This manual provides answers to the costly woes of transportation. When transit bus service, for instance, is competitively contracted out to private firms, savings range from 30 percent to 60 percent with no reduction in safety or service quality. 20 pages.

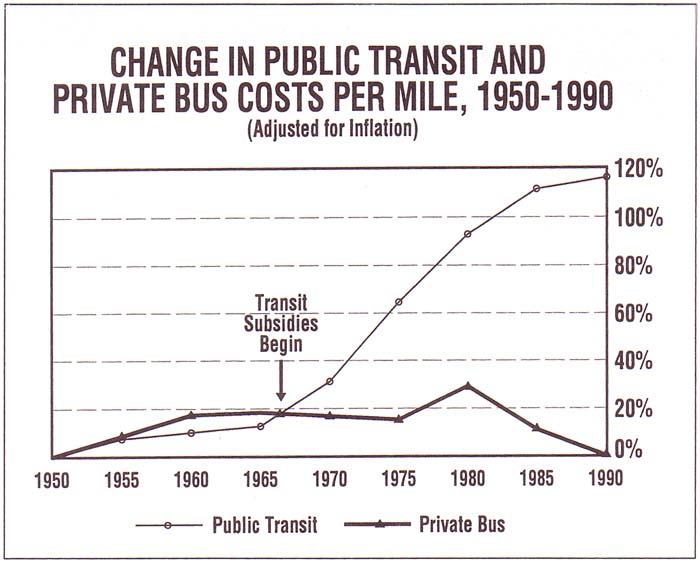

In the United States, transit operating costs per vehicle mile increased 418 percent from 1970 to 1990-twice the rate of inflation and two-and-a-half times the cost of similar service in the private bus industry. Two-thirds of transit costs are paid by federal, state, and, predominantly, local subsidies. The majority of the public funding has supported low and declining transit productivity and high transit wages and benefits. Transit's problem is not funding.

Nearly ten percent of regular transit bus service is competitively contracted in the United States. Savings range from 30 percent to 60 percent, and independent studies report that the safety, quality, and reliability of competitively contracted service equals or exceeds that of the public sector. Political, bureaucratic, and perceptual barriers have prevented competitive contracting of transit in many areas. And competitive contracting is slowed by legal barriers such as Section 13(c) of the federal transit act.

Under competitive contracting, the public authority retains the service franchise (ownership) and controls the service. The public authority specifies route alignments, service frequencies, fares, schedules, and any other requirements deemed to be in the public interest. Private transportation companies respond to requests for proposals from public authorities to provide specific services for a limited period of time (typically no more than five years). Winning cost proposals, final contracts, and requests for proposals are available to the public. In some cases, the public authority leases the vehicles (buses, etc.) to the successful contractor; in other cases the contractors supply their own vehicles.

The success of competitive contracting depends on three fundamental principles: public control, competition, and open access and process. First, the public authority has a responsibility to the riders and taxpayers to ensure that public services meet quantity and quality standards that are set by government. Second, contracting programs must foster the development and maintenance of a truly competitive market so that costs are kept under control. Third, these two principles are best served when all interested parties are allowed to participate and have access to records.

Public-transit service in the United States once was provided by unsubsidized private companies under public franchise. But, for more than two-and-a-half decades, most urban public-transit services have been provided by public authorities and supported by public subsidies.[1] Much of the public aid has been consumed by costs that have escalated well ahead of the inflation rate. Public transit provides mobility for an ever-smaller minority of the general population, while increasing public transit unit costs have resulted in increasingly higher fares and federal, state, and, predominantly, local subsidies (see Figure 1).

Transit operating costs per vehicle mile increased 418 percent from 1970 to 1990—twice the rate of inflation and two-and-a-half times the cost of similar service in the private bus industry.[2]

Since the public sector began to produce transit service, transit cost increases have outstripped every element of the consumer price index, including fuel and medical care costs.

Nationwide, fares cover about one-third of transit's operating costs and none of transit's capital costs. Since 1956, transit has consumed nearly $200 billion in federal, state, and local subsidies.[3] Fares, which lagged behind inflation during the 1970s and 1980s, are high and rising in large metropolitan areas, further eroding transit's small market share. Yet, many transit agencies face or will face budget shortfalls despite proposed increases in federal transit subsidies.[4] These growing deficits will increase the pressure for more state and local aid to transit.

Transit's problem is not lack of funding; increased subsidies have contributed

to rising transit costs.[5] Three-quarters of all new inflation-adjusted monies received by transit has been used to fund costs that have exceeded inflation.[6] Most of the subsidies have been consumed by declining worker productivity[7] and wages and benefits that are two or more times those of similar private-sector workers.[8]

While public-transit costs outpaced inflation over the past two decades, private bus industry costs per mile declined relative to inflation. From 1970 to 1985, real private-sector costs per mile declined 8.3 percent[9] compared to the 64 percent real increase in public transit. If public-transit costs had risen at the rate of increase in the private bus industry, service levels now could be more than double the 1989 level.[10]

The private bus industry operates more than 120,000 vehicles (four times the number of active public transit vehicles) and includes more than 3,000 firms, ranging from small local operations to large national companies[11] (see Table 1). In addition to charter, tour, shuttle, and intercity service, the private bus industry provides under contract to transit agencies and school districts one-third of the nation's school bus services, more than 60 percent of dial-a-ride service for the elderly and handicapped, and 10 percent of regular transit route services.[12]

Table 1

|

COMPETITIVE CONTRACTING OF TRANSIT SERVICE IN LARGE U.S. METROPOLITAN AREAS |

|

|

Competitively Contracted* |

1992 |

|

20% or more |

Austin |

| Dallas-Ft. Worth | |

| Denver-Boulder | |

| Las Vegas | |

| San Diego Atlanta Area | |

|

15% to 19% |

Houston-Galveston-Brazoria |

| Minneapolis-St. Paul | |

|

10% to 14% |

Atlanta Area |

| Los Angeles-Anaheim-Riverside | |

| Kansas City Area | |

| San Francisco-Oakland-San Jose | |

|

5% to 9% |

Baltimore |

| Chicago-Gary-Lake County | |

| Miami-Ft. Lauderdale | |

| Phoenix | |

| Sacramento/Seattle-Tacoma Area | |

| Washington Area | |

*Does not include demand-response services for the elderly and handicapped, management services, maintenance-only services, or non-competitive contracting.

As a result of high and rising transit costs, many transit agencies in the United States and throughout the developed world have sought alternatives from the competitive market: sale of assets, deregulation (load shedding), and competitive contracting[13]

A. Sale of Assets

The sale of assets and operations to the private sector is appropriate for profitable public services. Public transit, however, is generally unprofitable in the United States and Western Europe. U.S. demand for transit—transit market share—is low and continues to decline. Less than 2 percent of all personal trips in 1990 were made by public transit, most during morning and afternoon rush hours.[14] For most transit routes in the largest cities, ridership is so low that even cost-efficient transit operators could not collect sufficient fare revenue to cover capital and operating costs. In addition, transit is overcapitalized. Public transit facilities tend to be larger than private facilities, and they tend to be in high-cost locations. Lacking competitive incentives for efficiency, public transit probably owns more vehicles than would be needed to produce the same service by the private sector. Assets could be sold to commercial transportation operators only at a loss.

B. Deregulation (Load Shedding)

In most metropolitan areas, the public transit agency is the only legal provider of public-transit services. Private entrepreneurs may be arrested, fined, and their vehicles impounded for offering non-subsidized transit services to the public. Transit can be provided by the private sector without subsidy in some areas and for some routes as it is in areas of New York and Miami.[15] Deregulation could save public money; it could result in innovative and responsive van and bus service, particularly in low-income minority neighborhoods; and, because of low barriers to entry and almost universal driving skills, it could foster the development of entrepreneurial activity, particularly for minorities, as it has in South Africa. State and local ordinances that give the transit agency the exclusive right to operate or regulate transit services could be modified to permit free entry (subject to minimal regulatory requirements for safety, insurance, proper licensing, and coordination) of commercial transit services.

C. Competitive Contracting

Competitive contracting is the most viable private-sector solution to high and rising public-transit costs in low-demand markets such as United States cities and where full public control of transit is desired. Competitive contracting is used by a small but increasing number of U.S. public-transit agencies to provide cost-effective, safe, reliable transit services.

A. Direct Savings

Competitively contracted public-transit services have achieved average direct cost savings of more than 30 percent.[16] For example, the first competitively contracted services mandated by state law have resulted in cost savings of more than 31 percent for Denver,[17] in Snohomish County, Washington, a suburb of Seattle, contracted express service saves more than 30 percent; St. Louis saved more than 50 percent on competitively contracted routes;[18] and in Los Angeles, two large contracts resulted in average cost savings of 60 percent.[19]

B. Ripple Savings

A competitive environment also improves public cost performance for services that are not yet contracted. This is referred to as the "ripple" effect. Lower public cost increases have occurred in transit agencies such as San Diego, Norfolk, and London upon introduction of competition. In San Diego before competitive contracting, transit costs increased at a rate similar to that of other transit agencies. From 1979 to 1990 (after conversion to a competitive contracting program), San Diego costs per mile increased at a rate half that of the transit industry, generally.[20]

C. Service Quality

Public administrators of competitively contracted transit services have rated the quality and performance of contracted services as equal to or better than in-house public service provision.[21] Where there have been third-party evaluations of service quality, auditors have found that the safety, reliability, and quality of contracted service is equal or superior to in-house agency provision.[22]

A number of barriers impede competitive contracting of transit services: These include legal, bureaucratic, political, and perceptual barriers. Legal barriers can be surmounted by passage of well-designed competitive-contracting legislation and the amendment of existing laws.[23]

A. Legal Barriers

Local labor contracts may explicitly prohibit or restrict contracting, or they may constrain contracting through "exclusive rights to provide service" clauses. Moreover, where contracts are silent on the issue, arbitrators may construe competitive contracting to be prohibited. Prohibitions and restrictions to contracting can be eliminated by passing "public prerogative" legislation (separately or as part of a competitive contracting bill), which forbids restrictions on competitive contracting and specifies that the right of the citizenry to obtain public services for no more than the market rate cannot be a subject of labor bargaining.[24]

Public transit agencies also frequently cite as a barrier the labor-protective provisions of the federal Urban Mass Transportation Act of 1964, and as amended. One provision of Section 13(c) requires that an employee whose job is eliminated due to economies or efficiencies be provided up to six years' severance pay. While Section 13(c) can cause difficulties, it does not create a barrier where local labor contracts or state laws permit competitive contracting. Section 13(c) generally has not been a barrier even where labor contracts do not authorize competitive contracting if:

Contracting has been implemented within the employee turnover rate so that no employees are laid-off; or

As in Denver, transit employees were paid although idle. (The Denver transit agency still saved through competitive contracting.)

B. Political Barriers

Transit management and organized labor have opposed competitive contracting programs even where present employees were protected, and they have opposed commercial operation even when these operations do not infringe upon public transit routes and services. These groups have fostered political opposition to competitive contracting and commercial operation. Political opposition declines, however, in response to other circumstances such as when:

Local governments are unable or unwilling to fund large and rising transit deficits;

Transit funding is insufficient to cover the increase in operating costs, and riders are confronted with cuts in service, higher fares, or both; or

The public becomes aware of the high cost of public transit. Local political opposition can be surmounted when states legislate competitive contracting or deregulation of public transit.

C. Bureaucratic Barriers

While not always the case, many public transit agencies often have not fairly evaluated, awarded, and administered the competitive-contracting process when the agency itself also is a proposer (bidder). In most foreign nations that convert to competitive contracting and in states with a high percentage of contracting, such as California, governments create separate bodies to determine transit policy. This separation of policy from operations helps to ensure that the policy agency is unencumbered by self-interested operating concerns and is focused upon obtaining the most (safe, quality) service for the public money expended.

D. Perceived Barriers to Competitive Contracting

In addition to political and legal barriers to competitive contracting, perceived barriers, usually in the form of arguments advanced to impede conversion to competitive contracting, restrict contracting opportunities.[25] Perceived barriers include the widely held belief that the public sector provides cheaper service, because it is not required to pay taxes or earn a profit; the fear that competitive contracting will result in chaotic service; or the belief that public employees provide better service than private employees because they are more committed to the public good. None of these contentions is systematically supported by experience, but they command media attention, and they are advanced by opponents to competitive contracting and commercial services. A simple examination of competitive contracting and commercial experience in the United States and abroad can overcome these barriers.

Under competitive contracting, the public authority retains the service franchise (ownership) and controls the service. The public authority specifies route alignments, service frequencies, fares, schedules, and any other requirements deemed to be in the public interest. Private transportation companies respond to requests for proposals from public authorities to provide specific services for a limited period of time (usually no more than five years). The public authority awards a contract to the lowest responsive and responsible proposer. Winning cost proposals, final contracts, and requests for proposals are available to the public. In some cases, the public authority leases the vehicles (buses, etc.) to the successful contractor; in other cases the contractors supply their own vehicles.

Under a properly designed contract, the private contractor has incentives to perform effectively. The profit motive provides firms with an incentive to reduce costs within the constraints of the contract. Additionally, the contract may be canceled for unsatisfactory performance; indeed, many contracts provide for penalties for unsatisfactory performance. Finally, the private company will be interested in being favorably considered when the contract is re-contracted at expiration or when another service package is to be contracted.

Administered properly, competitive contracting results in the lowest costs. Where private costs are less than public costs, the service is operated privately. Where public costs are less than private costs, the service is operated by a public authority under the same terms and conditions as would have been imposed upon a private company. In either case, the service is operated the least expensively. Competitive contracting in the public sector is analogous to "make or buy" analysis in the private sector.

A. Preparation

Public authorities should consult with private transportation providers before designing and issuing requests for proposals. This consultation may be through informal meetings, hearings, or through formal committees of private providers under the sponsorship of public authorities. Advance consultation permits the public authority to consider alternatives for service and contract design that take full advantage of private-sector capabilities, consistent with public requirements.

B. Request for Proposal Information

Requests for proposals should contain a complete description of the service to be purchased, including schedules, service miles, service hours and any applicable service or safety standards. Further, requests for proposals should contain a clear description of the required proposal format. In New Orleans and Denver, public-transit authorities have provided detailed questionnaires and cost forms, which, once completed, are the private company's proposal. This approach reduces uncertainty about what is required in the private company's proposal and greatly simplifies the preparation of proposals. Simplification increases the number of companies likely to respond, especially smaller companies, which tend toward lean management. Requests for proposals should, at a minimum, contain detailed cost proposal forms to be completed and submitted as a part of the proposal.

C. Length Of Procurement Process

The time span between issuance of the request for proposals and submission of proposals may be the single greatest deterrent to the number of competitors. There should be sufficient time for all potential proposers to solicit and receive copies of the request for proposals, to attend any pre-proposal conferences, and to prepare their proposal. In general, the amount of time allotted should increase with the size of the service to be proposed and to the extent that the contractor would have to provide facilities, capital equipment, and vehicles. Normally, except for very small and emergency contracts, two months is sufficient time for private companies to respond to requests for proposals. For large contracts of 100 vehicles or more, agencies should allow three or more months for response.

The amount of time allowed between the award of the contract and service provision is usually specified in the request for proposals and the ensuing contract. Insufficient lead time will deter competent service providers from proposing. For small contracts and when the authorities supply the vehicles, two to three months is sufficient lead time. When contracts are large or require a company to supply vehicles or specialized equipment or facilities, six to nine months of lead time may be needed. Public authorities also should allow themselves adequate time for a thorough evaluation of the proposals received.

D. Proposal Evaluation Most public authorities divide the evaluation process into two parts:

Evaluation of service qualifications and specifications; and

Determination of the most cost-effective proposal.

A company's price proposal is not considered if it does not meet the service qualifications and specifications. Some public authorities require separate sealed envelopes—one with the service proposal and qualifications and the other with the price. The price envelope is opened only for companies that have qualified in the first step. This approach is useful in building the confidence of private providers in the procurement process and minimizes the potential for challenges by unqualified companies.

E. Fair Cost Comparison

Public transit authorities often compare in-house operating costs with proposed competitive costs before determining whether to award a contract to a private proposer. Private providers have alleged that public-transit authorities have not fairly evaluated private proposals relative to in-house costs. Some public transit authorities have determined their in-house costs only after reviewing the competitive proposals. In other cases, public authorities have understated in-house costs.[26] As a result, a general mistrust has arisen in cases where public authorities administer competitive contracting processes in which they are also competitors.

Two adverse effects result when a publicly funded agency wins a contract as a result of understating its costs:

Overall competition for public contracts tends to decline resulting in long-term cost increases. The private sector is not inclined to respond to requests for proposals where the process is perceived as unfair.

Total public costs increase or services decrease because the winning proposer must subsidize the transit service it won with public monies that were earmarked for another purpose. The publicly funded agency must cut a service for which it was funded or must request additional funding or increased fares or user fees to cover the costs of the transit service. Public-transit authority contract administrators have required detailed accounting from publicly funded proposers to eliminate this cross subsidization. The Federal Transit Administration requires that public transit authorities must propose no less than fully allocated capital and operating costs when responding to requests for proposals.[27]

Three public transit authorities that have taken special steps to assure objectivity offer potential models. In Cincinnati, the Southwest Ohio Regional Transit Authority (SORTA) hired an accounting firm to prepare its internal proposal and submitted its sealed proposal by the deadline required of the private providers. Personnel assisting in the development of the internal proposal were not permitted to participate in the evaluation of proposals. The Bi-State Development Authority of St. Louis separated the internal preparation of a proposal from the evaluation process. Bi-State did not permit personnel who prepared the internal proposal to participate in the evaluation of proposals. The Suburban Mobility Authority for Regional Transportation (SMART) in suburban Detroit followed procedures similar to SORTA and Bi-State, but SMART also publicly announced the agency bid price prior to opening private bids at the proposal deadline to alleviate any doubt about agency price manipulation.

To obtain the maximum level of competition and, therefore, the lowest price, public authorities must encourage the confidence of the private sector in the fairness of the procurement process. This is best accomplished by requiring that public authorities be subject to the same rules as private companies and that public authorities propose their true costs when competing for contracts.

F. Pre-proposal Conference

Many public authorities hold one or more pre-proposal conferences with potential proposers after issuance of the request for proposals. Pre-proposal conferences often result in changes in the proposal package as the public authority makes corrections in the original specifications or, as a result of questions from the potential contractors, becomes aware of alternative ways to deliver the service. Pre-proposal conferences can assist both the public authority and the private providers by improving the understanding of the service required, and this results in lower costs and more responsive private proposals.

G. Fixed-price Contracts

Most public transit authorities in the United States require that proposers submit a final price that is largely unalterable throughout the term of the contract. This is called a fixed-price contract. Most contracts contain a provision that allows for minor changes in the amount of service. Typically, service levels may be increased or decreased by a certain percentage (usually plus or minus 5 percent), and many contracts allow for modifications to the route structure if both parties agree.

The extensive use of fixed-price contracts has been instrumental in maintaining the cost effectiveness of competitive contracting. The most important characteristic of fixed-price contracts is that contract rates (prices) cannot be non-competitively manipulated. Fixed-price contracts involve the proposal of a certain price for a given amount of service over a specific contract length, usually expressed in cost per unit of service, such as service miles or service hours.

From the public perspective, the optimum level of competition and, thus, the lowest costs are likely to be achieved through "pure" fixed-price contracts. Proposers are required to quote fixed prices for basic contract terms, for all option periods, and for downward or upward adjustments in service level. There is no price negotiation after execution of the contract and, therefore, no provision for adjustment of unit prices.

Fixed-price contracts may, however, include forms of indexation that permit contract price adjustments based upon the change in generally accepted indices such as measures of inflation, fuel costs, or transportation industry costs. Indexing can reduce the risk for private contractors as they attempt to predict future costs. Potential contractors propose basic unit prices, but the unit prices are increased or decreased periodically according to specified indices. The price variation may be a percentage of the index's change or may be invoked only when a certain level is reached such as a 10 percent increase or decline from a base level. As in pure fixed-price contracts, indexed fixed-price contracts do not provide for price negotiation after execution of the contract—remuneration can be altered only in response to changes in the appropriate indices.

Contract-price indexing can increase public costs, since U.S. private-sector costs historically have increased at rates slower than inflation and substantially slower than transportation industry indices. But indexing can provide a simple tool for dealing with major variations in cost that are outside the control of the contractors, especially fuel costs.

There is a simpler, more cost-effective way to deal with extraordinary and universal escalation of some costs like fuel. Some contracts have reduced private risk by negotiation or "pass through" of these costs. In "pass-through" arrangements, bidders do not include the price of fuel in their cost estimations or they are given a constant price (one dollar per gallon) for estimation purposes. Reimbursement for the winning bidder is based on the current market price of the cost component. Negotiation is less formal; the winning bidder may request that the authority adjust the contract price to reflect the increase in the designated cost component, usually fuel. These methods avoid contract-price indexing, which can unduly increase public costs. Limited negotiation and "pass-through" options reduce the risk of the private operator, thus potentially reducing contract prices.

H. Renewal Options Contract duration can be defined in two ways by public authorities.

Some public authorities offer contracts that have a specified ten-n, such as three years, while other public authorities may award contracts for a basic term plus renewal "options." For example, a public authority may award a three-year contract with a two-year renewal option for a total contract term of five years. At the end of three years, the public authority may decide to exercise the two-year option and have the incumbent company continue to provide the service. On the other hand, the public authority may decide to competitively procure the service again at the end of three years. The use of options can increase the incentives to the contractor to provide quality service and can give the public authority a way to change contractors without invoking termination.

I. Contract Duration

Costs are likely to be higher for shorter contract durations because the risks will be greater, since proposers must recover fixed costs over a shorter period of time. Further, "start-up" costs are incurred when a new private provider assumes a service. Costs will also tend to be higher because the number of proposers will decline as the risk increases. Contract duration can be shorter in cases where the public authority provides vehicles for the private contractor. Some contracts have been for only one year, while most have been at least two years. Where the contractor supplies the vehicles, contracts should be at least three years.

Alternatively, contract periods can be too long. Longer contracts require greater risks for both parties, since it is extremely difficult to project costs. Generally, contracts, including options, do not extend to beyond five years. The primary reason is that, as contract lengths extend beyond five years, it is necessary to rely more on negotiated price increases and adjustments, which, in the absence of competition, are likely to result in higher public costs.

Finally, it is important to observe the same contract duration whether the contract is awarded to a public authority or a private company. Failure to competitively re-procure a contract represents an abandonment of competitive incentives and likely will result in higher public costs.

J. Contract Size

Many transit authorities believe it more convenient to deal with a few large contracts. The transit industry is characterized by diseconomies of scale,[28] so a preference for large contracts merely limits competition and raises public, costs. There are a large number of small private providers in the United States, and they increase industry competition and help keep private transit prices low. The smaller the proposal package, the more likely that smaller companies will be among the proposers.[29]

K. Market-Share Limitation

Many public transit authorities and two pieces of competitive contracting Legislation[30] limit the total percentage of transit service that can be awarded to any one contractor. These market-share limitations restrict the ability of a single company to gain market power and limit competition. Colorado Senate Bill 164 limits individual contractors to no more than 50 percent of competitively procured service, while model state legislation by the American Legislative Exchange Council imposes a 25 percent limitation where more than 60 vehicles of service are operated competitively under the sponsorship of the public authority.

L. Rotation of Procurements

When public authorities have more than one contract, they should rotate the procurement and expiration dates. Rotating the procurement dates reduce the incentive for an incumbent company to seek undue political advantage in the award process. It allows for winning proposers to acquire equipment and losing contractors to dispose of equipment in small parcels, thus reducing the overall risks associated with entry and exit. Finally, rotation of contracts increases the likelihood of consistently good performance by current contractors who also wish to propose on the new service package. (A contractor who is performing poorly on a current contract would not be likely to win a new package.)

M. Service Specifications

Public authorities clearly describe route alignments, public timetables, estimated annual service miles and service hours, and vehicle descriptions and appearance (color and exterior markings) in their contracts and requests for proposals. The public authorities also specify what ancillary services are to be provided, such as marketing, telephone information, etc.

N. Provision of Vehicles, Equipment, and Facilities

Vehicles for competitively contracted transit services may be provided by public authorities or by the private companies. Specialized transit equipment, such as vaulted fare boxes, usually are provided by the transit agency even when the agency does not supply vehicles. Facilities are rarely provided, but this practice may become more common as contracting expands and in high-cost cities where it is difficult for a private company to find or afford garage and maintenance space. An increasing number of public transit authorities, like the San Mateo County Transit District near San Francisco and the Dallas Area Rapid Transit Authority, have made or plan to make public vehicles available for use by private contractors to reduce costs and to increase competition. Fairfax County, Virginia, provides facilities and San Diego is planning to provide maintenance facilities for contractors.

There are several advantages to public vehicle (and facility) provision:

The federal government provides 80 percent of the cost of transit-agency vehicles. These monies may be used to pay depreciation for privately owned vehicles in use for contracting, but paperwork and procedures make direct provision easier;

Public authorities do not pay interest charges and taxes on vehicles; and

Public provision of vehicles ameliorates the private operator's risk associated with vehicle acquisition and disposal. A disadvantage of public vehicle provision is that the public authority incurs additional costs of monitoring the maintenance records of the private company operating the vehicles.

O. Insurance Coverage

Most public authorities require contractors to maintain accident and liability insurance limits at least as high as the public authorities carry themselves and similar to those required by the U.S. Interstate Commerce Commission. Any requirement above this common industry practice, even where it may be justified, adds to the costs of the contract.

P. Performance and Bid Bonds

Most public transit authorities require contractors to post bid (proposal) bonds and performance (service) bonds or their equivalents such as irrevocable letters of credit. (Bonds and letters of credit are financial instruments that guarantee payment to the transit agency if the contractor or bidder defaults.) Bid bonds or their equivalents are submitted by all bidders with their proposals and cover the agency's costs of re-awarding the contract plus the incremental costs of service during the extra time needed to award and start contracted service should the current bidder fail to begin service. Bid bonds or similar instruments are returned to losing bidders and to winning bidders upon commencement of service.

Performance bonds or similar instruments serve two primary functions:

To demonstrate the contractors' business soundness; and

To compensate the public authority for any losses resulting from contractor default.

Performance bonds and their equivalents represent the most simple and reliable indicator of the contractor's financial ability to perform. Public authorities are not skilled in judging the fiscal condition of private businesses, and it can be unwise for a public authority to perform such a task. Performance bonds and their equivalents can be an easy, cost-effective way for public authorities to minimize risks.

Performance bonds should be limited to the maximum potential loss to the public authority in the event of a default by a private transportation provider, and a consensus is arising that the maximum performance bond amount should be no more than three months' of the contract value. Even this may be excessive-there have been just five days of service lost as a result of contractor default in the United States during the past decade. Since public-transit service is readily available from the competitive market, the maximum foreseeable loss from a contractor default is the incremental cost of purchasing substitute service while a new procurement process is undertaken. The public cost of an unscheduled procurement process also is added to this incremental cost. San Diego County has developed its performance-bond requirement by making such a calculation and Miami allows contractors an option to performance bonds: the transit agency deducts a portion of the early contract payments and establishes an escrow account equal to the amount of a performance bond.

The necessity of ensuring the performance of private contractors must be balanced against the higher costs that are likely to occur from the requirement of performance bonds and their equivalents—their value should be no greater than the foreseeable loss.

Q. Performance Standards

Most contracts provide for some standards of performance. These may include indices for service quality (cleanliness, color, lettering, and decor of the vehicle; driver attire; and driver courtesy), on-time performance, trip completion, record keeping, and safety. Interestingly, the standards set for contracted services routinely exceed those standards previously—and often concurrently—set for service provided by the public authority. In many cases, there were no preceding standards for performance, although limited performance records are required by the federal government.

Safety: Most public transit contracts require that contractors include safety standards and vehicle maintenance standards.

Service Quality: Various service quality standards are customarily included in contracts, such as on-time performance, trip completion, vehicle cleanliness, driver courtesy, and passenger complaint rates.

R. Penalties and Incentives

Many public authorities specify financial penalties for unsatisfactory performance (in addition to the ultimate penalty, cancellation of the contract). Judiciously administered, financial penalties can enhance the likelihood that contracted service maintains high standards of quality and performance. Excessively high penalties or penalties based upon unreasonable standards impose additional costs on both the public authority and the contractor. Potential contractors will calculate the costs of excessive penalties and increase their proposal prices to compensate. Public authorities must evaluate the total costs and benefits of each penalty. Incentives generally have not been used in competitively contracted bus services because public authorities have assumed that the profit motive will be incentive enough for a responsible private provider.

S. Public Supervision

Public-transit services require extensive supervision, whether they are provided by the public authority itself or by private contract. The additional costs of supervising competitively contracted services are small. London Regional Transport has reported that its incremental contract monitoring cost was 2.5 percent of contract value for a program that involves more than 20 contracts and 800 competitively contracted buses. Ann Arbor, Michigan, reported incremental supervision costs of less than 2 percent. Common sense would indicate that the costs of supervision would be directly correlated to the extent of the monitoring effort. This is usually, but not always, the case. Public transit authorities have been innovative with regard to supervision. Miami uses temporary help to do random monitoring of on-time performance and service quality, permitting a higher degree of monitoring than would otherwise be possible. Carson, California performs random monitoring but supplements this with routine calls to frequent riders for comments on performance issues.

Changes in circumstances and supplier markets may require alterations in competitive-contracting processes and practices. Despite modifications in design, circumstances, and markets, the success of competitive contracting rests on three fundamental principles: public control, cost effectiveness, and open access and process (see Figure 2). First, the public authority has a responsibility to the riders and taxpayers to ensure that public services meet quantity and quality standards that are set by government—this requires public control. Second, competitive contracting programs must foster the development and maintenance of a truly competitive market so that costs are kept under control. Third, these two principles are best served when all interested parties have access to the procurement process and records. The implications of these three principles are described below:

|

PRINCIPLES OF COMPETITIVE CONTRACTING FOR TRANSIT SERVICES |

|

| Public Control | þ Service design |

| þ Service monitoring | |

| þ Contract to lowest responsive and responsible bidder | |

| Competitive Market | þ Request for proposals (RFPs) to all potential proposers |

| þ RFPs clearly specify service requirements | |

| þ Contracts for small increments of service | |

| þ Contracts and extensions total no longer than 5 years | |

| þ Contract expiration dates staggered (multiple contracts) | |

| þ Limited market share | |

| þ Fixed-price contracts | |

| þ Fair participation by public agency | |

| Fully Open Process | þ Open pre-proposal conference |

| þ Wide advertisement of RFP | |

| þ RFPs and copies of contracts to all interested parties | |

PRINCIPLE #1:

Public control should be retained over services.

A. Public authorities should design the service consistent with schedules, standards, and performance criteria that it has established, and at the fares it has established.

B. Public authorities should closely monitor service-contract compliance as a routine activity, whether the contract has been awarded to a public authority or a private company. Public authorities should be prepared to invoke the contract provisions required to ensure public service of specified quality and quantity.

C. Contracts should be awarded to the lowest responsible and responsive proposer: the public authority should ensure that it is obtaining service from a company that is capable of providing the service having proven its financial and management responsibility in similar services. Further, the public authority should ensure that it awards the contract to a company that understands the service package, having submitted a proposal that is sufficiently responsive to the public request for proposals that was issued for the service.

PRINCIPLE #2:

A competitive supplier market should be fostered to ensure the most cost-effective service.

A. Requests for proposals should be provided to all potential proposers in sufficient time to pen-nit well-considered responses.

B. Each request for proposals should cover the smallest increment of service practical so that the maximum number of qualified proposers may respond.

C. Requests for proposals should clearly specify all service requirements and contain clear and concise information on the required format of proposals.

D. Service contracts should be subject to new requests for proposals at least every five years, whether the incumbent operator is a private company or a public authority.

E. Contract expiration dates should be rotated to minimize the increment of service being competitively contracted at a particular time.

F. No single private company should be permitted to contract for an excessive percentage of public-transit service.

G. Contract prices should be subject to negotiation after contract award only in extreme cases: No payment adjustment should be permitted except as specified in the contract according to the provisions of the request for proposals, or where extremely unusual circumstances have resulted in cost increases that are both outside the control of the contractor and have similarly impacted all potential contractors in the supplier market.

H. Public authorities should participate fairly in the procurement process:

Individuals and departments involved in preparing a public-authority proposal should not take part in the evaluation of proposals.

Public authorities should submit sealed proposals subject to the request-for-proposals deadline.

Public authorities should be subject to the same proposal and contract terms, conditions, and performance criteria as would apply to a private company including termination provisions.

Public-authority proposals should include the attributable fully allocated operating and capital costs for the functions proposed for purchase through the request for proposals.[31]

Public authorities should include cost-saving innovations in their proposals only to the extent that such innovations are used in other services provided by the public authority. (To permit otherwise encourages public authorities to reduce proposal costs for the purpose of winning contracts without reducing overall public costs.)

I. Where there are public capital facilities, they should be made available to the successful public or private proposer to provide the specified service. This will minimize capital and financing costs.

J. Public authorities should impose no contractor employee requirements beyond compliance with applicable labor laws.

PRINCIPLE #3:

Requests for proposals and final contracts and prices should be disseminated to any and all parties that solicit the information. Pre-proposal conferences should be open to all private operators and their designees. Public authorities should formally adopt, advertise, and abide by this principle of "open process" to assure the integrity of the procurement system and to encourage healthy, fair competition.

As a result of high and rising transit costs, many transit agencies in the United States and throughout the world have turned to the private sector as an alternative. Deregulation can save public money and result in more innovative and responsive van and bus service. But competitive contracting is the only widely viable private-sector alternative to high and rising public transit costs in low-demand markets such as those in the United States and where full public control of transit is desired.

Although there is much opposition to competitive contracting, a well-designed, carefully monitored competitive contracting program yields direct savings of more than 30 percent in the United States. A number of studies of competitive contracting indicate the service quality, safety, and reliability of contracted services equals or exceeds that of the public sector.

The success of transit contracting rests on three fundamental principles: public control, competition and cost effectiveness, and open access and process. First, the public authority has a responsibility to the riders and taxpayers to ensure that public services meet quantity and quality standards that are set by government—this requires public control. Second, competitive-contracting programs must foster the development and maintenance of a truly competitive market so that costs are kept under control. Third, these two principles are best served when all interested parties have access to the procurement process and records.

Jean Love and Wendell Cox are consultants who have completed transit projects in Canada, the United States, Australia, New Zealand, and the United Kingdom. They are associated with Wendell Cox Consultancy in Belleville, Illinois.

1. Prior to passage of the Urban Mass Transportation Act of 1964, most transit service in the United States was produced without public subsidy by franchised private companies. The companies obtained revenue through passenger fares and advertising. Ridership plunged after World War 11, when gasoline rationing was lifted. As their revenues plunged, the private franchised companies could not afford to offer service on low-use routes at the current fares, but the franchise boards that regulated transit were reluctant to allow companies to abandon low-use routes or to raise fares. Federal legislation helped cities finance a buy-out of the private companies, and public subsidies allowed transit to continue to service on low-use routes.

2. Data from National Urban Mass Transportation Statistics: Section 15 Annual Report (Washington, D.C.: U.S. Department of Transportation, Urban Mass Transportation Administration, multiple editions); Transit Operating and Financial Statistics (Washington, DC: American Public Transit Association, multiple editions). The Urban Mass Transportation Administration changed its name to the Federal Transit Administration in 1991.

3. Trends in Public Infrastructure Outlays and the President's Proposals for Infrastructure Spending in 1993 (Washington, D.C.: Congressional Budget Office, May 1992).

4. The Intermodal Surface Transportation Efficiency Act of 1991 authorized a 50 percent increase in federal subsidies to transit and allowed for additional monies to be diverted from highway funds.

5. William F. Shughart and Mwangi Kimenyi, Public Choice, Public Subsidies, and Public Transit (Washington, D.C.: U.S. Department of Transportation, Urban Mass Transportation Administration, Office of Private Sector Initiatives, February 1991); Don Pickrell, "Rising Deficits and the Uses of Transport Subsidies in the United States", Journal of Transport Economics and Policy, Vol. 24, 1985; Robert Cervero, "Effects of Operating Subsidies and Dedicated Funding on Transit Costs and Performance," Urban Analysis, Vol. 8, 1984; John Pucher, "Effects of Subsidies on Transit Costs," Transportation Quarterly (Westport, Conn.: Eno Foundation for Transportation, October, 1982); and Wendell Cox and Jean Love, "Controlling the Demand for Taxes through Competitive Incentives," Government Union Review, Vol. 12, No. 2 (Spring 1991).

6. Jean Love and Wendell Cox, False Dreams and Broken Promises: The Wasteful Federal Investment in Mass Transit (Washington, D.C.: The Cato Institute, 1991).

7. Charles Lave, Measuring the Decline in Transit Productivity in the U.S. (Thredbo, NSW, Australia: International Conference on Competition and Ownership of Bus and Coach Services. 1989) and Don Pickrell, The Causes of Rising Transit Operating Deficits (Washington, D.C.: U.S. Department of Transportation, Urban Mass Transportation Administration, 1983).

8. Wendell Cox and Jean Love, A Public Purpose for Public Transit, Reason Foundation Local Government Center Study #207, (Santa Monica, CA: Reason Foundation, January 1990).

9. Calculated from Interstate Commerce Commission and American Bus Association data.

10. Calculated from the National Urban Mass Transportation Statistics: Section 15 Annual Report (Washington, D.C.: U.S. Department of Transportation, Urban Mass Transportation Administration, multiple editions); and Transit Operating and Financial Statistics (Washington, DC: American Public Transit Association, multiple editions).

11. Wendell Cox, Optimizing Public Transit Service through Competitive Contracting (Washington, D.C.: Department of Transportation, Urban Mass Transportation Administration, 1987).

12. Almost 10 percent of regular transit route services are provided by private contractors. 8 percent is provided by competitively procured contractors; 2 percent is provided by franchised private operators, predominately in New York and New Jersey. Data from School Bus Fleet Annual Fact Book (January 1991) and National Urban Mass Transportation Statistics: 1990 Section 15 Annual Report (Washington, D.C.: U.S. Department of Transportation, Urban Mass Transportation Administration, 1992).

13. Wendell Cox and Jean Love, International Experience in Competitive Tendering, presented to the Second International Conference on Privatization and Deregulation in Passenger Transportation, Tampere, Finland, June 1991.

14. Alan E. Pisarski, Travel Behavior Issues in the 90s and New Perspectives in Commuting (Washington, D.C.: U.S. Department of Transportation, Federal Highway Administration, Office of Highway Management, July 1992). Transit figure adjusted to account for intercity private bus and taxicabs.

15. "Illegal" vans and buses currently operate in New York and Miami offering unsubsidized transit services at fares lower than those charged by the respective transit authorities. Both cities have fined drivers and impounded vans. E.S. Savas, Sigurd Grava, and Roy Sparrow, The Private Sector in Public Transportation in New York City: A Policy Perspective (New York: Institute for Transportation Systems, City University of New York, 1991); Daniel Machalaba, "Opportunistic Vans Are Running Circles Around City Buses," The Wall Street Journal, July 24, 1991; and Dan Holly, "It's Metro vs. Minis in the Battle of Buses," The Miami Herald, May 4, 1991.

16. Private Sector Briefs: Private Sector Involvement in Public Transportation (Washington, D.C.: U.S. Department of Transportation, Urban Mass Transportation Administration, Office of Private Sector Initiatives, 1988, 1990, 1992); R.F Teal, G. Giuliano, and E. Morlock, Public Transit Service Contracting (Washington, D.C.: U.S. Department of Transportation, Urban Mass Transportation Administration, 1986).

17. KPMG Peat Marwick, Subhash R. Mundle and Associates, and Transportation Support Group, Denver RTD Privatization Performance Audit Update (Denver: November 1991).

18. Wendell Cox and Jean Love, "Reclaiming Transit for the Riders and the Taxpayers," Critical Issues: How Privatization Can Solve America's Infrastructure Crisis, Edward L. Hudgins and Ronald D. Utt, eds. (Washington, D.C.: The Heritage Foundation, 1992).

19. Price Waterhouse, Subhash R. Mundle and Associates, Benjamin D. Porter, and Patti Post and Associates, Bus Set-vice Continuation Project: Final Report (Los Angeles: January 1992).

20. Data from National Urban Mass Transportation Statistics: Section 15 Annual Report (Washington, D.C.: U.S. Department of Transportation, Urban Mass Transportation Administration, multiple editions).

21. Wendell Cox and Jean Love, "Designing Competitive Tendering Systems for the Public Good: A Review of the U.S. Experience," Transportation Planning and Technology, Vol. 25 (London, U.K.: Gordon and Breach Science Publishers, June 1990).

22. For example, Price Waterhouse, Subhash R. Mundle and Associates, Benjamin D. Porter, and Patti Post and Associates, Bus Service Continuation Project: Final Report (Los Angeles: January 1992) and KPMG Peat Marwick, Subhash R. Mundle and Associates, and Transportation Support Group, Denver RTD Privatization Performance Audit Update (Denver: November 199 1).

23. See also, Jean Love and Jim Seal, "Competitive Contracting in the US: Overcoming Barriers," paper presented to the Second International Conference on Privatization and Deregulation in Passenger Transportation in Tampere, Finland (June 1991).

24. (See also endnote 30.) To ensure that the riders of Boston's public-transit system received the full benefit of increasing public-transit subsidies, Massachusetts enacted (1980) a law to reserve public prerogative (public management right) in organizing and managing the delivery of the public-transit services of the Massachusetts Bay Transportation Authority (MBTA) in Boston. The act prohibited MBTA from bargaining collectively or entering into any agreement over inherent management issues including competitive contracting. (A legal challenge by the transit unions yielded a United States Court of Appeals decision upholding the Massachusetts law.)

25. For a full exploration of perceptual barriers, see Wendell Cox and Jean Love, "Bus Service," Privatization for New York: Competing for a Better Future, E. S. Savas (ed), A Report of the New York State Senate Advisory Commission on Privatization, Ronald S. Lauder, Chairman (New York, N.Y.: 1992).

26. Public transit authorities sometimes have understated their costs in third-party procurements. (A "third-party procurement" is one in which a publicly funded agency, other than the contracting authority itself, responds to a request for proposals. The publicly funded agency may be a neighboring transit authority, a university, or some other branch of state or local government. It is a third-party procurement, for example, if transit authority B responds to a request for proposals issued by transit authority A.)

27. Chief Counsel of the Urban Mass Transportation Administration, Yellow Cab Company v. Jaunt, Inc., June 30, 1988.

28. Michael Keough, Scale Economies Among United States Bus Transit Systems (Washington, D.C.: U.S. Department of Transportation, Urban Mass Transportation Administration, 1989).

29. A draft report on U.S. contracting from 1984 to 1992 by Travers Morgan and Wendell Cox Consultancy found that contracts for 50 buses or more attracted the smallest number of bidders regardless of which party supplied the buses. When agencies supplied buses, more bidders were attracted by service contracts of 15 buses or less. When contractors were required to supply buses, the largest number of bidders were attracted by service packages of 15 to 29 buses. (See July to August 1992 Transit Times, a publication of the American Bus Association.)

30. Colorado Senate Bill 164 and The Public Transportation Consumer Protection Act, The Source Book of American State Legislation, Vol. 6 (Washington, D.C.: American Legislative Exchange Council, 1990-1992). The Colorado bill was the first state legislation to mandate competitive contracting of transit services. The Denver transit agency was required to contract for 20 percent of its bus service.

31. Nonattributable costs, that is, capital and operating costs that represent functions not covered by proposed service contract (most typically, planning and marketing) should not be included in public-agency cost comparisons. Use of fully allocated or total costs provides realistic estimates of the stable, long-term costs of the agency and savings through competitive contracting. Use of marginal costs as inappropriate for public-sector monopolies like transit, which are characterized by unproductive use of resources.