Ending the regional monopoly structure in the generation of electricity was intended to provide customers with lower rates and improved service quality, while also increasing generating capacity for electricity in the state. But attempts are underway to reverse the course of this restructuring.

The Michigan Legislature in May 2000 approved the introduction of competition in retail power supplies. Ending the regional monopoly structure in the generation of electricity was intended to provide customers with lower rates and improved service quality, while also increasing generating capacity for electricity in the state. But attempts are underway to reverse the course of this restructuring.

In numerous radio and television ads, a coalition headed by DTE Energy is warning the public of a power market meltdown if Michigan fails to alter key provisions of the electricity choice program. According to DTE Chairman and CEO Anthony Earley, Jr., “If left unattended, we believe [Michigan’s Electric Choice Program] will lead to a California-like energy crisis. I am referring specifically to significant rate increases for residential and small commercial customers, a financially crippled Detroit Edison, potential job losses in Michigan’s electric industry and service and reliability problems.”[1]

Competitive energy prices and a reliable electrical grid are indeed crucial elements of economic growth and job creation in Michigan. It is incumbent on lawmakers, the media and the public to carefully consider whether a policy shift is warranted. Based on our analysis of state law and market conditions, we conclude that restricting competition in electricity supply would actually harm rather than benefit Michigan consumers and the businesses that employ them. However, some regulatory reforms could improve the system.

The provision of electricity was once regarded as a “natural monopoly.” The theory of “natural monopoly,” now largely questioned, presumes that building competing electricity infrastructure is too costly to justify. Supposedly, the customer base and price of electricity are insufficient to recover the capital investment required to construct a competing power plant. Consequently, the state bestowed regional monopoly status on select utilities, and imposed price controls and other regulations to temper the market power of the chosen monopolists.

For decades, Michigan has been divided into service territories with a specific utility designated by the state to generate electricity, transmit the power to the grid and distribute it to customers. Detroit Edison and Consumers Energy, between them, have long serviced 90 percent of the market statewide. The Michigan Public Service Commission regulates rates and service standards. In the late-1990s, in concert with a deregulatory trend nationwide, Michigan lawmakers began mulling reform proposals. Electricity rates in the state were consistently higher than the Midwest average, putting Michigan at a competitive disadvantage in retaining and attracting new industries. Lawmakers sought to open the market to competing suppliers of electricity and to promote investment in new, more efficient power plants.

The Legislature authorized utility restructuring in Public Act 141 of 2000, the “Customer Choice and Electricity Reliability Act.” The new law effectively “unbundled” power generation, transmission and distribution as distinct services, and allowed alternative power suppliers both inside and outside the state to consign electricity to the existing power grid and thus compete with Detroit Edison and Consumers Energy for industrial, commercial and residential customers.

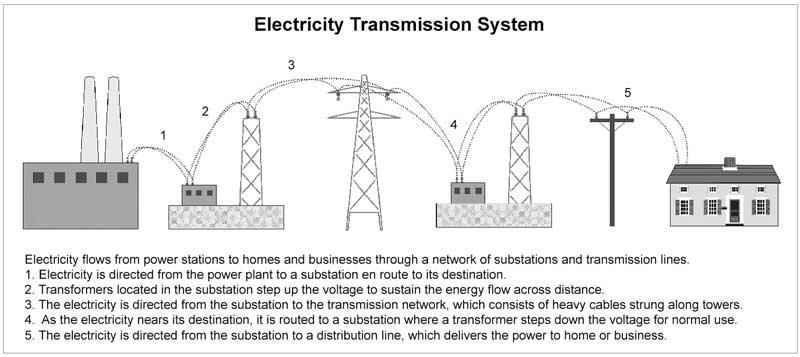

As a practical matter, power suppliers cannot direct the electricity they produce to specific customers. But the total volume of power they add to the transmission grid represents the load specified by their customer contracts.

To comply with changes in federal and state law, both Consumers Energy and Detroit Edison in 2002 sold their transmission facilities to an “independent system operator.” Independent management of these transmission assets is being phased in. The Midwest Independent Transmission System Operator, Inc., will ultimately oversee an electricity network traversing 15 states, from Pennsylvania to Montana, and including Manitoba, Canada.

Monopoly status carried both advantages and obligations. With government protection from competition, Detroit Edison and Consumers Energy could depend on a secure share of the market. But they were also required to maintain at all times enough power capacity to serve the peak demands of all customers in their regions. In many instances, this required the utilities to negotiate long-term contracts with other power suppliers without knowing what the future market price of electricity would be months or years into the future.

Moreover, the utilities invested capital in infrastructure based on the power demands forecast for a fixed share of the market.

When the debate over restructuring commenced, utility officials and shareholders were particularly concerned that a loss of customers to competitive power suppliers would deprive them of revenue needed to recoup investments that had been made with the explicit approval of the state, and for which a return was guaranteed through regulated rates paid by a captive customer base.

With this in mind, lawmakers sought to ease the transition to competition for Detroit Edison and Consumers Energy. Public Act 141 of 2000 authorized the Public Service Commission to analyze which utility investments were made to fulfill regulatory obligations. If the utilities’ customer base does not generate sufficient revenue to recoup the regulated investments, the commission is authorized to impose charges to recover so-called “stranded costs” to be paid monthly by every ratepayer, regardless of supplier.

The issue of “stranded costs” continues to arouse considerable debate. Opponents contend that power plants are actually valuable assets for which there continues to be market demand. The utilities’ debts, they argue, can be recovered through the sale of electricity on the spot market or by private contracts, or by outright sale of the infrastructure. Moreover, encumbering all ratepayers with a share of “stranded costs” artificially inflates the price of electricity in Michigan and, therefore, diminishes the benefits of competition.

Nonetheless, stranded cost recovery was the political price paid to initiate utility restructuring. The two incumbent utilities are also guaranteed compensation for costs associated with transforming the power networks and billing systems to facilitate competition.

Michigan ratepayers are liable for a total of $2.2 billion in utility debt recovery. The bulk of the tab — $1.77 billion — represents the dollar value of securities sold by Detroit Edison in order to refinance outstanding debt. This process of refinancing, called “securitization,” enabled the utility to obtain an influx of cash at very attractive interest rates because debt securities are exempt from federal income taxes. They also carry less risk to investors because a revenue stream for repayment was secured by the state.

The recovery of utilities’ costs related to implementing restructuring, such as adapting billing systems to competition, has prompted litigation. But the Michigan Court of Appeals in April ruled that the Public Service Commission had improperly delayed consideration of this cost recovery, and rightly ordered the state to move ahead with compensation.

Michigan, like other states, is in a transition phase of utility restructuring, with competition on an upswing. The number of alternative energy suppliers now serving customers increased by 10 in 2003, bringing the statewide total to 26. The number of customers choosing alternative suppliers nearly doubled in 2003, to more than 13,000 and 2,859 megawatts of electricity.[2]

The economic benefits of competition are tangible. “By allowing small businesses to choose lower-cost electric providers, this law has preserved the equivalent of 20,000 jobs since it was enacted four years ago,” said Rob Fowler, president and CEO of the Small Business Association of Michigan.[3]

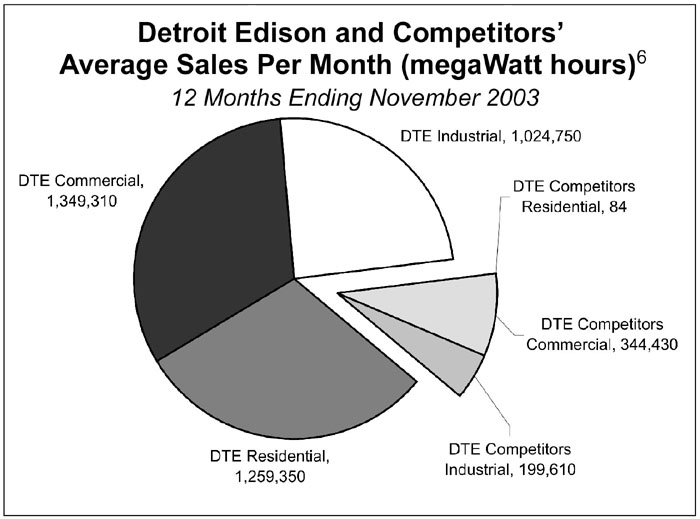

In the Detroit Edison service area, alternative power suppliers now account for about 20 percent of commercial sales and 16 percent of industrial sales. Over the past 12 months, the number of customers opting for alternative suppliers grew by 100 percent, while the amount of competing supply of electricity grew by 60 percent.[4]

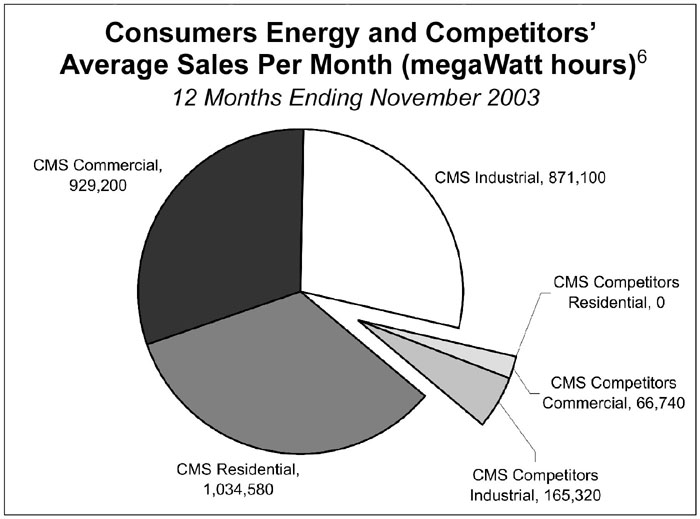

In the Consumers Energy territory, alternative power suppliers account for about 7 percent of commercial sales and 16 percent of industrial sales. Over the past 12 months, the number of customers opting for alternative suppliers grew by 75 percent, while the amount of competing supply of power grew by 47 percent.[5]

Very few residential customers have opted for a competing supplier. This is not surprising, however. Lawmakers in 2000 mandated a 5 percent rate cut, which reduced customers’ incentive to seek service alternatives. More important, residential rates have been kept artificially low by the imposition of higher rates on commercial and industrial customers. Meanwhile, new entrants in the power market have targeted their marketing efforts on large-volume purchasers, the better to gain a foothold in the market.

Residential customers do benefit from restructuring, however. Competition exerts downward pressure on electricity rates, which helps to limit increases in the prices of products and services.

Critics of competition claim that new entrants are “cherry picking” high-volume customers. But targeting the most profitable customers is standard strategy for new competitors in any market. For example, the most successful start-up airlines, such as JetBlue and Southwest, first offered service on high-volume routes between major cities before expanding into smaller markets. Similarly, satellite television services like DirecTV were launched in the mid-1990s as high-end services before being marketed as a standard alternative to cable.

There are significant rate variations among power suppliers. Some Michigan manufacturers report savings of 15 percent to 20 percent from opting for alternative service providers. Michigan public schools and universities are likewise turning to new suppliers to cut energy costs.

More important, perhaps, is the investment in new generating capacity in Michigan spurred by Public Act 141. The Public Service Commission has identified at least 15 new facilities in the planning stages or under construction that, if completed, would add nearly 12,000 megawatts of new generating capacity in the state — or about four times the amount currently provided by alternative suppliers.[8]

Based on the increased competition in power supply, utility restructuring in Michigan is progressing on course. To claim failure now would be unwarranted considering the consumer and economic benefits that restructuring has produced.

DTE Energy is a principal architect of the campaign to alter Michigan’s electric choice program. The company and its allies have organized as the “CLEAR Coalition” (Citizens for Long-term Energy Affordability and Reliability). Officials of Consumers Energy also back reform, but prefer action by the Public Service Commission to that of the Legislature. Reopening the state’s controlling statute could invite more extensive revisions as well as intensify political risks.

Some of the rhetoric employed by CLEAR is clearly misleading. For example, CLEAR claims that Michigan is heading toward an energy crisis as occured in California. But the collapse of California’s energy market two years ago was largely a consequence of too much government interference rather than too little regulation, and few, if any, of the same contributing factors exist in Michigan.

In the case of California, regulators forced utilities to divest all generating capacity, and required them to purchase all power from wholesale suppliers and brokers such as Enron. Regulators also prohibited California utilities from negotiating long-term contracts that would ensure a stable supply of electricity at lower, fixed rates. Compounding the problem were price controls that forced utilities to sell power at retail rates far below the prices paid for the electricity on the wholesale market.

It was, in short, a recipe for market collapse.

But Michigan runs no such risk. Indeed, Mr. Earley assured shareholders in 2001 that Michigan was well protected against a California-type crisis. “I don’t anticipate California-like problems here,” the DTE chairman said. “The drafters of our legislation paid attention to the early warning signs in California and established safeguards that will provide for an orderly transition to competition.”[9]

The incentive of incumbent utilities to alter Michigan’s utility restructuring is rather basic: Incumbent utilities prefer to eliminate competition through regulation rather than have to fight in the marketplace to retain customers.

According to DTE officials, the company has lost to competitors some 12 percent of its market share in the past year. The company is forecasting continued erosion of market share by year’s end — down by 18 percent of last year’s load.[10]

In a series of ominous public ads, the CLEAR Coalition is warning that “plummeting” revenues could undermine power plant maintenance and thus “lead to more outages, reduced ability to restore customers after storms and other reliability issues.”[11]

But such assertions are questionable. There is no evidence that overall market demand for power has dropped. On the contrary, economic growth increases demand for electricity. Incumbent utilities, therefore, can maintain market share by improving efficiency, which would translate into more competitive rates with which to lure customers.

Detroit Edison’s sales were indeed $120 million lower in 2003 as compared to 2002. But the difference cannot be attributed solely to the advent of competition. The summer of 2003 was unusually cool, which cut deeply into electricity demand for air conditioners. Significant sales also were lost during the blackout in August 2003, which was unrelated to utility restructuring — notwithstanding claims to the contrary by critics of an open energy market.

By market standards, DTE Energy remains strong. The price of company stock has risen more than 30 percent since January 2000. Moreover, DTE’s earnings have increased from 92 cents per share in the first quarter of 2003 to $1.09 per share in the first quarter of 2004.[12] Shareholders also have enjoyed strong dividends this year.[13]

To the extent that unnecessary regulation undermines the utility’s competitiveness, reform is needed. But the company can still use excess capacity to generate power for sale on the spot market, or to supply privately negotiated contracts.

The regulatory bailout initially advocated by CLEAR would have restricted choice to large industrial and commercial customers, and forced small and medium-sized firms as well as Michigan families to once again become captives of a utility monopoly.

Such action, however, is unwarranted.

The Legislature has begun consideration of a package of six bills introduced on July 1 to amend the electric choice program. Unfortunately, the proposed legislation, while more modest than the reforms advocated by CLEAR, is flawed.

The package includes legislation that would require all electricity suppliers to maintain a “reserve” generating capacity of 15 percent. This proposal appears to be an attempt to “level the playing field” for the incumbent utilities by imposing on all suppliers the reserve requirements currently applied only to the former monopolies.

The proposed 15-percent reserve requirement is wholly arbitrary, however, and would significantly increase the cost of market entry for competitors — thereby thwarting the purpose of restructuring. A more rational approach would be to eliminate government reserve requirements altogether. Power generators have every incentive to maintain adequate electricity supplies for their customers — especially in a competitive market.

Another element of the proposed legislation would require all power suppliers to contribute to a subsidy fund for low-income customers. But such a requirement would effectively constitute a new tax, in addition to the substantial subsidy programs that currently exist. If lawmakers deem energy assistance to be a worthy social goal, payments should be allocated from the General Fund rather than borne by utilities and ratepayers.

Also proposed is a new method of calculating the amount consumers are forced to pay for the supposed “stranded costs” of incumbent utilities. The proposed calculation would eliminate the annual accounting of cost savings realized by the incumbents through improved efficiencies. This proposal is misguided because consumers would pay higher “stranded costs,” while the incumbent utilities would have less incentive to operate more efficiently. A related proposal to extend to 10 years the period in which transition charges are levied on all ratepayers should also be rejected as unnecessarily costly and anti-competitive.

The legislation also contains a provision to create a new energy subsidy, ranging between 10 percent and 20 percent, for K-12 public schools. But as noted earlier, schools have already realized energy savings by contracting with alternative electricity suppliers. The cost of a new subsidy would be borne by all ratepayers, but there is no justification to impose a new school energy tax on Michigan citizens.

A proposal to provide low-interest financing to the incumbent utilities for plant improvements is also unwarranted. Every new charge levied on ratepayers reduces the cost-savings that can be realized through competition. This proposed subsidy thus undermines the viability of competing suppliers by artificially increasing their rates.

One proposal does merit serious consideration. It would eliminate the current requirement that incumbent utilities must reconnect customers who discontinue service with an alternative supplier at the regulated rate. This change would reduce the burden on incumbent utilities of maintaining unused capacity, or of having to buy more costly power on the spot market.

The goal of a competitive market will not be fulfilled until the vestiges of monopoly regulation are eliminated. As with any product or service, electricity customers must weigh the benefits and risks of their choices. If they are dissatisfied for any reason with their power supplier, they remain free to shop for another. This consumer freedom is precisely the disciplinary force that will keep power suppliers in line.

In the campaign to restrict competition in electricity supply, proponents have raised some legitimate issues that deserve consideration. None warrant new limits on competition, but some changes could improve Michigan’s power market.

A key complaint among the incumbent utilities is the requirement that they alone must act as the suppliers of last resort. Detroit Edison and Consumers Energy, for example, must reconnect customers at the regulated rate should they opt to leave a competing service provider. This requirement constitutes a competitive disadvantage because incumbent utilities must underwrite the costs of maintaining supply for phantom customers or purchasing more costly power that regulated rates would not cover.

Incumbent utilities should not be forced to provide service to every household or business at standard cost. The choice to live in a remote area involves trade-offs that ought not to be subsidized by DTE, Consumers Energy and their ratepayers. Demand for more affordable power supplies in remote locations would undoubtedly stimulate R&D in cost-effective options.

Incumbent utilities are also required to provide home heating assistance programs. But if electricity welfare is indeed a worthy social goal, the subsidies should be apportioned from the General Fund rather than imposed selectively. Nor is there a lack of assistance from public sources. Michigan receives some $97 million in federal funds for home heating assistance programs, and contributes an additional $27 million to such programs. The state offers a home heating tax credit, while the Family Independence Agency provides emergency heating assistance.

The one element of P.A. 141 that deserves repeal is the imposition of price caps that locked rates at 5 percent below 2000 levels until 2006. Price controls inhibit competition, innovation and efficiency by artificially limiting returns on investment. Absent price controls, competition exerts downward pressure on rates.

The campaign to alter Michigan’s utility restructuring has created uncertainty in the marketplace. Investors are understandably reluctant to risk their capital where the rules of engagement appear to be in flux. For this reason alone, the Legislature should only undertake reforms that stimulate competition and attract investment, and without delay. Considering the benefits to date of competition in power supply — and the promise of more to come — lawmakers would do well to summarily reject any bid for government protection from competition and focus instead on further de regulation of the electricity market. In the campaign to restrict competition in electricity supply, proponents have raised some legitimate issues that deserve consideration. None warrant new limits on competition, but some changes could improve Michigan’s power market.

DTE Energy, "A Message from the Chairman," http://my.dteenergy.com/main/choiceReform.do.

Michigan Public Service Commission, "Michigan Energy Appraisal, Summer 2004," May 2004.

Online Digest of the Small Business Association of Michigan, "Small Businesses say electric choice saves money and jobs," Feb. 10, 2004. http://www.sbam.org/sbam0304/resource/digest/features/021004.html.

Michigan Public Service Commission, "Status of Electric Competition in Michigan," April 2004.

Ibid.

Energy Information Agency, "Electric Power Monthly," March 2004.

Michigan Public Service Commission Utility Rate Books, available at http://www.cis.state.mi.us/mpsc/electric/download/rates1.pdf. The ranges represent differences in average rates for different sizes of customers.

Michigan Public Service Commission, "Status of Electric Competition in Michigan," February 1, 2004.

Anthony F. Earley, Jr., Chairman of the Board and Chief Executive Officer, "DTE Energy Annual Report for 2000," dated January 31, 2001, p.5.

DTE Energy Press Releases, "PA 141 is Top Priority, DTE Energy CEO Tells Shareholders," April 29, 2004.

DTE Energy, "A Message From the Chairman," http://my.dteenergy.com/main/choiceReform.do.

Reuters News Service, "DTE Energy First Quarter Profits Rises 20%," April 28, 2004, http://biz.yahoo.com/rc/040428/utilities_dte_earns_2.html.

Reuters News Service, "DTE Energy Declares Dividend" March 9, 2004; Press Release, "DTE Energy Declares Dividend," May 14, 2004.

Theodore Bolema is an adjunct scholar of the Mackinac Center for Public Policy and is on the faculty of the Finance and Law Department of Central Michigan University’s College of Business Administration. He holds a Ph.D. in Economics from Michigan State University, and a J.D. from the University of Michigan Law School.