: TABOR is more strict in restraining state spending, since TABOR includes more state revenues, such as tuition paid to state colleges, towards the spending cap; TABOR does not permit a budget stabilization fund comparable to what would have existed under the SOS proposal; TABOR does not require withdrawals from the budget stabilization fund when state revenue is less than the spending limit; and TABOR "ratchets down" Colorado’s annual spending limit to the actual spending level for any year when state revenue lags, while the SOS proposal would simply have kept the current (higher) spending limit in place.

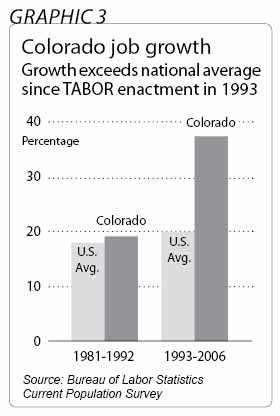

The implementation of TABOR coincided with strong economic growth for Colorado. Even after a pronounced recession beginning in 2001, Colorado’s job growth from 1993 to 2006 was nearly 38 percent, or almost 690,000 new jobs, according to data from the U.S. Bureau of Labor Statistics. This increase substantially eclipsed the 20 percent national job growth for the same period. In contrast, in the 10-year period prior to TABOR’s enactment, the nation added 18 percent to its jobs base, and Colorado added a more average 19.1 percent.

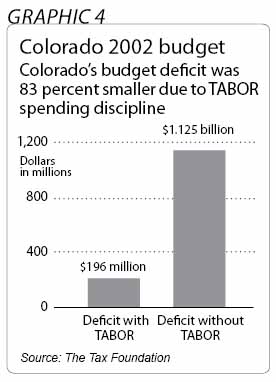

The Washington, D.C.-based Tax Foundation has observed that by preventing Colorado state government from increasing state spending rapidly prior to 2001, TABOR appears to have mitigated the budgetary challenges that could have appeared after 2001. In 2002, when Colorado’s total state revenues declined by more than $1 billion, the state budget faced a deficit of about $196 million — considerably less than the $1.1 billion deficit the state might have faced absent TABOR’s spending limitations.

U.S. Census Bureau data show that from 1993 to 2005, Colorado’s population increased 29 percent, a rate more than twice the national average. The Washington, D.C.-based Heritage Foundation also found that measures of per-capita personal income growth and per-capita gross state product show Colorado lagging the national average in the decade prior to TABOR and then significantly outperforming the average in the decade afterward.

By some measures, Colorado state government spending on such programs as health care and education is below the national average. The United Health Foundation nonetheless ranks Colorado as the 17th healthiest state in the nation for 2005 — 9.7 percent above the national average. In 2003, Colorado’s primary and secondary school students scored 15th highest in the nation on the National Assessment of Educational Progress, a ranking mostly unchanged from 1992, prior to the implementation of TABOR.

Michigan state government would have spent an estimated $9.6 billion less from fiscal 1995 to fiscal 2007 if the SOS proposal had been in effect. These state spending reductions would have meant fewer state programs and activities, but there is also economic evidence that lower taxes aid in the creation of economic activity and jobs.

The necessity for some of the $9.6 billion in spending was called into question by many of the lawmakers themselves. The majority party in the state House of Representatives convened a task force in 2000 to examine potential cases of government waste in the 1999 budgets and issued a report that classified more than $131 million worth of spending for that year as "non-essential."

Some have argued that the SOS spending cap would be ill-suited to state government, since government purchasing is disproportionately concentrated on such items as health care and education, which increase faster than the official inflation rate. This argument should be balanced against two additional observations: Individual and business taxpayers must bear such costs as rising health care as well, and much of the rising cost of a government good like public education appears to be the result of its being a government enterprise. The fact that government spending on a government enterprise is rising quickly compared to private-sector spending could easily be an argument in favor of the state spending cap, rather than against it.

It does not appear that the SOS provision to end publicly funded pension plans for state legislators would have put the pay of legislators in Michigan below that of legislators in other states. Michigan is one of a dozen or so states with a full-time legislature (an exact count depends on how "full-time" is defined). Michigan lawmakers are the second-highest compensated state lawmakers in America. They presently receive more than $79,000 per year in base salary, and they are permitted an expense account for $12,000 more. About half of all states pay a base annual salary of less than $20,000.

On July 10, 2006, a ballot committee calling itself "Stop Overspending (SOS)" filed a ballot petition with the Michigan Bureau of Elections to place before the state’s voters a proposed constitutional amendment that would have, among other things, capped annual state spending increases. The state Board of Canvassers later rejected the petition because of insufficient signatures.

The proposal appears to have been modeled on a Colorado constitutional provision that has been in effect since 1993. Attempts were made to place similar proposals on ballots in several other states in 2006, and at the time of this writing, a spending cap had been successfully placed on the state ballot in Maine.

Given the breadth of the SOS proposal and the possibility that a comparable proposal might be put before Michigan voters on a future ballot, the study below reviews the proposal and considers what its impact would have been in Michigan.

The proposal sought to accomplish four objectives, which are explained in detail below.

The SOS proposal would have capped the annual increase in state spending. State revenue (as opposed to state spending) is already limited by a provision in the Michigan Constitution popularly known as the "Headlee amendment." The Headlee amendment also acts as a spending limit because of Michigan’s constitutional requirement that the annual state budget be balanced.

The Headlee amendment restricts the annual revenue raised from Michigan taxpayers to no more than 9.49 percent of their combined annual personal income. If tax revenues exceed this dollar amount by more than 1 percent, the amendment requires state government to send refunds to income and business taxpayers in proportion to the taxes they paid. Exceptions to this refund requirement are permitted in certain emergency circumstances, but these are narrowly defined and have never been invoked.†

Federal funds are not counted when calculating the Headlee amendment’s revenue limit; they would also have been exempt from the spending limit in the SOS proposal. Federal aid represented 32 percent of the fiscal 2006 state budget, largely for a variety of restricted spending purposes.

For fiscal 2006, the estimated Headlee limit is $30.76 billion. State spending subject to the Headlee limit is expected to be $25.97 billion — about $4.79 billion less than the cap.[1]

If enacted, the SOS proposal would have constitutionally capped the annual increase in state spending to the sum of the percentage increases in inflation and in state population for the previous year. If, for instance, the previous year’s inflation rate had been 3 percent and the increase in Michigan’s population had been 2 percent, then state spending could not have increased by more than 5 percent from the previous year. In instances of deflation or falling state population, the declining component would not have been used to calculate the allowable spending limit for the following year.

Thus, the SOS proposal’s limit on state spending increases would have adjusted state spending upward or, in the exceptional case of deflation and no state population growth, kept state spending constant. The proposal would not have ratcheted state spending down to a lower spending limit.

Whenever state revenue, together with withdrawals from the state budget stabilization fund, did permit state spending to match the SOS spending limit, the current SOS spending limit would have become the spending limit for the next year and for each succeeding year thereafter until revenues again reached the limit.‡ At that point, the spending limit for the following year would have again increased by the sum of the percentage increases in population and inflation.

The SOS spending limit would have been an addition to, not a replacement of, the existing Headlee revenue limit. However, because the Headlee revenue limit is adjusted for the state’s aggregate personal income, which traditionally has grown faster than population and inflation combined, the likely practical effect of the SOS proposal would have been a spending limit that was more strict than the Headlee revenue limit.

|

† Article 9, Section 27, of the Michigan Constitution states: “The revenue limit of Section 26 of this Article may be exceeded only if all of the following conditions are met: (1) The governor requests the legislature to declare an emergency; (2) the request is specific as to the nature of the emergency, the dollar amount of the emergency, and the method by which the emergency will be funded; and (3) the legislature thereafter declares an emergency in accordance with the specific [sic] of the governor’s request by a two-thirds vote of the members elected to and serving in each house. The emergency must be declared in accordance with this section prior to incurring any of the expenses which constitute the emergency request. The revenue limit may be exceeded only during the fiscal year for which the emergency is declared. In no event shall any part of the amount representing a refund under Section 26 of this Article be the subject of an emergency request.” |

|

‡ Because of the SOS proposal’s budget stabilization fund provision (described under “Refunds to Taxpayers and Payments to the Budget Stabilization Fund”), the cap would always have been met and reset for the following year whenever state revenues and state budget stabilization monies were sufficient to meet the spending cap. This appeared to be true regardless of lawmakers’ spending decisions. |

Refunds to Taxpayers and Payments to the Budget Stabilization Fund

In any year in which revenue exceeded the proposed spending limit, the SOS proposal would have returned at least 50 percent of the surplus to taxpayers, with each receiving an amount proportional to the personal income taxes he or she paid. The SOS proposal would have removed the Headlee provision granting refunds to business taxpayers.

The remainder of any revenue surplus — but never more than 50 percent for any given year — would have been deposited in the state budget stabilization fund. If the stabilization fund’s balance had reached 10 percent of the current year spending limit, any remaining tax revenue surplus would have been rebated back to the taxpayers according to the formula detailed above.

In sum, the SOS proposal would have restricted the percentage increase in state government spending to the combination of inflation and state population growth. It would have mandated that up to 50 percent of any state revenue exceeding the proposal’s spending limit be placed in a budget stabilization fund that would have been allowed to grow to 10 percent of that year’s state spending limit.∂ The proposal would also have required that at least 50 percent of all annual revenue surpluses be rebated to taxpayers, and that up to 100 percent of the surplus be rebated to taxpayers whenever the budget stabilization fund had reached its maximum mandated annual size.

|

∂ The SOS proposal did not stipulate how the substantial monies that could have accumulated in the budget stabilization fund might have been invested. |

Definition of "Revenue"

From 2000 through 2005, the state received more than $1.8 billion from a lawsuit settlement against the U.S. tobacco industry. Annual payments from this suit have ranged from a low of $261 million to a high of more than $350 million. This tobacco money and some other recent sources of nontax state revenue are not counted as part of the Headlee revenue limit. The Headlee limit therefore does not curb state expenditures as much as it would if these other sources of state income were considered.[2]

The SOS proposal would have altered the existing Headlee language so that the definition of "total state revenues" specifically included the tobacco settlement money and "any (revenue) source now in existence, or created or identified in the future." As noted earlier, federal funds would have been exempt from the SOS proposal’s spending cap, just as they are under the Headlee revenue cap. Several other exceptions to the Headlee cap would also have been kept by the SOS proposal,¶ such as revenue from voter-approved bonds for capital construction projects and monies for state-administered pension and insurance plans. The state treasurer’s mandatory transfers from the budget stabilization fund (detailed below) also would not have counted toward the calculation of "total state revenues" under the SOS proposal.

|

¶ The list of exceptions is lengthy and specialized. Article 9, Section 33, of the Michigan Constitution stipulates, “‘Total State Revenues’ includes all general and special revenues, excluding federal aid, as defined in the budget message of the governor for fiscal year 1978-1979.” Thus, the exceptions include the line items in that gubernatorial budget message, as well as a variety of state funds detailed in Article 9. |

Exceptions to the Spending Limit

The Headlee revenue limit may be exceeded for one year, provided that the governor declares an emergency, states a specific reason for exceeding the limit, specifies the specific amount needed and proposes a specific means of raising the additional money (such as a tax increase). The Legislature must then approve this request by an affirmative vote of two-thirds of each chamber. To date, no governor has ever made such a request. The SOS proposal would have narrowed the constitutional definition of "emergency" in both the Headlee and SOS limits to include only instances involving "an imminent threat to public health or safety."

The SOS proposal would also have added a new mechanism for exceeding both the revenue limit and the proposed spending limit. With a two-thirds vote from both the state House and the state Senate, a request to collect and spend above the Headlee revenue and SOS spending limits could have been submitted to the voters for their approval at a November general election. While the request would not have required a reason or purpose for the additional spending, such as an "emergency," the following statement would have had to appear in the ballot language presented to voters: "A ‘yes’ vote on this measure will authorize the state to retain extra taxes and spend them in excess of constitutional limits by [insert amount of predetermined maximum additional spending]."

It is important to note that if such a request had been granted by voters on an election day for either president or governor, the approved additional spending would have been counted as a permanent upward adjustment to the spending limit, regardless of the inflation and population adjustment for that year. Alternatively, if voters had approved the request in another general election (i.e., odd-year November elections), the resulting upward adjustment in spending would have counted only for that particular year — a one-time source of additional revenue that would not have affected the spending limit of subsequent years.

The state budget stabilization fund, popularly known as the "rainy day fund," is a state budget account that is discussed in the Michigan Constitution. The fund is like a savings account in which state government can deposit surplus revenues during favorable economic times. The fund is intended to provide additional monies during declines in state revenue, though the Legislature and the governor have sometimes changed the law governing the fund to allow withdrawals for reasons other than this original purpose.

The SOS proposal not only would have mandated that a fixed percentage of surplus revenue be dedicated to the fund (described above in "Refunds to Taxpayers and Payments to the Budget Stabilization Fund"), but also would have eliminated the Legislature’s political authority to withdraw money from it. Only the state treasurer would have been constitutionally permitted to withdraw money from the fund. He or she would have been allowed to do so when, and only when, total state revenues for the year had not proved sufficient to allow state spending to match the spending limit; moreover, in these circumstances, he or she would have been required to remove enough money to meet the cap (if possible), but to withdraw no more than that amount.

Taxpayers and local governments have had several legal battles over the meaning of the Headlee amendment’s restrictions on the taxation authority of government.** A number of the SOS proposal’s modifications appear to be efforts to clarify Headlee language.

|

** In 1994, the “Headlee Blue Ribbon Commission Report,” requested by Michigan Gov. John Engler, examined many of these disputes. The Headlee Blue Ribbon Commission had members representing taxpayers, state government and local government. The commission’s opinion regarding local government disputes with taxpayers was not always unanimous. The official report of the commission states all sides of these disputes and issues conclusions from both the majority and minority perspectives. A copy of the “Report of the Blue Ribbon Commission on the Headlee Amendment” may be obtained from the Michigan Department of Treasury. Substantial excerpts of the report have been posted online by the Anderson Economic Group at http://www.andersoneconomicgroup.com/modules.php?name=Content&pa=display_aeg&doc_ID=1537. |

Limited Tax General Obligation Bonds

The Headlee amendment allows an exception to its revenue limitation in the case of voter-approved bond sales. The purpose of this exception is to allow taxpayers a chance to vote on any local government proposal that obligates them to pay for future spending.

Some local governments have adopted the practice of selling a particular type of bond — "limited tax general obligation bonds" — without the consent of the voters. These bonds are repaid out of tax revenue that local governments already have the authority to levy. The sale of these bonds does not violate the Headlee restriction for the current year or necessarily even create a tax increase for that year, but the bonds nonetheless create a long-term payment obligation for taxpayers, just as voter-approved bonds do.[3]

The SOS proposal would have prohibited this practice and require that this type of long-term borrowing be subject to voter approval.

Special Assessments and User Fees

The Headlee amendment requires voter approval before a local government can create a new tax or increase the maximum allowable rate of an existing tax. The definition of a "tax" has thus been a matter of legal dispute, particularly on the question of distinguishing "user fees" and "special assessments" from "taxes."

A pivotal court case involved the Lansing city government’s creation of a system to separate the city’s storm water runoff from the city’s sewer water. To pay for this system, Lansing implemented a charge against property owners without seeking voter approval.

City officials argued that the charge was a "user fee," rather than a tax. The levy entered popular understanding as the "rain tax," however, and following a lawsuit by a Lansing taxpayer, the Michigan Supreme Court in 1999 agreed that the charge was a tax requiring voter approval, in part because "users" had no ability to cease receipt of the service or control the amount that they used.[4]

The SOS proposal would have placed the following definition of the term "mandatory user fee" in the state constitution: "‘Mandatory user fee’ means a compulsory obligation to pay for goods or services under circumstances where the user does not have the absolute discretion to choose how much of the good or service to use, or whether to use it or buy it at all, without giving up common law rights incidental to private property ownership." The proposal would have required voter approval for these fees, while the decision to increase voluntary user fees would have remained with local officials.

The SOS proposal would also have added "special assessments" to the list of government levies that would have needed voter approval. "Special assessments," unlike the general property taxes charged on the value of a property, are levied proportional to a specific benefit provided to a property. For example, a special assessment for new streetlights might bill each nearby store owner based on the number of lights in front of his or her building. Properties that are not located near the lights and not receiving a direct benefit from them would not be taxed.

Headlee "Rollbacks" and "Preapproval"

The Headlee amendment requires an automatic reduction in the rate of local taxation when property values increase faster than inflation (this automatic tax reduction does not apply to state education property taxes).[5] This automatic reduction is commonly known as a "Headlee rollback" and has the effect of limiting the growth of local government tax revenues to only the value of new construction and the growth in inflation. However, with voter approval, commonly known as a "Headlee override," local governments are permitted to forgo the rollback and continue levying the current tax rate.

In advance of this automatic tax rate reduction, some taxing jurisdictions have been requesting "preapproval" from voters for tax rates that exceed what is presently allowed by law, but that exactly equal an impending Headlee rollback. Although the higher tax rate cannot be levied right away, the local government institutes the new tax after the Headlee rollback takes effect, thereby keeping the tax rate constant. The SOS proposal would have no longer permitted this "preapproval" practice.

Statute of Limitations to Challenge Headlee Violations

The Michigan Constitution does not currently specify how much time taxpayers have to challenge an alleged violation of the Headlee amendment. In the absence of constitutional language, courts have imposed a one-year statute of limitations on Headlee-based lawsuits. The SOS proposal would have instituted a three-year statute of limitations for challenging Headlee and SOS violations, giving taxpayers two additional years in which to sue.

Michigan lawmakers currently receive a taxpayer-funded matching contribution for the money they place in a state-administered 401(k) retirement fund. The SOS proposal would have prohibited state lawmakers elected after January 31, 2007, from receiving any pension or other retirement benefits that are financed by Michigan taxpayers or other state revenues.

The SOS proposal is in large part a response to several state budget trends. Four of these trends are reviewed below, and an analysis of the proposal follows after.

This discussion of the state budget begins with fiscal 1995. Starting with an earlier year would likely produce similar observations, but comparisons of the pre- and post-1995 state budgets involve serious practical difficulties because of the significant constitutional changes created by the passage of Proposal A of 1994 (a landmark state constitutional amendment involving public school finance). In adopting fiscal 1995 as a starting point, this study is following the example of the Michigan Senate Fiscal Agency, which likewise chose fiscal 1995 as the starting point for its analysis of the SOS proposal.

State spending in Michigan since fiscal 1995 can be separated into two distinct phases, with fiscal 2001 serving as a watershed. The first phase occurred during a time of rising state tax revenues and economic strength; the second phase occurred during a time of falling tax revenue and economic decline.

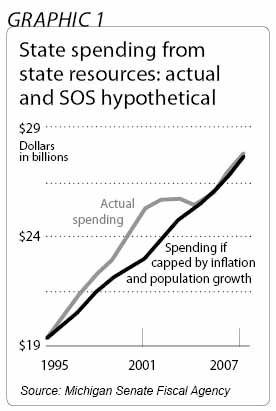

From fiscal 1995 through fiscal 2001, state spending grew along with rapidly rising state tax revenues and a strong Michigan economy. According to the Michigan Senate Fiscal Agency, total state spending from state resources (as opposed to, for instance, federal government resources) was about $19.3 billion in fiscal 1995 and more than $25.2 billion in fiscal 2001, a total growth of more than 30 percent. During the same period, the sum of the inflation rate and the state’s population growth rate was less than 20 percent. Thus, if the SOS proposal had been in effect in fiscal 1995, the fiscal 2001 state budget would have been more than $2.2 billion smaller, or about 9 percent less, than it actually was (see Graphic 2).[6]

State government spending changed with the national recession in 2001. Michigan jobs and capital declined, and state government tax revenue fell as well. This problem has persisted since fiscal 2001. State spending from state resources declined significantly against inflation over the next six years, growing less than 10 percent from fiscal 2001 to the recently approved budget for fiscal 2007, while total inflation and population growth for the period was 20 percent.[7] In fiscal 2004, state revenue collection lagged so much that total state spending from state resources fell more than $250 million from what had been spent the year before.[8]

The Michigan Senate Fiscal Agency estimates that implementing the SOS proposal’s state spending cap in fiscal 1995 would have produced a fiscal 2007 state spending limit of $27,674,900,000. The actual spending level appropriated for fiscal 2007 is $27,743,200,000.

Hence, if the SOS proposal had been in effect, fiscal 2007 state spending from state resources would have been just one-quarter of one-percent less than spending in fiscal 2007 is currently budgeted to be. At the same time, with the upward spike in annual state spending from fiscal 1995 to fiscal 2001 prohibited by the SOS spending cap, state government would ultimately have spent approximately $9.6 billion less in total from fiscal 1995 to fiscal 2007 under the SOS proposal. The proposal would have required this $9.6 billion surplus to be divided between taxpayer refunds and deposits into the budget stabilization fund.[9]

The budget stabilization fund had a balance of almost $1.3 billion in fiscal 2000. The fund is effectively empty today, the money having been spent from fiscal 2001 through 2003 when state tax collections were no longer keeping up with the spending pace that had been established in the late 1990s. As noted above, the actual total state spending from state resources for fiscal 2001 was more than $2.2 billion higher than it would have been if the SOS cap had been placed on state spending in fiscal 1995.[10]

Assuming the fiscal 1995 enactment date for the SOS proposal hypothesized by the Michigan Senate Fiscal Agency, and assuming that all historical economic and tax collection facts remained constant, the SOS proposal’s spending limits from fiscal 1995 through fiscal 2000 would have led to almost $4.3 billion less state spending from state resources.[11] The rules of the SOS proposal would have required that portions of this surplus be deposited annually into the budget stabilization fund until the fund level reached 10 percent of the annual state spending limit. The maximum 10 percent balance would have been achieved by at least 1999 with a total of just over $2.2 billion; the fund’s balance then would have grown with inflation and population each year to mirror the growth of the SOS spending limit. By fiscal 2001, under a hypothetical SOS proposal, the budget stabilization fund would have contained about $2.3 billion — more than $1 billion higher than the fund’s actual balance.[12]††

This trend of producing a slow increase in the fund’s balance would have continued in every year to the present except for fiscal 2005, the only year when the tax money collected would have failed to equal the spending limit. In fiscal 2005, state revenues from state resources would have dipped below the allowable spending limit by $31.2 million, about one-tenth of one percent less than that year’s hypothetical SOS cap. The state treasurer would have made an automatic withdrawal to supplement spending. After this withdrawal, the budget stabilization fund would have contained almost $2.5 billion.[13] Thus, if all other factors had remained constant, and if the SOS proposal had been implemented in fiscal 1995, it appears that after 2001, state government would have had a larger budget stabilization fund and experienced diminished surpluses, rather than larger deficits.

|

†† There are several assumptions that make this a conservative estimate of the outcome. The budget stabilization fund balance was calculated only as direct deposits based upon the surplus figures reported by the Michigan Senate Fiscal Agency. Obviously, the fund is invested and earns interest, but these gains — while likely significant — were not calculated into the size of the hypothetical fund balance following fiscal 1995. Adding these monies would have led to a budget stabilization fund that achieved its maximum amount much sooner and required smaller annual deposits to maintain the fund balance year to year. As such, the portion of the surplus dedicated to taxpayer refunds would have likely been larger. |

The Stop Overspending initiative has been compared to Colorado’s "Taxpayer’s Bill of Rights," a 1992 amendment to the Colorado Constitution. The amendment, commonly referred to by the acronym "TABOR," was implemented in 1993. TABOR regulates the growth of Colorado’s state spending and revenue, capping it in most years at the sum of the percentage rates of inflation and population growth. In this, TABOR resembles the SOS proposal.

TABOR, however, contains different local taxpayer provisions than the SOS proposal does, and TABOR does not contain the state lawmakers’ pension provision discussed earlier. Even TABOR’s spending cap and treatment of state surpluses do not quite match the details of the SOS proposal. The TABOR cap in its original form (the amendment was modified in fiscal 2005) thus shares an important similarity and three significant differences with the SOS proposal.

The most significant similarity between TABOR and the SOS proposal is that both use the inflation-and-population standard to regulate growth of a state spending limit. This provides a point of comparison regarding the SOS proposal’s potential impact on state spending.

Revenue taken from Colorado taxpayers did not exceed the TABOR limit from 1993 to 1996, the first four years after TABOR’s implementation. From 1997 to 2001, TABOR produced a total surplus of about $3.25 billion, all of which was refunded to Colorado taxpayers. The approximate total refund for a household of four people was $3,200.[14]

Unlike TABOR, the SOS proposal would have sometimes placed surplus state tax revenue in a budget stabilization fund, rather than returning it to taxpayers. The fact that the SOS proposal would have established a larger budget stabilization fund would have reduced the taxpayer refunds that SOS would have provided. Regardless, the estimated rebates to Michigan taxpayers through fiscal 2007 would have been about $8 billion if the SOS proposal had been in effect in fiscal 1995. This sum would have represented more than $3,000 per household of four.[15]‡‡

Thus, the total refund provided under TABOR to a Colorado household of four from 1993 to 2001 is similar to an estimated total refund provided under the SOS proposal to a Michigan household of four from fiscal 1995 to fiscal 2007. Colorado’s slightly higher figure could be the result of Colorado’s strong economic growth or of the SOS requirement that some of the surplus tax revenues be deposited in the budget stabilization fund, rather than returned to taxpayers. In any event, the similarity between the Michigan and Colorado household figures suggests some plausibility in the Michigan Senate Fiscal Agency’s estimate of a $9.6 billion surplus since fiscal 1995 under a hypothetical SOS proposal.

|

‡‡ This calculation is based on a shorthand per-capita calculation that divides the almost $8 billion in total rebates by the state’s population of about 10 million. It is thus calculated in the same way as the earlier $3,200 estimate for a Colorado household of four. Because the SOS proposal’s tax rebate is based on the amount of income tax paid, a household with no income taxpayers would not have received a rebate, while a household that included income taxpayers could have received substantially more than the $3,000. It also bears noting that lawmakers — knowing that SOS would not have allowed the state to keep this surplus revenue — could have instead elected to reduce the rate of collection of taxes other than the personal income tax (such as the Single Business Tax, for example). While this would probably not have changed the overall size of tax relief, it may indeed have changed the amount of relief awarded to any specific taxpayer. Additionally, the possibility exists that these tax reductions may have exceeded the figures cited, leading to larger tax relief, smaller surpluses and, thus, smaller deposits into the budget stabilization fund. |

One significant difference between TABOR and the SOS proposal is the type of revenue that is initially counted toward the state spending limit. In two significant ways, the original TABOR was stricter in restraining state spending than the SOS proposal would have been.

First, tuition paid by students to state institutions of higher learning was counted against the original TABOR spending cap, thus making tuition increases the equivalent of a state spending increase. This provision made the original TABOR far more likely to trigger tax rebates.[16]

As a point of comparison, tuition and fees paid to Michigan’s public universities and community colleges exceeded $2.4 billion in 2004.[17] This amount was equivalent to almost 9.5 percent of all spending that would have been counted under the SOS proposal.[18]

Additionally, from 1995 to 2006, the average in-state undergraduate tuition at Michigan’s autonomously governed public universities increased more than 98 percent — more than triple the inflation rate for the period. The SOS proposal’s exclusion of tuition and fee revenue from the calculation of a state spending limit would have made the SOS proposal substantially less restrictive than TABOR.[19]

Second, TABOR was originally drafted to include unemployment insurance taxes against its revenue base. The federal government mandates that states maintain an unemployment insurance system, and to remain solvent, the system must tax employers with a tax rate that rises and falls in inverse proportion to the strength of the economy. The inclusion of these payments in the TABOR revenue count has tended to push TABOR surpluses lower when the economy is strong and higher when the economy is weak.[20] The SOS proposal specifically excluded unemployment insurance taxes from the calculation of the revenue counted under the spending limit, thus negating the potential for this effect.

TABOR does not permit creation of a budget stabilization fund comparable to what currently exists in Michigan or to what would have existed under the SOS proposal. TABOR does require the establishment of an "emergency reserve" fund, but that fund must be maintained at 3 percent of total TABOR spending and cannot be used to address "economic conditions" or "revenue shortfalls."[21]

In contrast, the SOS proposal would require that Michigan use up to half of surplus state revenue to build a rainy day fund amounting to 10 percent of the SOS proposal spending limit. Hence, relative to state spending, the potential size of the stabilization fund under the SOS proposal would have been more than three times that of TABOR’s emergency reserve fund.

The SOS proposal would also have specifically required withdrawals from the budget stabilization fund when state revenue was less than the spending limit. Thus, state government would have used the budget stabilization fund to supplement state revenues under the SOS proposal in a way that Colorado state lawmakers cannot use the TABOR emergency reserve.

TABOR differs from the SOS proposal in the case of declining state revenues. TABOR resets Colorado’s annual spending limit to the actual spending level for any year when the state revenues available are not sufficient to reach the spending cap. The amendment also requires a popular vote to raise state taxes of any kind. Since TABOR does not allow lawmakers to tap a budget reserve when revenues lag, the spending cap can fall downwards from year to year (an outcome popularly referred to as the "ratchet effect").

As noted earlier, the SOS proposal would not have allowed the spending limit to ratchet downward to the actual spending level. Rather, the proposal would have locked the current spending limit in place for the following year whenever revenues and withdrawals from the stabilization fund did not enable Michigan lawmakers to meet the current spending limit. In addition, the substantial budget stabilization fund created by the SOS proposal would have increased the likelihood that state spending would have actually reached the spending limit in any given year.

The SOS proposal did not alter the existing authority of the governor and the Legislature to pass new taxes or to increase existing ones. If new taxes had allowed state spending to reach the SOS cap, the cap would have resumed its annual upward climb based upon population growth and inflation. The provisions of the SOS proposal would have made it unlikely that the spending limit would have remained constant for long, unless the state had suffered a serious economic decline.

Discussion of the SOS proposal in Michigan has so frequently involved TABOR and its impact on Colorado’s state budget and economy that Colorado’s experience is reviewed in some detail below. Also reviewed are the SOS spending cap’s possible effects on Michigan had the SOS proposal been in place during the past dozen years; the spending cap’s use of inflation and population; the provision eliminating pensions for legislators; and issues concerning debatable terminology in the SOS proposal.

The Colorado Economy: 1993-2001

An analysis of Colorado state spending both before and after the passage of TABOR suggests that the amendment restrained state spending growth. According to the Golden, Colo.-based Independence Institute, from 1993, when TABOR was enacted, to 2002, total state spending grew about 64 percent — more or less matching the combined total growth of population and inflation for the period. In contrast, in the decade before TABOR, Colorado spending increased nearly 90 percent — more than double the 40.1 percent combination of inflation and population.[22]

The implementation of TABOR coincided with strong economic growth for Colorado. Even after a pronounced recession beginning in 2001, Colorado’s job growth from 1993 to 2006 was nearly 38 percent, or almost 690,000 new jobs.[23]∂∂ This substantially eclipsed the 20 percent national job growth for the same period. In contrast, in the 10-year period prior to TABOR’s enactment, the nation added 19 percent to its jobs base, while Colorado added 17.2 percent.[24]

Likewise, an analysis of U.S. Census Bureau data shows that Colorado’s population increased faster than the national average following enactment of TABOR.[25] The Washington, D.C.-based Heritage Foundation also found that measures of per-capita personal income growth and per-capita gross state product show Colorado lagging the national average in the decade prior to TABOR and then significantly outperforming the average in the decade afterward.[26] From 1993 to 2005, U.S. Census Bureau figures show that Colorado’s population increased 29 percent, double the national average.[27]

Colorado’s post-TABOR economic success had many contributing factors, and it would be inaccurate to ascribe the state’s exceptional economic success to any one of them. However, the acceleration of Colorado’s economy in the wake of implementing TABOR suggests that the resulting restraint on government taxes and spending may have contributed to Colorado’s economic and population growth.

|

∂∂ Colorado’s higher rates of job growth existed prior to the modification of TABOR in 2005. The job growth rate from June 1993 to June 2005 was 32.5 percent, which was well above the national average of 17.8 percent. |

Colorado’s Post-2001 Recession

The recession that began for the entire nation in 2001 was more severe in Colorado. As noted in a 2005 Cato Institute study, the terrorist attacks of September 11, 2001, resulted in a 14 percent decline in skiing tourism that winter.[28] The worst drought in decades occurred the following year, touching off damaging forest fires and reducing both summer tourism and agricultural production. Nearly 12 percent of the Colorado workforce relies directly upon these two industies.[29]

The Cato Institute’s study also found that this sharp economic contraction contributed to a 12 percent reduction in tax collections for 2002.[30] A smaller reduction in revenue for 2003 brought the two-year total reduction to more than 13 percent. Most states experienced revenue shortfalls because of this recession, but Colorado’s was about twice the national average.[31]

As the Washington, D.C.-based Tax Foundation has observed, the spending discipline enforced by TABOR appears to have mitigated the budgetary challenges that appeared after fiscal 2001. TABOR required a state tax rebate of about $1 billion in fiscal 2001, because revenue collection had exceeded the TABOR limit by that amount. The 2001 state budget — the last before the recession reduced state revenues — was therefore not based on spending the extra $1 billion. In 2002, when total revenues declined by more than $1 billion, the state budget faced a deficit of about $196 million — considerably less than the $1.1 billion deficit the state would have faced if the $1 billion in extra revenue in fiscal 2001 had been spent in the state budget, instead of being returned to taxpayers.[32] Thus, TABOR’s spending cap probably reduced the largest state budget deficit of Colorado’s recession by 83 percent.

Colorado’s poor job growth since the recession has led some to argue that TABOR’s economic impact has been negative.[33] One figure from the U.S. Bureau of Labor Statistics suggests that Colorado has had virtually no job growth since fiscal 2001.

This measurement is not consistent with other figures put out by the Bureau of Labor Statistics and other independent economic sources. The bureau’s monthly national unemployment statistics indicate that Colorado has added more than 137,000 jobs since 2001. This is a job growth rate of nearly 6 percent, compared to a national growth rate of less than 4 percent.[34]

In April 2005, the Federal Deposit Insurance Corporation issued a state profile that found that Colorado had the 10th fastest annual state job growth in 2004, achieving a rate 31 percent above the national average. According to the Denver Business-Journal, an FDIC spokesman commented about the findings: "Colorado has had a remarkable turnaround. I don’t think anybody expected the type of rapid acceleration that the state has had."[35]

While it will be easier to tell by next year whether Colorado’s economic and job growth are indeed above the national average, it seems unlikely that the Bureau of Labor Statistics data suggesting no growth is correct.

Amendment 23 and Referendum C: The Education Spending Mandate and the TABOR "Time-Out"

Colorado’s fiscal 2002 budget was heavily affected by Amendment 23, a constitutional spending mandate for primary and secondary education that was approved by Colorado voters in November 2000. Amendment 23 requires that state spending on local public schools through 2010 increase annually by no less than one percentage point above the rate of inflation. After 2010, the amendment requires state spending on local public schools to meet or exceed the inflation rate.¶¶

As a 2003 Colorado House report on TABOR observed, Amendment 23 was passed during a widespread assumption in 2000 that Colorado’s budget surpluses would continue.[36] From 1998 to 2001, Colorado’s economic growth had resulted in state tax revenue that annually exceeded the TABOR limit by more than $500 million, requiring tax refunds of comparable size.[37]

The budget surpluses ended shortly after voters approved the spending mandate, however. Overall state spending had to be reduced to match the lower revenue, but the state budget for primary and secondary education, representing about 24 percent of total Colorado government spending, was constitutionally required to increase above the inflation rate.[38] By 2006, according to the Cato Institute, Amendment 23 mandated that public school spending be $818 million higher than it had been in 2001, even as state tax collections remained $226 million less than they were in fiscal 2001.[39]

Colorado lawmakers achieved the education spending increases by making cuts to other state programs. In 2005, advocates of these programs persuaded Colorado voters to ratify "Referendum C," a statewide ballot proposal that allows the state to keep all of the projected revenue surpluses through 2010.

The estimated cost to taxpayers of the forgone rebates during the next five years is more than $4.88 billion, a larger sum than the total TABOR rebates to date.[40] Absent the education spending mandates in Amendment 23, taxpayers would have been much less likely to incur these costs, since the higher spending would have required voters to approve new taxes.

|

¶¶ A similar education spending mandate is contained in Michigan’s current Proposal 5, which will appear on the November 2006 statewide ballot. The Michigan proposal mandates increases only at the inflation rate, but the proposal also mandates increases in state spending on higher education. The proposal includes several other spending mandates as well (see the Mackinac Center for Public Policy’s “An Analysis of Proposal 5: The ‘K-16’ Michigan Ballot Measure,” September 2006). |

TABOR’s Effect on Government Programs

Some critics of the SOS proposal have argued that TABOR harmed Colorado government programs for health care, roads and education, and that the SOS proposal would cause similar damage in Michigan.[41] One statistic cited is that in 1992 Colorado ranked 35th as a share of personal income for primary and secondary education spending, but fell to 49th by fiscal 2001. Similar figures exist for higher education.

Lower spending figures do not necessarily mean that the quality of services is lower, however. As of July 2005, more than 1 million people had moved to Colorado since enactment of TABOR. This immigration produced a total growth in state population of 29 percent, which is double the national average over those years and significantly higher than a comparable period prior to the passage of TABOR.[42] This influx of new residents to Colorado suggests the state was a relatively attractive location. It seems unlikely that Colorado became an attractive place to live while simultaneously developing a poor education, health and road system.

The United Health Foundation, while noting that the state has comparatively low spending on public health, nonetheless ranks Colorado as the 17th healthiest state in the nation for fiscal 2005 — 9.7 percent above the national average. This is not substantially changed from 1990, three years prior to the enactment of TABOR, when Coloradans ranked 14th healthiest.[43]

The education statistics cited above involve spending as a share of personal income, a measure that is somewhat distorted by Colorado’s rapid economic growth. In the 12 years following the implementation of TABOR in 1993, per-capita personal income in Colorado increased from 17th highest in the nation to eighth highest, growing from 3 percent above the U.S. average to 10 percent above the average. The fact that education spending fell as a percentage of this rapidly rising income means only that education spending did not rise as quickly, not that this spending did not rise at all.[44]

The latest data available for per-pupil education expenditures on primary and secondary education reveals that in 2003 Colorado was the 26th highest spending state, similar to the 22nd place ranking for per-pupil spending that Colorado achieved in 1992, before TABOR was enacted. In 2003, Colorado’s primary and secondary school students scored 15th highest in the nation on the National Assessment of Education Progress tests, an apparent improvement from 1992.[45]

As noted above under The State Budget: 1995-2007, The Budget Stabilization Fund, and Spending Limits and Taxpayer Rebates, the SOS proposal would have had a significant impact on state spending from fiscal 1995 to fiscal 2001, the years in which Michigan state revenues were growing rapidly in response to a strong state and national economy. If the SOS proposal had taken effect in fiscal 1995, the state budget would have been more than $2.2 billion smaller in fiscal 2001 than it actually was.[46] In addition, because the SOS proposal would have prevented the rapid rise in state spending from fiscal 1995 to fiscal 2001, state government would have spent approximately $9.6 billion less from fiscal 1995 through the recently enacted budget for fiscal 2007.[47] An estimated $8 billion of this $9.6 billion would have been returned to taxpayers as annual income tax refunds.[48]

These state spending reductions would have meant fewer state programs and activities, a result that some would argue is necessarily a net loss to the state. Nevertheless, it is not clear that all of the $9.6 billion in spending represented necessary state services. Total tax collection for 1999 and 2000 exceeded lawmakers’ projections, and for each year, new "supplemental" appropriations bills were written to spend the unexpected surplus taxes — more than $300 million for 1999, and nearly $400 million for 2000.

A number of new spending items were created during this period. For example, lawmakers in 2000 instituted a $2,500 college scholarship for high school students who score well on the state’s education assessment test. From fiscal 2000 to fiscal 2006, more than $800 million was spent on this new program.[49]

The necessity for some of the additional state spending during this period was called into question by many of the lawmakers themselves. The majority party in the state House of Representatives convened a task force in 2000 to examine potential cases of government waste in the 1999 budgets and issued a report that classified more than $131 million worth of spending for that year as "non-essential." Much of that $131 million involved spending enabled by the unexpected surge in tax revenues that year. A few months later, state lawmakers passed more supplemental spending for 2000.[50]

The monies spent on "non-essential" services were not available to taxpayers for their own savings and investment — uses that might have been more economically productive. The SOS proposal would have required that the state return almost $8 billion of the $9.6 billion tax revenue surplus from fiscal 1995 to fiscal 2007 to income taxpayers as annual refunds.[51] While the national recession that began during 2001 would have affected Michigan regardless of how much money state government was spending, there is historical economic evidence that lower taxes aid in the creation of economic activity and jobs,[52] a result that appears to occur at least in part because government spending, which is not subject to market discipline, can be less efficient.

Hence, under the SOS proposal, the Michigan economy might have exceeded its actual historical performance following the recession. The largest tax rebates under the proposal — estimated at more than $2 billion in fiscal 2001 and more than $1.5 billion in fiscal 2002 — would have occurred on the threshold of the national recession.[53]

Based on Colorado’s experience with TABOR and on the calculations in "The State Budget: 1995-2007" above, the SOS proposal might have created more stable state budgeting and a stronger economy. The proposal’s use of inflation and population to set a cap in state spending growth also had a certain plausibility. Government programs often face rising costs due to inflation and to the desire to provide government programs to an increasing population. Using the combined increase in inflation and population to limit spending growth would seem to allow spending to adjust to basic changes in the state’s circumstances without major, fundamental increases from current state spending as a percentage of Michigan’s economy.

Critics of the cap, however, have argued that government purchasing is disproportionately concentrated on items that increase in cost faster than the goods in the Consumer Price Index that determine the official inflation rate. The items most frequently cited as creating special demands on state government are education and health care. Critics have also argued that limiting spending increases by population growth is flawed because Michigan’s aging population will lead to a disproportionate number of persons needing state services, such as health care payments.[54]

The demand for some government programs, such as health care subsidies, may indeed increase with an aging population. It is not clear, however, that the demand for other programs would also rise at a similar rate. For instance, the demand for such programs as primary and secondary schools, higher education and corrections might rise more slowly or even decrease, given that the demand for these programs is often related to the presence of younger people. These three programs together constitute more than half of state spending from state resources.

Government is not alone in paying the rapidly rising cost of health care and medical services. Businesses and other taxpayers bear these costs as well. Additionally, consumers spend more than twice as much of their average budget on transportation costs as government does, and these costs have been exceeding the rate of inflation as fuel prices have soared.[55] Providing a cap on the growth of state spending would likely leave individuals with more resources to cope with such costs.

Public primary, secondary and higher education constitutes about 54 percent of state government spending from state resources, and costs in this area have increased more than twice the rate of inflation.[56] However, much of the rising cost of public education appears to be the result of its being a government enterprise.

The presence of a tax base means that government spending is often less responsive to market signals. For example, one source of rising public education costs in Michigan is the retirement plan for Michigan public school teachers. According to the Michigan Senate Fiscal Agency, the cost of this benefit now consumes a significant share of all new state spending on primary and secondary education.[57] The retirement plan pays benefits that the vast majority of Michigan’s private-sector employers do not offer.[58] In addition, many Michigan public school districts are reluctant to privatize their noninstructional services, despite evidence that privatization could lower costs without harming service quality.[59]

The objection to the SOS cap on grounds that education costs rise faster than the inflation rate seems unpersuasive. The fact that government spending on a government enterprise is rising quickly compared to private-sector spending could easily be a better argument in favor of the state spending cap than against it.

The SOS proposal’s prohibition on state-funded lawmaker pensions would have reduced state legislators’ overall compensation. It does not appear that this reduction would have put the pay of legislators in Michigan below that of legislators in other states.

Michigan is one of a dozen or so states with a full-time legislature.*** Michigan’s lawmakers presently receive more than $79,000 per year in base salary, and they are permitted an expense account for $12,000 more.††† They are the second-highest compensated state lawmakers in America.

Most states have a part-time legislature and pay lawmakers considerably less than Michigan does. About half of all states pay a base annual salary of less than $20,000. Texas, the second largest state for both geography and population, meets every other year for five months and pays lawmakers an annual salary of $7200. New Mexico lawmakers receive only expenses while in session, and New Hampshire lawmakers receive nothing more than a flat $200 fee for two years of service.[60]

|

*** An exact count of the number of full- and part-time legislatures depends on how these terms are defined. ††† Those who serve in leadership positions, such as the Speaker of the House and the Senate Majority Leader, may receive up to $27,000 in additional compensation. |

Prior to the SOS proposal’s dismissal from the November 2006 ballot, critics of the SOS proposal had suggested that the proposal’s language was unclear. The Michigan Chamber of Commerce asserted that the SOS proposal "is ambiguous, would introduce unfamiliar terms into the state constitution, and lacks clarity." The chamber concluded that the proposal "would result in years and years of costly litigation."[61] The Defend Michigan Coalition, a group formed to oppose the SOS proposal, has suggested that the SOS amendment would force every license or fee increase to go to a countywide vote.[62]

If the proposal did produce litigation, as seems likely, the result would be in keeping with most major constitutional reforms. The Headlee amendment produced substantial litigation involving disputes over definitions and language. As discussed earlier, the ultimate decision by the Michigan Supreme Court to define a "mandatory user fee" as a tax requiring voter approval was decided in 1998, 20 years after the amendment’s ratification. The "Durant" lawsuits over application of the Headlee amendment’s unfunded-mandate clause took roughly as long.

Indeed, for the first six years after passage of the Headlee amendment, Michigan government failed to make an official calculation of the Headlee revenue limit. This was remedied in 1986, after an estimate of the prior year accounts seemed to indicate that the revenue limit had been exceeded for the first time. While it was ultimately determined that the limit had not been exceeded, a formal system for calculating and reporting compliance with the limit was finally created by the Legislature only after this event.

The assertion that such items as dog licenses would have required a vote of the entire electorate seems less likely to have prompted serious dispute. For instance, the director of the Michigan Senate Fiscal Agency specifically singled out dog licenses as a user fee that would not require voter approval before the fee could be increased.[63]

The major findings of this study appear in the "Executive Summary." They suggest several conclusions.

First, the SOS proposal would have had its most significant impact on Michigan through its state spending cap. As noted in this study, the proposal’s local tax issues would have been resolved over time through the courts and would have represented a change in the degree, not the nature of, the local taxpayer provisions under the Headlee amendment. And while ending publicly funded pensions for new Michigan lawmakers would indeed have affected the state budget, that budget impact is small in comparison to the impact of the state spending cap over the long term.

The evidence suggests that the SOS proposal would have significantly restrained state government spending growth while allowing annual spending increases: State spending from state resources would have been reduced by an estimated $9.6 billion in total between fiscal 1995 and fiscal 2007. This extra money would have generated a fiscal 2005 state budget stabilization fund estimated at $2.5 billion, compared to the effectively empty stabilization fund that actually existed in 2005. This $2.5 billion would have been available to insulate the state budget from future revenue declines resulting from a depressed state economy.

Currently, the Headlee amendment to the state constitution implicitly caps Michigan government spending. In fiscal 2000, state spending exceeded the Headlee limit by $159.7 million. At least since 1995, however, Michigan government spending has been restrained in practical terms only by the relative strength of the Michigan economy.

During years when a strong economy has produced increased tax revenue, Michigan lawmakers and governors have spent much of the additional revenue, often by creating new government programs. Lawmakers themselves later classified some of this additional spending as "non-essential." Only in periods of recession has state spending abated, largely due to the decline in available tax revenue.

The SOS spending limit would have produced annual state spending in fiscal 2007 that is almost identical to the current state budget. This similarity suggests that Michigan government could have financed programs within the boundaries of the SOS spending cap.

An estimated $8 billion would have been rebated to Michigan taxpayers between 1995 and 2007 under the SOS proposal. It is possible that this de facto tax cut could have improved Michigan’s economic performance. The largest tax rebates would have occurred on the threshold of the current recession.

These rebates would have resulted in less state government spending, but Colorado’s experience with a state spending cap based on population and inflation suggests that lower levels of government spending do not necessarily lead to a decline in quality of life.

(New Language underlined — Deleted language struck)

A Proposal to Amend the Constitution of the State of Michigan by amending Article 9, Section 24; Article 9, Section 26; Article 9, Section 27; Article 9, Section 28; Article 9, Section 31; Article 9, Section 32; and Article 9, Section 33; as follows:

Article 9, Sec. 24.

Members of the legislature of the state of michigan shall not earn or accrue any financial benefits of a state funded pension plan, deferred compensation plan, retirement savings plan, retirement system of the state, or a matching state contribution, as a result of their legislative service for terms commencing after January 31, fiscal 2007. This shall not be construed to affect salaries or expenses, to prevent a person from voluntarily allocating a defined contribution from his or her salary to a retirement savings plan, or to reduce or eliminate any benefits vested prior to the effective date of this amendment. The accrued financial benefits of each pension plan and retirement system of the state and its political subdivisions shall be a contractual obligation thereof which shall not be diminished or impaired thereby. Financial benefits arising on account of service rendered in each fiscal year shall be funded during that year and such funding shall not be used for financing unfunded accrued liabilities.

Article 9, Sec. 26.

A) There is hereby established a limit on the total amount of taxes which may be imposed by the legislature in any fiscal year on the taxpayers of this state. This limit shall not be changed without approval of the majority of the qualified electors voting thereon, as provided for in Article 12 of the Constitution. Effective with fiscal year 1979-1980, and for each fiscal year thereafter, the legislature shall not impose taxes of any kind which, together with all other revenues of the state, federal aid excluded, exceed the revenue limit established in this section. The revenue limit shall be equal to the product of the ratio of Total State Revenues in fiscal year 1978-79 divided by the Personal Income of Michigan in calendar year 1977 multiplied by the Personal Income of Michigan in either the prior calendar year or the average of Personal Income of Michigan in the previous three calendar years, whichever is greater.

B) For any fiscal year commencing after December 23, fiscal

2006, in the event that Total State Revenues exceed the revenue

STATE SPENDING limit established in this Section 28 by

1% or more, the excess revenues shall be deemed a surplus. the surplus,

or at least 50% thereof, shall be promptly refunded, by individual check for

amounts exceeding $25 over existing tax liabilities (adjusted for inflation

after fiscal 2007), or credited against tax liabilities for lesser amounts, to

taxpayers pro rata based on the liability reported on the Michigan income tax

and single business tax (or its successor tax or taxes) annual

returns filed following the close of such fiscal year after a portion is first

transferred If the excess is less than 1%, this excess may be

transferred to the State budget stabilization fund. The portion of

surplus transferred to the state budget stabilization fund shall be equal to the

lesser of (1) an amount necessary to ensure that the balance in the budget

stabilization reserve fund attributable to surplus funds or interest thereon at

the end of the state fiscal year is an amount equal to 10% of the state spending

limit for that fiscal year, or (2) an amount equal to 50% of the surplus.

C) for any state fiscal year that commences after December 23, fiscal 2006, if total state revenues are less than the amount of the state spending limit, the state treasurer shall transfer money from the state budget stabilization fund to the general fund from available funds in the minimum amount necessary to offset a shortfall of total state revenues below the state spending limit, under no other circumstances shall the state treasurer transfer moneys from the fund.

D) The revenue limitation established in this section shall not apply to: 1) taxes imposed for the payment of principal and interest on bonds, approved by the voters and authorized under Section 15 of this Article prior to November 7, fiscal 2006, or any subsequently authorized bonds which are amortized for at least 20 years and dedicated specifically for the acquisition of, or construction upon, real property, and 2) loans to school districts authorized under Section 16 of this Article.

E) If responsibility for funding a program or programs is transferred from one level of government to another, as a consequence of constitutional amendment, the state revenue and spending limits may be adjusted to accommodate such change, provided that the total revenue authorized for collection by both state and local governments does not exceed that amount which would have been authorized without such change.

Article 9, Sec. 27.

A) The state spending limit of section 28 and the revenue limit of Section 26 of this Article may only be exceeded in an emergency, as defined herein, or by a voter-approved suspension.

B) Emergency spending may occur only if all of the following conditions are met: (1) The governor determines that an imminent threat to public health or safety exists and requests the legislature to declare an emergency; (2) the request is specific as to the nature of the emergency, the dollar amount of the emergency, and the method by which the emergency will be funded; and (3) the legislature thereafter declares an emergency in accordance with the specific terms of the governor’s request by a two-thirds vote of the members elected to and serving in each house. The emergency must be declared in accordance with this section prior to incurring any of the expenses which constitute the emergency request.

C) A voter-approved suspension of the state spending limit and the revenue limit may occur only if all the following conditions are met: (1) two-thirds of the members of each house vote to refer a suspension of the limits, up to a predetermined maximum, to the voters; (2) a ballot advisory in bold capital letters directly above the ballot title instructs voters: ‘a "yes" vote on this measure will authorize the state to retain extra taxes and spend them in excess of constitutional limits by [insert amount of predetermined maximum additional spending.]’; And (3) the suspension is approved by a majority of eligible voters participating in a statewide general election.

D) The state spending limit or the revenue limit may be exceeded only during the fiscal year for which the emergency is declared or suspension is approved. In no event shall any part of the amount representing a refund under Section 26 of this Article be the subject of an emergency request.

Article 9, Sec. 28.

A) No expenses of state government shall be incurred in any fiscal year which exceed the sum of the revenue limit established in Sections 26(A) and 27 of this Article plus federal aid and any surplus from a previous fiscal year.

B) Recognizing that subsection (a) defines a limit on expenses, this subsection (b) establishes a "state spending limit" for any state fiscal year that commences after december 23, fiscal 2006, unless subsection (a) would require less spending, as follows: (1) the total amount of state fiscal year spending in the preceding fiscal year increased by a percentage amount equal to the result obtained by adding any positive increase in the rate of inflation for the calendar year ending during the preceding state fiscal year, plus any positive percentage change in state population during the calendar year ending during the preceding state fiscal year, or, (2) the state spending limit for the previous fiscal year; whichever amount is greater.

Article 9, Sec. 31.

Units of Local Government are hereby prohibited from levying

or charging any new local tax, excise, special assessment, or mandatory user fee

not authorized by law or charter when this section is ratified and already being

lawfully levied or charged on november 7, fiscal 2006, or from increasing the

rate of an existing tax or amount of a mandatory user fee above that rate or

amount authorized by law or charter when this section is ratified and already

being lawfully levied or charged on november 7, fiscal 2006 without the approval

of a majority of the qualified electors of that unit of Local Government voting

thereon. If the definition of the base of an existing local tax or mandatory

user fee is broadened, the maximum authorized rate or amount of taxation

on the new base in each unit of Local Government shall be reduced to yield the

same estimated gross revenue as on the prior base. If the assessed valuation of

property as finally equalized, excluding the value of new construction and

improvements, increases by a larger percentage than the increase in the General

Price Level from the previous year, the maximum authorized rate applied thereto

in each unit of Local Government shall be reduced to yield the same gross

revenue from existing property, adjusted for changes in the General Price Level,

as could have been collected at the existing authorized rate on the prior

assessed value. No unit of local government may request approval from the voters

for any tax that, together with all other taxes then authorized, would exceed

the maximum tax that may be imposed under state law, charter, or this

constitution if such a tax were levied at the beginning of the next fiscal or

calendar year, whichever is sooner. The limitations of this section shall not

apply to taxes imposed for the payment of principal and interest on bonds or

other evidence of indebtedness or for the payment of assessments on contract

obligations in anticipation of which bonds are issued which were authorized

prior to the effective date of this amendment.

Article 9, Sec. 32.

Any taxpayer of the state shall have standing to bring suit within 3 years of the accrual of the cause of action in the Michigan State Court of Appeals to enforce the provisions of Section 6, Section 24, and Sections 25 through 34, inclusive, of this Article, by means of injunctive, monetary, and/or other relief and, if the suit is sustained, shall receive from the applicable unit of government his costs and expenses incurred in maintaining such suit, including actual reasonable attorney fees. no costs or attorney fees shall be ordered against such plaintiffs unless the action is determined frivolous under Michigan law.

Article 9, Sec. 33.

Definitions. The definitions of this section shall apply to Section 6, and Sections 25 through 34 of Article IX, inclusive.

A) "Total State Revenues" means all moneys or credits

received by the state from any source now in existence, or created or identified

in the future, including bonds, fees, and tobacco settlement proceeds, except

the following: 1) moneys received from the federal government; 2) moneys

received as gifts which must be expended for purposes specified by the donor; 3)

moneys which are income earned on moneys in permanent endowment funds, trust

funds, pension funds, disability funds, unemployment funds and deferred

compensation funds, and which are credited to such funds; 4) the proceeds of

bonds contracted specifically for the acquisition of tangible assets or the

construction of public projects which are amortized over a period of more

than/at least 20 years; 5) moneys transferred from the budget stabilization

fund; 6) the amount of any credits based on actual tax liabilities or the

imputed tax components of any rental payments, carry-over funds from prior years

and non-refundable property tax credits; and 7) proceeds from the sale of

government assets to non-government entities at real market value to the extent

the proceeds are dedicated as surpluses to taxpayer refunds, or to the budget

stabilization fund, according to section 26 of this article. This definition

shall not be construed to alter or change the base year ratio as previously

established in section 26 of this article, which is 9.49% of personal income in

the state of michigan. includes all general and special revenues,

excluding federal aid, as defined in the budget message of the governor for

fiscal year 1978-1979. Total State Revenues shall exclude the amount of any

credits based on actual tax liabilities or the imputed tax components of rental

payments, but shall include the amount of any credits not related to actual tax

liabilities.