Public officials need accurate cost comparisons of in-house vs. outsourcing to make informed decisions. This guide presents a step-by-step approach for assessing the true cost of providing services. 18 pages.

Fiscal constraints are prompting state and local officials to streamline government operations, and contracting out has emerged as a popular tool for providing high-quality services at the lowest possible cost. State and local governments in the United States currently contract for over $100 billion in services every year, and interest in contracting out is increasing.

Though there are many considerations that enter into the privatization decision, cost is unquestionably among the most important. Public officials seeking to make an informed judgment need access to accurate assessments of the costs of both in-house and contracted services. This guide presents a step-by-step approach for assessing the true cost of service provision.

Historical public-sector accounting practice is ill-suited to this task. The most common reason governments contract out is to save money, yet because government activities are typically funded through several departments, officials are often unaware of the full . cost of providing a given service. One major national study suggests that the true cost of public service provision is frequently underestimated by as much as 30 percent. This guide identifies costs that are often ignored in calculating in-house costs.

Likewise, ancillary costs associated with contracted services, such as contract administration and monitoring of performance, can often be overlooked as well. This guide presents accepted financial practices for estimating the total cost of a contract, which includes monitoring and administration.

The question of which costs should be considered—fully allocated, avoidable, and marginal-in comparing service delivery options is also addressed. These accounting concepts are defined, and their appropriate use in choosing a means of service provision and estimating cost savings is discussed.

State and local governments contract out for over $100 billion in services annually.[1] The reason most frequently given for contracting out is to reduce the cost of service delivery.[2] For public officials to make informed judgments about contracting out, valid comparisons need to be made between the costs of in-house and contracted service delivery.

Cost is not the only consideration for public officials making the decision between public and private service provision. Issues such as service quality, managerial flexibility, the likelihood of labor actions, the extent of competition among providers, and other factors must be scrutinized as well. Cost is simply one component—although an important one—in the decision matrix.

Attempting to compare the costs of in-house and contract service delivery is difficult. One major national study suggests that the cost of in-house service delivery is frequently underestimated by as much as 30 percent.[3] Case-study evidence also suggests that the cost of contract service delivery is often underestimated as well, due to a failure to properly account for such costs as contract administration and monitoring.[4]

Part of the difficulty is inherent in the nature of the task. As Jonathan Richmond of MIT's Center for Transportation Studies has observed:

"Cost analysis is art, not science. In complex organizations, large numbers of assumptions must be made about how costs which are incurred are to be allocated to various parts of the organization. Many costs are shared by a number of services, and there is often no one obvious way of assigning them to their sources.”[5]

The failure of governments to accurately compute the costs of in-house and contract service delivery is also related to the absence of a consistent methodology that ensures all relevant costs are included in the analysis. In a recent survey of the contracting out practices of 120 cities, counties, and special district governments nationwide, 50 percent of the respondents reported having no formal methodology for conducting cost comparisons.[6]

This guide provides a structured approach for making cost comparisons between in-house and contract service delivery that will be applicable to most state and local governments. The approach outlined here is based on: 1) mainstream public financial management thinking; 2) the best identified practices of federal, state, and local governments; and 3) a desire to keep the process as simple as possible while ensuring a high degree of validity. Though no set of accounting guidelines, however standardized or well-designed, can totally eliminate subjective judgments, this guide provides a useful framework for assessing the costs of public service provision versus contracting out.

Determining the total cost of in-house service delivery is discussed first. The next section considers the cost of contract service delivery. The issue of which in-house costs—"fully allocated" or "avoidable"—to use in comparing costs with contract service delivery is then addressed. As part of this discussion, a format is presented to display and compare cost data between in-house and contract service delivery. Finally, the relatively new phenomenon of in-house government departments bidding against contractors is discussed. Throughout this guide, an in-house service being considered for contracting out is referred to as a "target service."

The total cost of providing a target service in-house, also known as the fully allocated cost, is the sum of its direct costs plus a proportional share of organizational overhead, or indirect costs.[7] When the direct and overhead costs of a target service are identified, the resulting dollar amount constitutes the "fully allocated cost," or total cost, of providing a target service in-house.[8]

A. Direct Costs

Direct costs are those cost items that only benefit, and thus are totally (100%) chargeable to a target service. Examples of direct costs include the salaries, wages, and fringe benefits of government employees who work exclusively (100%) on the in-house delivery of a target service, as well as the costs of supplies, materials, travel, printing, rent, utilities, communications, and other costs consumed or expended for the exclusive benefit of a target service.

B. Direct Costs Frequently Overlooked

Some direct-cost items are routinely overlooked when computing the cost of providing a target service in-house and thus warrant special mention. Frequently overlooked cost items include: interest costs, pension costs, and facility and equipment costs.

INTEREST COSTS

Interest on capital items purchased for the exclusive (100%) use of a target service through a bond issue or other financing arrangement should be included as a direct cost of in-house service provision. For example, a fire truck purchase that is financed will typically take interest payments from a local government's general fund, but this cost should be counted toward the cost of fire-protection services. (Equipment costs are handled below.)

PENSION COSTS

The pension costs of government employees who work exclusively (100%) on a target service should be included as a direct cost of in-house service provision regardless of whether the government fully funds the pension plan or not. Unfunded and under-funded pension plans defer, but do not avoid, these costs.

FACILITY AND CAPITAL EQUIPMENT COSTS

Facilities and capital equipment used exclusively (100%) for a target service should also be included as a direct cost of in-house service provision. Depreciation costs can be computed, or, if depreciation is not appropriate or no depreciation schedule exists, a use-allowance factor can be computed. (Use allowances are employed for those capital items for which no depreciation schedule exists. For most municipal items, depreciation is appropriate.) Even when no actual cost is incurred, a use allowance factor should still be included because the asset could be used for other government purposes or sold.

C. Overhead Costs

Overhead costs, or indirect costs, are cost items that benefit the target service and at least one other government service, program, or activity. The expenses of various administrative and support services provided to a target service by other governmental departments are overhead costs.[9] Examples include: salaries, wages, fringe benefits, supplies and materials, travel, printing, rent, utilities, communications, and other costs that benefit the target service and at least one other government service, program, or activity. A check should also be made to ensure that overhead costs include applicable interest costs, pension costs, and depreciation or use-allowance costs on shared facilities and equipment. If not, these costs should be added to applicable overhead costs.

Overhead costs are generally apportioned among government services, programs and activities according to some allocation scheme. The most common methods are "personnel costs," "total direct costs" and the "step-down" method.[10] The personnel-cost method assumes that overhead costs are proportional to the number of employees (or full-time equivalent employees). The total direct-cost method assumes overhead is proportional to the budget of the target service. And the step-down method divides all departments into either support or production departments, and works by allocating all the costs of support departments to the other entities they serve.

Many state and local governments have automated accounting systems capable of identifying, tracking, and allocating overhead costs. Frequently, state and local governments develop overhead or indirect cost rates that are simply applied to the personnel or total direct costs of a target service.

The total cost of contract service delivery is the sum of: 1) contractor costs; plus 2) contract administration costs; plus 3) an allowance for one-time conversion costs; minus 4) off-setting revenues.

A. Contractor Costs

Contractor costs may be the easiest component of contract-service delivery costs to compute. Contractor costs are simply the total costs a contractor proposes to charge for performing the target service. Contractor costs can generally be taken directly from a contractor's bid or proposal.

B. Contract Administration Costs

Contract administration costs may be the most difficult component of contract-service delivery costs to compute. Contract administration can be defined as all those activities that take place from the time a decision is made to contract out until the contract is fully executed and final payment is made.[11] Contract administration costs include: procurement, contract negotiations, contract award, the processing of amendments and change orders, the resolution of disputes, the processing of contractor invoices, and contract monitoring and evaluation.

The two major methods in use for estimating the cost of contract administration are informed judgment and federal Office of Management and Budget (OMB) guidelines.

INFORMED JUDGMENT

Based on state and local government experiences with contracting out, the costs of contract administration have been assessed at between zero and 25 percent of contractor costs. At the low end of the cost range falls the County of Los Angeles, which computes the costs of contract administration at zero.[12] In Los Angeles County, existing staff are assigned contract administration duties in addition to their regular job responsibilities. Consequently, the county maintains that no additional contract administration costs are incurred when a target service is contracted out.

Estimating the cost of contract administration at zero almost certainly underestimates the true cost.[13] Even when existing staff are used to perform the contract monitoring function, government departments such as purchasing and finance still experience workload increases with attendant cost implications. For example, purchasing departments have new bid and proposal packages to develop and issue, and finance departments have new contractor invoices to process and audit.

At the high end of the cost range is the estimate of 25 percent of contractor costs derived from a major study of municipal contracting out in the greater Los Angeles area.[14] Other estimates of contract administration costs fall somewhere between these two values. The City of Cincinnati, Ohio, uses a figure of 4 percent of contractor costs unless more precise cost data are available.[15] E. S. Savas, a nationally recognized expert on contracting, estimates the cost of contract monitoring-exclusive of other contract administration costs-at between 2 and 7 percent of contractor Costs.[16] John Rehfuss, another contracting expert and a former city manager, suggests that the cost of contract monitoring-again exclusive of other contract administration costs-is probably closer to 5 or 10 percent of contractor costs.[17] This cost may depend on what soft of service is contracted, and the ease with which it can be objectively measured and monitored.

Whereas the estimate of zero underestimates monitoring costs, computing the costs of contract administration at 25 percent of contractor costs probably overestimates the true cost. Most state and local governments should conduct at least some monitoring of in-house service delivery, so contract monitoring costs should not represent entirely new costs.

When all contract administration costs—not just monitoring costs—are considered, estimates can increase substantially. For example, the City of Phoenix, Arizona estimates the administration costs of its former sanitation contracts to be 16 percent of contractor costs.[18] A growing body of evidence suggests that on average the true cost of comprehensive contract administration falls between the two extremes of zero and 25 percent.

Based on the judgments and experiences noted above, a reasonable estimate for contract administration costs is between 10 and 20 percent of contractor costs.[19] A general rule of thumb in applying this cost range would be to move toward the higher end of the range for small dollar contracts and the low end of the range for large dollar contracts. In instances where existing staff are assigned contract-monitoring responsibilities, the low end of the range should probably be used.

OMB GUIDELINES

An alternative approach to computing the cost of contract administration is to utilize the staffing formula developed by the federal Office of Management and Budget (OMB). In 1985, OMB revised its Circular A-76, which governs the contracting out of commercial activities, to require the use of a staffing formula to estimate contract administration costs.[20] The OMB staffing formula is derived from a major study of federal contracting out conducted by the accounting firm then known as Peat, Marwick and Mitchell.[21]

The OMB staffing formula assumes that the best indicator of contract-administration requirements is the number of people engaged in providing a service—the larger the staff working on a particular service, the greater the contract-administration requirements. The OMB staffing formula (see Table 1) is based on the number of staff required to provide a target service in-house. The number of in-house staff is then related to the number of full-time-equivalent (FTE's) government personnel needed for contract administration if the target service is contracted out.

Table 1

|

OMB STAFFING FORMULA FOR COMPUTING THE COSTS OF GOVERNMENT CONTRACT ADMINISTRATION |

|

|

In-house staffing estimate |

Contract administrative staffing requirements in FTE’s |

|

10 or below |

0 |

|

11-20 |

1 |

|

21-42 |

2 |

|

43-65 |

3 |

|

66-91 |

4 |

|

92-119 |

5 |

|

120-150 |

6 |

|

151-184 |

7 |

|

185-222 |

8 |

|

223-265 |

9 |

|

266-312 |

10 |

|

313-367 |

11 |

|

368-429 |

12 |

|

430-500 |

13 |

|

501-583 |

14 |

|

584-682 |

15 |

|

683-800 |

16 |

|

Above 800 |

2% of the in-house staffing estimate |

Source: U.S. Office of Management and Budget, Supplement to OMB Circular No. A-76 (Revised). Performance of Commercial Activities (Washington, D.C.: U.S. Government Printing Office, 1985), p. IV.37.

Because of the complexity of federal contract procurement laws and regulations, the OMB staffing formula may overestimate the actual cost of contract administration for some state and local governments. The Texas State Auditor's Office, for one, has revised the OMB staffing formula for purposes of computing the costs of Texas state agency contract administration.[22] The revised Texas contract administration staffing formula is shown in Table 2.

Table 2

|

STATE OF TEXAS CONTRACT ADMINISTRATION REQUIREMENTS |

|

|

In-House Staffing Requirements |

Contract Administration Staff |

|

Less than 20 |

1 |

|

11-20 |

2 |

|

21-42 |

3 |

|

43-65 |

4 |

|

66-91 |

5 |

|

92-119 |

6 |

|

120-150 |

Use 2-4% of |

Source: Office of the Texas State Auditor, Guide to Implement the Competitive Cost Review Program, (Austin, TX: 1984). P.32.

C. One-Time Conversion Costs

One-time costs are sometimes incurred when converting a target service from in-house to contract service delivery. Examples of one-time conversion costs include: 1) personnel-related costs; 2) material-related costs; and 3) other costs. When substantial one-time conversion costs are involved, these costs should be amortized over multiple years. The "front-end-loading" of substantial one-time conversion costs into one year can skew cost comparisons between in-house and contract service delivery in favor of the former.[23]

PERSONNEL-RELATED COSTS

Personnel-related costs include unemployment compensation, accrued annual and sick-leave benefits, and other severance items that must be paid to terminated government employees.

MATERIAL-RELATED COSTS

Material-related costs include costs associated with the preparation and transfer of government property or equipment to be made available to a contractor for use in providing a target service.

OTHER COSTS

Other costs include any other one-time conversion costs, such as penalty fees associated with terminating leases or rental agreements, the costs of unused or underused facilities and equipment until other uses are found or they are sold, and other costs associated with the transition.

D. Off-Setting Revenues

An off-setting revenue is any new or enhanced revenue stream (e.g. state or local income, sales, property or other taxes, user fees, etc.) that will accrue to the government as a result of contracting out a target service. If a revenue stream is already being received by a government and no increase is anticipated, then no entry is required. An item here that is sometimes overlooked is revenue to be derived from the sale or other disposition of facilities or equipment made redundant as a result of contracting out a target service. Any amount included in this section represents a deduction from the cost of contract service delivery.

E. The Total Cost of Contract Service Delivery

When contractor costs, contract administration costs, and one-time conversion costs are combined and reduced by any off-setting revenues, the resulting dollar amount represents the total cost of contract service delivery.

A. When to Use Fully Allocated Costs

As noted earlier, the total cost, or fully allocated cost of providing a target service in-house is the sum of its direct and overhead indirect costs. Cost comparisons using fully allocated costs are useful in determining if the in-house cost of providing a target service is comparable with private-sector market prices.[24] The state of Texas, for example, routinely compares the fully allocated cost of in-house service delivery with private-sector market prices. If the fully allocated cost of in-house service delivery is greater than 110 percent of the prevailing private-sector market price, the state agency must reduce its costs within a specified period of time or the service may be targeted for contracting out. In addition, it may be appropriate to consider fully allocated costs when comparing the operating efficiency of service delivery before and after privatization. For example, if prior to privatization the per-household fully allocated unit cost of public garbage collection was $9, compared to total private-contracting costs of $6, these figures may be used to reflect the relative operating efficiency of public and private service provision. These figures do not, however, necessarily reflect the cost savings that will be realized through privatization, for reasons explored in the next section.[25]

B. When Not to Use Fully Allocated Costs

The use of fully allocated costs is generally inappropriate in estimating the savings to be realized by contracting out a target service that is currently being conducted in-house. In other words, the amount of money that is likely to be saved is not simply the difference between fully allocated in-house costs and the total contracting cost. This is because contracting out does not generally result in a dollar-for-dollar reduction in governmental overhead costs. For example, the contracting out of a target service, or a portion thereof, may result in decreasing the workload of service departments like personnel, finance, and facilities management but the workload reductions may be insufficient to have any significant effect on the costs of maintaining these departments. When attempting to determine the potential cost savings associated with the contracting out of a target service, the appropriate in-house costs to use in the comparison are the "avoidable costs"; these are defined in the next section.

C. Avoidable Costs

Avoidable costs are those in-house costs that will not be incurred if a target service, or portion thereof, is contracted out.[26] How-to contracting books,[27] as well as several contracting-out guides prepared by state and local governments,[28] recommend the use of avoidable costs when assessing the likely cost savings achievable through contracting out. The use of avoidable, or incremental, costs is also the generally accepted managerial accounting approach to conducting the financial component of a business "make-or-buy" decision.[29] Determining which in-house costs are avoidable is not a simple task. Of course, virtually all direct costs will be avoidable. But ascribing what portion of overhead costs are avoidable is a matter of judgment, and depends largely on three factors:

The determination of the public sector to reallocate resources efficiently;

The extent of the privatization effort, both in the target service area and in other services that employ the support of the same government departments; and

The time period in-which resource allocation is expected to occur.

RESOURCE REALLOCATION

In the private sector, the decision to discontinue a particular function is usually accompanied by a swift reallocation of resources in support areas as well. For example, a company that eliminates a product line that accounts for 30 percent of sales will not only eliminate those positions directly involved in manufacturing that product, but is also likely to reduce the size of support staff—such as personnel, procurement, accounting, etc.—by something approaching 30 percent. The private sector has a strong incentive to reduce overhead as much as possible. The public sector lacks such strong incentives, and the extent to which overhead costs can be avoided in the wake of contracting out is partly a function of political will.

EXTENT OF PRIVATIZATION

The reduction in overhead costs is related to the extent of the privatization, as illustrated in the janitorial example presented below. There is a cumulative effect to be considered, in that contracting out not only in the target service but in other services which make use of the same overhead support functions influences the potential for overhead reduction. For instance, contracting out a service with only five employees would be unlikely to reduce overhead by any appreciable amount, unless several other small programs were also being contracted out as well. Several small contracts, which considered separately would have a negligible impact on overhead, could in the aggregate reduce overhead significantly.

TIME FACTOR

There are many costs that cannot be avoided in the short term that may be avoidable in the long term. For example, contracting out of a portion of transit service may leave a public entity holding a lease for more storage and maintenance capacity than is necessary. In the short term, that cost may be unavoidable, but in the long term the public entity could decline to renew the lease. Similarly, there may be instances in which contracting out leaves a public entity over-staffed but legally obligated not to lay off workers. In the short term, this represents an unavoidable cost, but in the long term, staff levels could be reduced to efficient levels through attrition.

Avoidable costs can never exceed fully allocated costs. You can never avoid more than the service currently costs to provide. Over the long term, however, an organization should reconfigure itself so that overhead is adjusted downward to an efficient level. MIT's Jonathan Richmond has written that "in the longer term, as a general rule... marginal costs approach and converge with fully allocated total costs."[30] In this way, fully allocated costs can be thought of as the long-term theoretical upper limit of avoidable costs.

This emphasis on avoidable costs does not mean that computing the fully allocated costs of providing a target service in-house is a superfluous exercise. In order to determine the costs to be avoided by contracting out, the fully allocated costs of in-house service delivery must first be determined. And, as mentioned previously, fully allocated costs are appropriate when comparing operating efficiencies of the public and private sectors.

In all cases, the sought-after figure when estimating cost savings should be:

D. Cost Comparisons Using Fully Allocated Costs and Avoidable Costs: Two Scenarios

The rationale for using avoidable costs when evaluating likely cost savings from contracting is perhaps best explained by a pair of examples. Table 3 compares the fully allocated costs of providing in-house Janitorial services at a 10,000 square feet county government facility with the costs that will actually be avoided if the county decides to contract out.

Table 3

|

SCENARIO ONE: COMPARISON OF FULLY ALLOCATED COSTS AND AVOIDABLE COSTS |

||

|

Cost Item |

Fully Allocated Costs |

Avoidable Costs |

|

Direct Costs |

|

|

|

Salaries and wages |

$20,000 |

$20,000 |

|

Employee benefits (@ 21.25%) |

$4,250 |

$4,250 |

|

Supplies |

$2,000 |

$2,000 |

|

Total Direct Costs |

$26,250 |

$26,250 |

|

Indirect Costs |

|

|

|

Division overhead |

$11,520 |

0 |

|

Branch overhead |

$1,683 |

0 |

|

Department overhead |

$4,452 |

0 |

|

Countrywide overhead |

$2,792 |

0 |

|

Total Indirect Costs |

$20,447 |

0 |

|

Total Direct and Indirect Costs |

$46,697 |

$26,250 |

|

Cost per square foot |

$4.67 |

$2.63 |

Source: Joseph T. Kelly, Costing Government Services: A Guide for Decision Making, (Washington, D.C.: Government Finance Officers Association, 1984), p. 107, used with permission.

In this scenario, the county has received a responsive bid from a responsible bidder in the amount of $32,500, or $3.25 per square feet to provide janitorial services at the facility for a period of one year.

The county has an automated accounting system capable of identifying, tracking and allocating overhead costs and developing overhead rates for its various management levels. The overhead rates in ascending order are: division level (57.508%), branch level (8.413%), department level (22.259%) and countywide level (13.957%). These overhead rates are applied to a base of salaries and wages. The question is: will the county reduce the cost of janitorial services at the 10,000 square feet facility by contracting out?

As Table 3 illustrates, the fully allocated costs of providing janitorial services in-house at the 10,000 square feet county facility for a period of one year consist of $26,250 in direct costs (salaries, wages and benefits of 2 custodians and an allowance of $2,000 for supplies) plus $20,447 in allocated overhead costs for a total of $46,697 or $4.67 per square feet. When the in-house cost ($4.67 per square feet) is compared to the bid price of $3.25, it appears that the county can reduce service delivery costs by $1.42 per square feet, or $14,200, by contracting out. This estimate of cost savings however is illusory as the avoidable cost analysis demonstrates.

If the county contracts out in this scenario, only the direct costs ($26,250) of in-house service delivery will actually be avoided. No overhead costs will be avoided because the amount of in-house janitorial activity being contracted out is too marginal to affect overhead costs. Only the $2.63 per square feet of direct costs will be avoided, but $3.25 per square feet (the contractor's bid) in new costs will be incurred. Thus, in this scenario, contracting out will actually increase, rather than reduce, service delivery costs. For contracting out to be justifiable purely on the grounds of reducing service delivery costs, the amount of existing in-house costs to be avoided must be greater than the new costs of contract service delivery that will be incurred. One can properly conclude that the greater the proportion of an in-house service targeted for contracting, the greater is the potential impact on overhead cost, and thus the greater the potential to reduce service delivery costs,

Table 4 presents a second contracting-out scenario where the county is contemplating contracting out all in-house janitorial services. The contract would involve 1,691,500 square feet of county facility space, and the contractor's bid is again computed at $3.25 per square feet for a period of one year. In this scenario, all direct costs associated with in-house delivery of janitorial services will be avoided. Additionally, all division and branch overhead will be avoided because these supervisory and operational support levels, with their attendant costs, will now be the responsibility of the contractor. Also, a significant proportion of department and countywide overhead costs-but not all-will be avoided because these management levels will no longer be required to provide services (e.g., personnel, finance, facilities management, etc.) in support of the janitorial function. (As mentioned previously, contracting out of non-janitorial functions that make use of the same support overhead would have the same effect.) The total costs to be avoided in this scenario will be slightly in excess of $6 million or $3.55 per square feet. The contractor's bid is $3.25 per square feet. Thus, contracting out will result in avoiding 30 cents per square feet, or $507,450.

Table 4

|

SCENARIO TWO: COMPARISON OF FULLY ALLOCATED COSTS AND AVOIDABLE COSTS |

||

|

Cost Item |

Fully Allocated Costs |

Avoidable Costs |

|

Direct Costs |

|

|

|

Service Provision Salaries and wages |

$2,145,817 |

$2,145,817 |

|

Employee benefits (@ 21.25%) |

$455,986 |

$455,986 |

|

Service and Supplies |

$950,000 |

$950,000 |

|

Subtotal |

$3,551,803 |

$3,551,803 |

|

Division Overhead |

|

|

|

Salaries and Wages |

$1,017,745 |

$1,017,745 |

|

Employee Benefits |

$216,271 |

$216,271 |

|

Subtotal |

$1,234,016 |

$1,234,016 |

|

Branch Overhead |

|

|

|

Salaries and Wages |

$219,506 |

$219,506 |

|

Employee Benefits |

$46,645 |

$46,645 |

|

Subtotal |

$266,151 |

$266,151 |

|

Departmental Overhead (@22.259%) |

$753,057 |

$600,000 |

|

Countrywide Overhead (@13.958%) |

$472,209 |

$350,000 |

|

Total Cost |

$46,697 |

$26,250 |

|

Cost per square foot |

$3.71 |

$3.55 |

The cost comparison analysis between in-house and contract service delivery is still not complete. Contract administration costs and one-time conversions costs must be added and off-setting revenues subtracted to arrive at the total cost of contract service delivery. Even after these costs are included in the analysis, however, this scenario would likely result in the county saving several hundred thousand dollars by contracting out all Janitorial services.

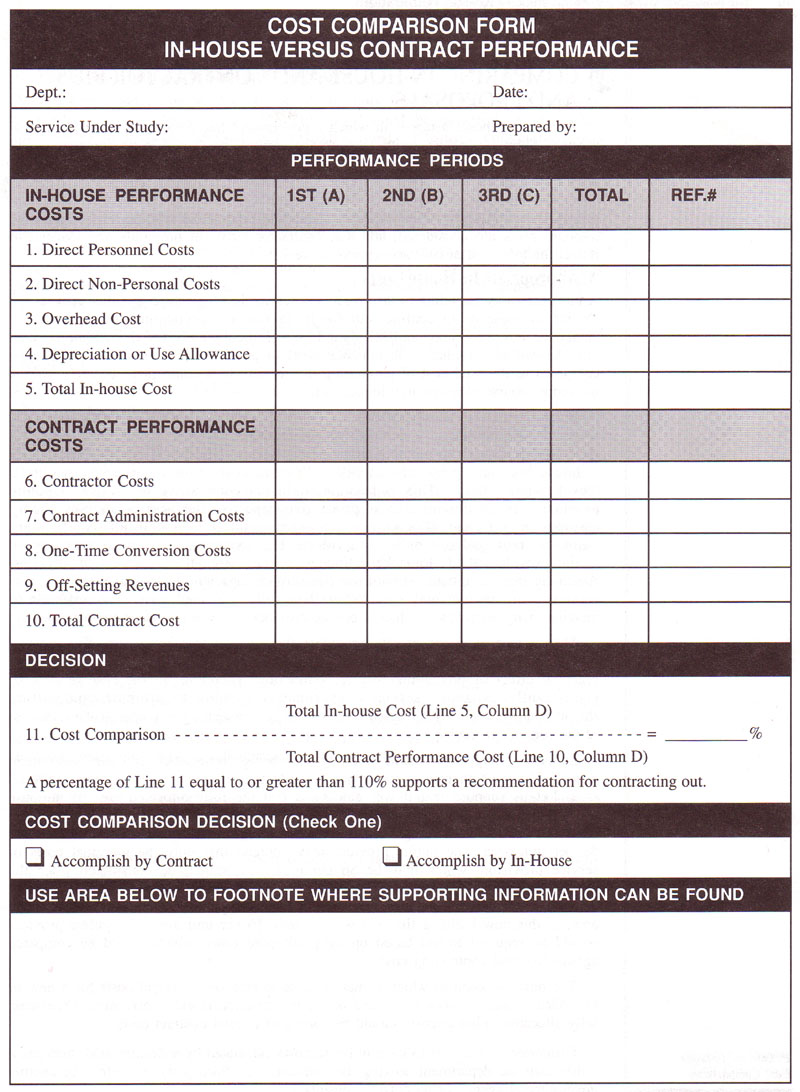

A number of state and local governments have developed cost comparison formats to assist officials in presenting a summary of cost comparison data between in-house and contract service delivery. The City of Cincinnati, Ohio has developed one of the more comprehensive formats.[31] A modified version of the City of Cincinnati's cost comparison format appears on the following page.

While the cost-comparison format is basically self explanatory, three aspects do warrant special mention: 1) avoidable costs; 2) performance periods; and 3) the cost-comparison ratio.

A. Avoidable Costs

Only avoidable costs are entered in the various categories under in-house service delivery costs. The cost-comparison format assumes that the fully allocated costs of in-house service delivery have already been determined.

B. Performance Periods

The format provides space to include cost-comparison data for up to three performance periods. A performance period is one fiscal year, or a portion thereof if a target service is being considered for contracting out in the middle of a fiscal year. Several reasons exist for carrying out the cost comparison over multiple performance periods. For example, the total cost savings associated with contracting out may not be realized in the initial performance period due to such factors as large contractor start-up costs for facilities or equipment and/or significant government one-time conversion costs. In both instances, these costs should be amortized over multiple performance periods. Another reason is that short-ten-n cost comparisons (i.e., one performance period) may fail to account for possible relevant future changes in the costs of labor, materials, transportation, etc.[32]

C. The Cost-Comparison Ratio

The cost-comparison ratio (see line 11 of the cost-comparison format) is the

ratio between the total cost of in-house service delivery and the total cost of contract service delivery. The purpose of the cost-comparison ratio is to establish a cost-savings threshold that justifies a decision to change the mode of service delivery. While theoretically justifiable on the basis of any cost savings, many government agencies have adopted the policy that the cost savings should be sufficient to warrant the organizational upheaval associated with the changeover. The federal government, the state of Texas, and the City of Cincinnati, Ohio have all established a threshold level of 10 percent when considering a change from in-house to contract service delivery.[33]

What about those instances in which a government has decided to undertake a new service? Should a public entity take on the service, or should it be contracted out? Often, an existing public department will seek to perform the service and bid against private contractors. This form of competition between the public and private sector is becoming increasingly common.[34] Making valid cost comparisons between bids and proposals submitted by in-house departments and contractors requires that appropriate in-house costs are considered, and that contractor bids and proposals are adjusted to reflect the total cost of contract service delivery.

A. Appropriate In-House Costs

A business entity intending to take on a new service has the choice to either provide the service in-house or to contract out for it. In business accounting this is termed a "make or buy" decision, and standard business theory calls for the additional cost (also known as marginal or incremental cost) of providing the service in-house to be compared to the total cost of purchasing the service. In a competitive business, this is the proper course of action to minimize total cost.

But what is sound business practice is not necessarily prudent for government entities, which do not operate in a competitive environment. For this reason, state and local governments desiring to promote public-private-sector competition may find that basing in-house bids and proposals on fully allocated costs comes closer to creating a "level playing field." This is because, unlike a competitive enterprise, a public provider often maintains excess productive capacity. Business accounting theory assumes an efficient allocation of resources, and this assumption is often not valid for monopolistic public providers. The existence of surplus capacity in public providers tends to make estimates of the marginal cost unrealistically low. Assuming that an in-house department has surplus capacity and bids to perform a new service using incremental cost rather than fully allocated cost, it is difficult to imagine many scenarios in which a private-provider cost would appear competitive.

This is true even for private providers that are far less expensive. The practice of comparing in-house marginal costs with the total cost of contracting has the practical effect of precluding private contracting. Therefore, in the case of new or significantly expanded service, governments wishing to promote competition should compare the fully allocated costs of the government agency against the total cost of the contracted service.

Suppose a large new public building was being constructed, and the government was deciding whether to contract out for maintenance or to expand their janitorial staff. Let us suppose that it was calculated that the fully allocated cost of in-house provision in those buildings currently serviced came to $10 per unit area, and that the total cost of contracting for services, including contract administration, came to $8 per unit area. The public provider may contend that only the marginal costs of service provision, which may be $6 per unit area, should be considered since the additional service will not increase overhead. In essence, this argument is a claim that while the cost for janitorial services in all other public buildings is $10 per unit area, in this new building the cost will be only $6 per unit area. The public provider should be required to bid based on fully allocated costs, which should be compared against the total contracting costs.

The only occasion in which it makes sense to consider marginal costs for a new or expanded service is when the extent of the privatization is extremely small. Otherwise, fully allocated in-house costs should be compared to total contract costs.

Furthermore, it is best to have in-house costs calculated by a disinterested third party, rather than the department seeking the contract. This third party can either be another governmental agency or an outside consultant.

B. Adjusting Contractor Bids and Proposals

A contractor's bid or proposal costs, of course, only represent part of the total cost of contract-service delivery. A contractor's bid must be adjusted (as described previously) to include: contract administration costs, one-time conversion costs and any off-setting revenues.

Cost is often an important consideration in the privatization decision, and officials should be aware of the true cost of both in-house and contracted services. Computing the cost of service delivery is a complex accounting endeavor, and there is no "cookbook" method that will eliminate all subjective evaluations. The guidelines presented in this paper, however, present accepted practices that will help ensure that all relevant costs are considered.

Once costs are computed, how should they be used in evaluating whether or not to privatize? Depending on the information sought, different sets of costs should be considered.

TOTAL CONTRACTOR COSTS

These are appropriate in assessing the cost of contracted service, and should include contract administration and monitoring.

FULLY ALLOCATED COSTS

These costs are appropriate in evaluating the operating efficiency of a public provider. Comparing the fully allocated cost of the in-house provider with the anticipated total cost of contracting is useful in assessing their relative efficiency. If the fully allocated costs of the public provider are more than ten percent greater than for a private contractor, that service merits further consideration for privatization. Fully allocated costs, however, are not the correct measure for estimating the likely cost savings through privatization, as fully allocated costs tend to overestimate savings, especially in the short term.

AVOIDABLE COSTS

These should be used to estimate cost savings. Comparing the avoidable in-house costs with the total cost of contracted services provides the best assessment of the likely cost savings achievable through privatization. Precisely which costs are considered varies with the time given the government provider to reallocate resources. Some costs that will not be avoidable in the first year will be avoidable three or five years later. In the short term, avoidable costs may be close to marginal costs. In many cases, in the long term, avoidable costs should approach fully allocated costs.

Whether a particular cost is avoidable or not also depends on the determination of the public entity to reallocate resources in order to hold down costs. Furthermore, a cost may or may not be avoidable depending on the extent of the privatization and legal constraints on the public provider.

When the privatization in question concerns a new or expanded function, fully allocated in-house costs should be compared to expected total contract costs.

Dr. Lawrence L. Martin is associate professor of public administration at Florida Atlantic University in Boca Raton. Dr. Martin holds the bachelor's, master's and Ph.D. degrees from Arizona State University at Tempe and an M.I.M. degree from the American Graduate School of International Management in Glendale, Arizona. He is co-author/co-editor of three books: Purchase of Service Contracting (Sage, 1987), Designing and Managing Programs (Sage, 1990), and Handbook of Public Budgeting and Financial Management (Marcel-Dekker, 1992). He is also the author/co-author of over 30 articles and book chapters dealing with privatization and state and local government. Before assuming his current academic position, Dr. Martin worked for 15 years as a state and local government manager in Arizona.

1. Irwin T. David, "Privatization in America," in The Municipal Yearbook 1988 (Washington, D.C.: The International City Management Association, 1988), pp. 43-55; David Seader, "Privatization and America's Cities," Public Management, 68 (December 1986), p. 7.

2. State Government Privatization 1992, Apogee Research, Inc., 1992; Privatization 1991, Fifth Annual Report on Privatization, Reason Foundation, 1991; Privatization In America, Touche Ross and Company, 1987,

3. E. S. Savas, Privatization-The Key to Better Government (Catham, NJ: Catham House Publishers, 1987), p. 259.

4. Lawrence L. Martin, "A Proposed Methodology for Comparing the Costs of Government versus Contract Service Delivery," in The Municipal Yearbook 1992 (Washington, D.C.:, International City/ County Management Association, 1992), pp. 12-15; Joseph T. Kelley, Costing Government Services: A Guide for Decision Making (Washington, D.C.: Government Finance Officers Association, 1984), p. 103; Synopsis of GAO Reports Involving Contracting Out Under OMB Circular A-76, (Washington, D.C.: U. S. General Accounting Office, 1980), p. 5.

5. Jonathan Richmond, "The Costs of Contracted Service: An Assessment of Assessments," MIT Center for Transportation Studies, July 20, 1992.

6. Findings of a National Survey of Local Government Set-vice Contracting Practices (Atlanta, GA: Mercer/Slavin, Inc., 1987), p. 2, pp. 13-14.

7. Fully Allocated Cost Analysis: Guidelines for Public Transit Providers (Washington, D.C.: Price Waterhouse, 1987), p. 1.

8. Ibid., 1987.

9. David E. Ammons, Administrative Analysis for Local Governments (Athens,

GA: University of Georgia, Carl Vincent Institute, 1991), p. 88.

10. In the step-down method, the costs of support-service departments (e.g., finance, procurement, facilities management, etc.) are allocated to user departments (i.e. line units that directly service citizens) based upon the actual amount of support services received during some prior time period or the anticipated amount of support service to be received in some future time period. For a more detailed explanation of the step-down method see: Guide To Implement the Competitive Cost Review Program (Austin: Office of the State Auditor, State of Texas, 1989), pp. 28-3 1.

11. Peter M. Kettner and Lawrence L. Martin. Purchase of Service Contracting (Beverly Hills: Sage Publications, 1987).

12. John A. Rehfuss, "Contracting Out and Accountability in State and Local Government: The Importance of Contract Monitoring." State & Local Government Review 22 (1990), pp. 44-48.

13. This is the position take by the U.S. General Accounting Office and the U.S. Office of Management & Budget. See U.S. General Accounting Office, 1985 and U.S. Office of Management & Budget (OMB), Supplement to OMB Circular No. A-76 (Washington, D.C.: U.S. Government Printing Office, 1985).

14. Barbara J. Stevens, Delivering Municipal Services Efficiently: A Comparison of Municipal and Private Service Delivery (Washington, D.C.: U.S. Department of Housing & Urban Development, 1984), p. 6.

15. Privatization Study Handbook, City of Cincinnati, Office of Research, Evaluation, and Budget, 1985, p. 17.

The City of Cincinnati may use the relative low figure of 4 percent of contractor costs because at one time this approach was recommended by the federal Office of Management & Budget (OMB). However, OMB changed this policy in 1985 and now recommends the use of a staffing formula (see Table 1).

16. E. S. Savas, Privatization: The Key to Better Government (Catham, NJ: Catham House, 1987), p. 260.

17. John A. Rehfuss, Contracting Out in Government (San Francisco: Jossey-Bass, 1989), p. 96.

18. Ibid., p. 45.

19. The author has argued this position elsewhere. See Martin, 1992.

20. U. S. Office of Management & Budget, 1985, pp. IV-37.

21. Harry Hatry, Kenneth P. Voytek, and Allen E. Holmes, Building Innovation Into Program Reviews (Washington, D.C.: The Urban Institute, 1989), p. 76.

22. Office of the State Auditor, State of Texas, 1989, p. 32.

23. These cost categories were developed by the City of Cincinnati. See City of Cincinnati, 1985, p. 17.

24. Stevens, 1984.

25. Office of the State Auditor, State of Texas, 1989, p. 35.

26. Donald W. Dobler, David N. Burt and Lamar Lee, Purchasing And Materials Management (New York: McGraw-Hill, 1990), p. 156.

27. For example: John Tepper Martin, ed. Contracting Municipal Services: A Guide for Purchase from the Private Sector (New York: John Wiley & Sons, 1984); Kelley, 1984; Rehfuss, 1989; and Dobler, Burt and Lee, 1991.

28. For example: Privatization Assessment Workbook, Colorado State Auditor's Office, 1989; City of Cincinnati, 1985; Office of the State Auditor, State of Texas, 1989.

29. Ray H. Garrison, Managerial Accounting, 6 ed. (Homewood, III: Richard D. Irwin. 1991).

30. Jonathan Richmond, "The Costs of Contracted Service: An Assessment of Assessments," MIT Center for Transportation Studies, July 20, 1992.

31. City of Cincinnati, 1985, p. 6.

32. Dobler, Burt, and Lee, 1990, p. 156.

33. See U.S. General Accounting Office, 1985 and U.S. Office of Management & Budget (OMB), Supplement to OMB Circular No. A-76 (Washington, D.C.: U.S. Government Printing Office, 1985). Guide To Implement the Competitive Cost Review Program (Austin: Office of the State Auditor, State of Texas, 1989), pp. 28-31. Privatization Study Handbook, City of Cincinnati, Office of Research, Evaluation, and Budget, 1985, p. 17.

34. David Osborn and Ted Gaebler, Reinventing Government (Reading, MA: Addison-Wesley Publishing Co., 1992), pp. 76-78.