In 1993, Michigan voters were asked to consider a plan that would cut property taxes and cap property assessments, raise the sales tax, and establish a $4,800 per-pupil guarantee for the public schools. "Proposal A" was defeated, but not without intensive debate in which this study figured prominently. The report identifies both pros and cons of "A," including independent, in-depth analysis of its likely impact on the state budget, schools, and property owners. Although "A" is now consigned to the history books, this study is a useful tool for understanding school finance, the economics of property taxation, and related constitutional questions. 40 pages.

"A"Would Cut Total Taxes Sharply in 1993, By Smaller Amounts in the Future

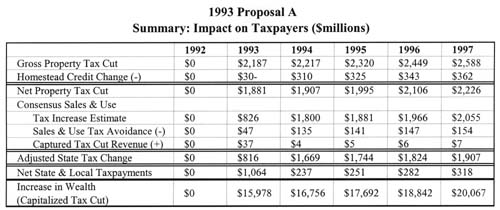

An economic model developed by the author for the Mackinac Center indicates that Proposal "A" would save Michigan taxpayers approximately $1.1 billion in net state and local taxes in the current year, and between $230 and $320 million in each of the next four years. This model relies on assumptions independent from those used by government agencies, incorporates dynamic behavior on the part of both the private and public sectors, and does not include tax savings measures proposed alongside "A" but not included in it. See page 21 and Appendix III on page 37.

"A" Would Increase Homeowners' Equity by $16 Billion

The permanent reduction in property taxes would significantly increase the value of property since the lower cost of holding the asset would increase its market value. This increase in homeowner's equity would add approximately $16 billion to the wealth of Michigan citizens in the current year, the equivalent of $1775 for even man, woman, and child. This real spendable wealth would be convertible to cash through mortgage refinancing, home equity loans, or sales of property. See page 13, and Appendix II on page 34.

Tax Cuts and Wealth Increases Would Add Jobs Economic Growth

The substantial net tax reduction in the current year, the smaller tax reduction in future years and the increase in wealth of Michigan residents would stimulate Michigan's economy. The additional disposable income would generate increased private sector jobs in the state and the reduction in property taxes would encourage investment in plant and equipment among Michigan industries. While estimates of "new jobs" from government programs are notoriously exaggerated, the benefits from a reduction in state and local tax burdens – allowing the private sector to create the jobs where most needed – are proven. See page 30.

"Cap" on Assessments Introduces Nonuniformity, But Avoids Assessment Shock

The cap on annual assessment changes would make property tax burdens much more predictable, but at the cost of introducing nonuniformity, since owners of similar parcels would often face different tax burdens. The current assessment system fails at providing due process, and "A" would substitute deliberate, but predictable and tax-limiting, nonuniformity. See page 8.

State Would "Lose" Over $130 Million a Year to Sales Tax Avoidance

The economic model developed for this study recognizes that taxpayers avoid paying taxes when possible. Using conservative estimates of tax avoidance behavior, the model predicts that a 50% increase in the sales and use tax rates would result in a 5% drop in taxed transactions. Tax avoidance results in about $135 million less sales and use tax revenue in 1994, growing to $154 million by 1997, than the consensus state government estimate. The sharply increased sales and use tax rates would result in more catalog sales from out-of-state vendors, purchases of big-ticket items in advance of the effective date, and reduced incentives to travel and purchase goods in Michigan. See page 21 and Appendix III on page 37.

Watch for Legislative Weakening of Millage Limits

The constitutional amendment is clearly intended to permanently limit property taxes by limiting school operating millage rates. "Operating" has a long history of meaning all purposes other than millage to repay voter-approved debt. However, the amendment allows the legislature to define "operating," and a draft bill excluded "operating deficit" millage. Such an exclusion, if it survived court challenge, would open the door to school property tax increases beyond the 27-mill limit clearly stated in the amendment.

Since future judicial interpretation of this amendment willhinge on for what the "common man" thought he was voting, voters must pay close attention to any statutes enacted prior to the election date that define its tax limitations. See page 6.

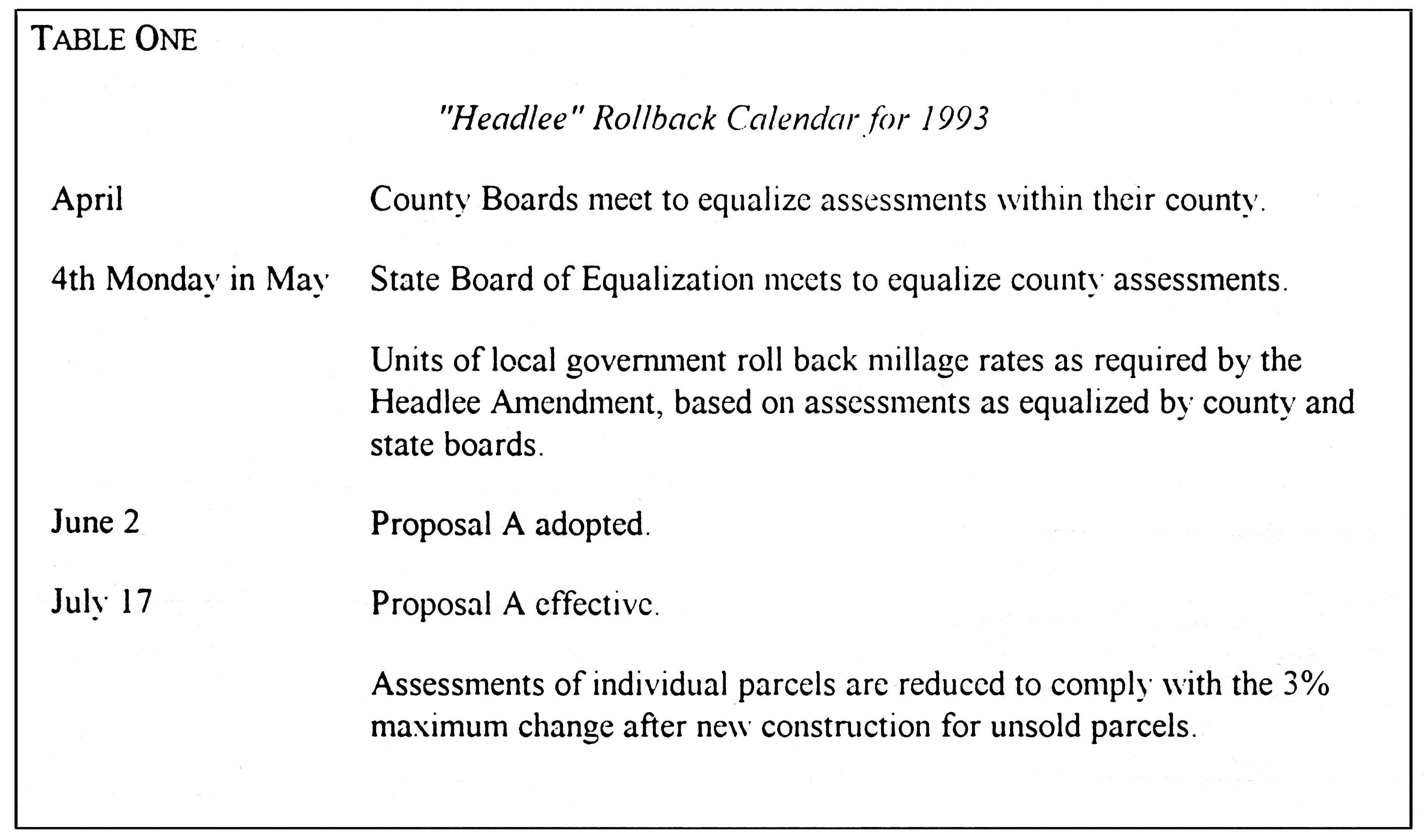

"Double Rollback" on Millage Rates and Assessments Required in 1993

Under the current Constitution and law, the assessment increases mailed to taxpayers in the spring must cause "Headlee " rollbacks in millage rates immediately after the fourth Monday in May – before the election date for Proposal "A." If "A" is adopted. then the new constitution would require further rollbacks in assessment increases that exceeded 3%, resulting in a "double rollback" for 1993. The "Headlee" millage rollback in 1993 accounts for approximately $110 million of the gross property tax savings under "A." Should immediate-effect legislation eliminate the millage rollback in 1993 under "A," it would add this amount to the property tax for future years as well. See page 11.

Taxpayers Would Gain Greater Control Over Local School Expenditures

Taxpayers in most school districts would gain more control over their local school finances under "A" because of its little-noticed provision restricting millage elections to no more than two per year, and its allowance of only 9 voted mills for operating purposes. Rather than facing multiple elections each year and "all or nothing" ballot questions, taxpayers under "A" would have two or less elections per year, and each ballot question would ask for marginal increases in tax revenue. See page 18.

"A" Would Strengthen "Headlee" State Tax Limit; Weaken Local Share Requirement

The new sales and use tax revenue would be applied against the existing Article IX section 26 ("Headlee") state tax limit. Although the state government currently has substantial cushion above the limit, the additional state tax revenue under "A" would reduce tile opportunity for a future legislature to raise taxes. However, the additional state spending to local schools would also weaken the Article IX section 30 ("Headlee") requirement that the statesend 41.6% of their spending to local units of government. See page 25.

Many Implementation Questions Unresolved

The constitutional amendment leaves many definitions, implementing procedures, and interpretation question to the legislature. Probably the most important are the property tax limitation issues. Besides the definition of "operating" purposes millage. cited above, important unresolved questions include

How school districts can levy "extra-voted" millage in 1993 and thereafter; see page 8; and

What expenditures are included in the per-pupil guarantee, and whether such funding counts for categorical programs protected by the "Headlee" amendment: see page 20.

"A" Not School Quality Reform, Except by Encouraging Some Competition

"A" would substantially reduce the current disparity in school district expenditures, primarily by allowing lower-than-average spending school districts to spend more. The historical record indicates strongly that student performance has little or no relationship to expenditures, so increased public school expenditures under "A" would likely have little long-term benefit in terms of student performance. However, "A" would encourage some competition among public school districts by making it easier to adopt a limited "schools of choice" system. See page 20.

Proposal A is a constitutional amendment placed on the ballot by the legislature in House Joint Resolution G on April 1, 1993. It has three main components: property tax reduction and limitation, sales and use tax increases, and a per-pupil school funding guarantee.

Specifically, the proposal would:

Reduce school operating property taxes, and limit them to no more than 27 mills. Currently, the average rate is about 35, and has been increasing in recent years. Most school districts – over three-quarters – would initially levy only 18 mills, which would not require voter approval. Additional mills – up to 9 – would require voter approval. This reduction in school millage would reduce property taxes by over $2.1 billion a year.

Limit the total operating property taxes of all units of local government, other than cities, villages, and charter authorities, to no more than 40 mills. Currently, these units are limited to 50 mills in total, and the reduction to 40 mills would prevent other units of local government from raising their millage rates to offset the school tax reduction.

Limit the annual percentage increase in the assessed value of each parcel of property to the inflation rate or 5%, whichever is less, until the parcel is sold.

Increase the state sales and use tax rates to 6%, starting in July of this year. This will raise an additional $1.7 billion in 1994, but only half that in the current year. Because the sales and use tax increases would only affect half this year, and the property tax cut the entire year, taxpayers will save about $1 billion in 1993. Net savings after that grow from about $230 million in 1994 to $280 million in 1996.

Dedicate the additional sales and use tax revenue, and net state lottery proceeds, to the school aid fund.

Establish a minimum state and local per-pupil school funding guarantee, beginning at $4,800 and adjusted annually for changes in state revenue. School districts would be guaranteed at least a 3% increase in funding per pupil in the first year. This per-pupil guarantee would not be available to private schools. However, it would establish the principle of dollars-follow-students, and therefore would ease a future transition to a full choice system.

Proposal A's biggest change in dollar terms would be its reduction and limitation of property taxes. (Appendix I explains the Michigan property tax system.)

School and Local Government Millage Limits

The Constitution, at Article IX section 6, limits the property taxes that local governments can levy on their taxpayers. The limit applies to "all purposes," but also provides a specific exception for taxes levied to pay principal and interest on bonded indebtedness, which must be specifically approved by the voters and can be levied in unlimited amounts. Millage is called "operating" millage unless it is levied to repay voter-approved debt.

Currently, between 15 and 18 mills are "allocated" in each county between schools, townships. and the county. These allocated mills are not approved by the voters.[1] Additional mills, called "extra voted," are approved by voters for periods of up to twenty years at a time. The total millage, both allocated and extra-voted, is subject to a 50-mill limit. Cities, villages, and other charter authorities have separate tax limitations. and are not subject to the 50-mill limit.

Proposal A would create a new system of limits:

The first 18 mills of school millage could be levied by local school boards without voter approval. These would operate similarly to "allocated" mills under the current system.

The "allocated" mills would be reduced in each county by the number of mills allocated to school districts in 1992, thus removing any possibilityof other units of government capturing that allocation.

Voters could approve up to 9 additional mills for school district operations. As under the current system, voters could also approve unlimited debt millage above the operating millage limits.

The current 50-mill limit would be reduced to 40 mills, again to reduce the opportunity of other units of local government capturing the millage previously levied by school districts.

The first 18 mills of "allocated" school millage, and any of the 9 allowed "extra-voted" millage, would be subject to the same "Headlee" rollbacks required by Article IX section 31.

In 1993, school districts would be allowed to levy the number of mills necessary to fund their operations at the same per-pupil rate as the previous year, plus at least a 3% increase. With $4,800 per-pupil guaranteed at 18 mills, this would place over three-quarters of the school districts at 18 mills.

Implementation Issues: Millage Limits

The proposal limits school millage for "operating purposes," and again guarantees school funding for "operating purposes." The term "operating" has a long history of being used to define all expenditures other than debt. Since capital investment in buildings and equipment is both expensive and yields long-term benefits, capital expenditures are often financed through long-term borrowings, thus spreading the cost over the period of benefits. Both Michigan's Constitution and its statutes have long segregated "operating" funds from those to repay debt, and required specific voter approval for debt, for both state and local units of government.

A straightforward reading of Proposal A places it within this tradition. Nonetheless, the specific wording admits some ambiguity, which must be examined for both the school millage limits and the guarantee of per-pupil expenditures.

"Operating Purposes" Millage

The proposal limits school millage to 18 mills, plus 9 additional extra-voted mills for "operating purposes." The term "operating purposes" does not exactly match the "[e]xcept as otherwise provided ... all purposes" language earlier used in Article IX section 6 to limit operating millage. which provides an exception only for voter-approved debt.[2] This raises the concern that school districts may attempt to avoid the 18-p1us-9 millage limit through the imaginative use of a different type of millage.

Draft implementation bills circulated the week of April 29 excluded from the operating miilage limits the following:[3]

Building and site sinking fund millage previously authorized by the voters. The legislature exempted building and site millage from the definition of "operating" millage in the Truth in Taxation law, 1982 PA 5 at MCL 211.24e, even though the maintenance and repair of buildings are clearly operating expenditures. "Sinking fund" millage is closer to bonded debt for capital improvements, since it can be used for the "purchase of real estate for sites for, and the construction and repair of, school buildings." The draft bill would allow existing sinking fund millage to continue until its authorization expires, but allow no more authorizations after Proposal A was adopted. Although "repair" expenditures are operating expenditures, and would be allowed under such legislation, the bill would over time eliminate such problems by not allowing any new authorizations.

"Taxes levied … for eliminating an operating deficit." This is a more serious problem, since it invites school districts to run deficits, and then levy taxes above the limit to cover tile deficit. Excluding from the limit on "operating" millage taxes levied to fund an "operating deficit" is a clear circumvention of the language and intent of the amendment.

Within its context, the amendment is reasonably clear that its limit on school "operating" millage is meant to apply to millage levied for "all purposes … except" voter-approved debt repayment. First. the section still would begin "[e]xcept as otherwise provided inthis constitution, the total amount of ad valorem taxes imposed on real and personal property for all purposes in any one year shall not exceed 15 mills ..." The Subsequent provision for school millage would remain under the authority of this sentence. Second, section 31 of the same article, which applies "Headlee" rollbacks to millage authorized in section 6, exempts only voter authorized debt millage[4] and the proposal specifically states that school millage is subject to these same rollbacks. Third, the amendment goes on to restate the total limit on operating school millage as 27 mills, after previously limiting it to 18 allocated plus 9 extra-voted, and then further confirms that these mills fall within the 40-mill limit. Finally, the Property Tax Limitation Act. 1933PA 62 at MCL 211.201, follows the convention of "operating" meaning "all purposes other than debt "

Voter Caution: Legislative Implementation of Millage Limits

The allowance for the legislature to define "operating" is troubling, since it opens the possibility that their constitutional millage limits would be circumvented. The taxpayers' recourse would be limited to asking the courts to rule such taxes unconstitutional, seeking remedial legislation, or constantly fighting local millage elections. While success is possible – even probable – on these fronts, this is a lot to ask of voters who would be simultaneously approving an unambiguous, unchallengable sales tax increase. Should "A" pass, future judicial interpretation of the property tax limits will hinge on the what the average voter thought he or she was approving on June 2. 1993. Therefore, voters should pay close attention to any implementation language passed by the legislature prior to the election Judges wi11, in the future, likely place significant weight on such previously-enacted statutes in determining what the " common man" thought this constitutional amendment would do.

"Limited" Tax General Obligation Bonds

The Michigan Constitution, at Article IX section 6, as amended by the 1978 "Headlee" amendment, requires voter approval of bonded indebtedness that is the obligation of the taxpayers. This ensures that taxpayers who must repay the debt through future taxation give their consent to such taxation. Once consent to the debt is granted by the voters, the Constitution allows taxes to be levied without limit as to rate or amount to repay it. Proposal A would continue that tradition, allowing voted debt to be repaid by millage above the new 27-mill limit.

Since passage of the Headlee amendment, some units of local government have circumvented the constitutional requirement of voter approval of general obligation debt, through the use of "limited tax general obligation" bonds issued without the approval of the voters. Such debt is of doubtful constitutionality.[5] "Limited" tax general obligation debt is identical to general obligation debt, in that it must be repaid ahead of operating expenditures. However, taxes can only be levied for its repayment up to the maximum authorized millage rate – that is, the maximum millage authorized for operating purposes.

Under the previous system, school districts could hide the repayment of "limited" general obligation debt by simply repaying it with operating millage, with the taxpayers often unaware. Proposal A would expose this behavior, for two reasons. First, the operating expenditures of school districts would be more uniform, and thus easier to compare. Second, the state would be guaranteeing a flat amount per pupil for operating expenditures. Depending on the implementing language, operating expenditures could exclude repayment of debt for capital investment as the term "operating" normally implies. Such a definition would leave "limited" debt without a dedicated funding source. Since the voters never approved the debt. they could quite fairly balk at paying it.

Of course. the legislature would be under pressure to allow the state guarantee funds to be used to repay "limited" debt. Should it do so, it would constitute a state taxpayer bailout of debt never approved by any voters, state or local, and of obviously doubtful constitutionality. In this case, the amendment is not clear, and the subject would be left to implementing legislation and the courts

"Headlee" Rollbacks and Other Millage Limit Issues

The proposal also leaves the legislature other millage limit issues. First, it is not clear on how extra-voted school millage rates can be levied in 1993, although it implies that enough can be levied to raise at least 103% of the amount raised the previous year. A draft of Senate Bill 597 introduced on April 29 follows this approach. However, the proposal could reasonably be interpreted to require new voter authorizations for all extra-voted mills in 1993. Certainly, it leaves the impression that am authorization for millage above that necessary to raise 103% of the 1992 revenue. and any millage over 27 mills, is immediately repealed.

Second, it is not clear how, or if, school districts could raise their 18 allocated mills back to 18, if reduced by section 31 of the "Headlee" amendment. Since the proposal states that the state must make guarantee payments as if the district was still at 18, it could be argued that allocated mills cannot be increased once reduced by the "Headlee" amendment, even with a vote. Certainly, as is explicitly stated in the proposal, such millage must be reduced when assessment increases on existing property outstrip inflation, and could not be again raise without a vote.

The second tax limitation feature of "A" is a limit on assessment increases for individual parcels. The Headlee amendment currently limits tax increases caused by assessment growth to the rate of inflation, but applies the limit to all existing property, taken as a group. "A" would place a limit of 5% or the rate of inflation, whichever is less, and apply it to individual parcels. This limit on assessment growth would add to the tax savings created by the exemption, although it could be offset by millage rate increases.

In addition, the cap on assessment increases would result in less "Headlee" rollbacks in millage rates, since SEV would not grow as fast as actual values. Thus. millage rates would be higher under "A" than under current law, although property tax burdens would be significantly lower because of the limit on school operating millage.

Market Value Versus Acquisition Value Assessment

The cap on individual parcel assessment growth would change the current assessment scheme from a market-value system to an acquisition-value system. Rather than attempting to estimate the current market value of all parcels, assessors would rely on the cost of acquiring the property, even if it was years ago, in determining the current assessment. "A" would cap the annual adjustment at the inflation rate or 5%, whichever is less, until the ownership of the parcel is transferred.

The inflation rate has been under 5% for most of the past decade, and land normally increases in value at about the inflation rate. If these trends continue, many areas of the state would find that the majority of their parcels do not hit the assessment cap. In fact, the total State Equalized Value of property in the state – including new construction, which probably added another 1-2% each year – increased by an average of 5.2% per year in the ten years from 1982 through 1991.[6]

Thus, on average, the 5%-or-inflation cap on individual parcel assessments would not have been effective in reducing property taxes over the past ten years. However, the cap is not designed to protect "on average" – it is designed to protect owners whose circumstances have given them rapidly increasing assessments. This would be likely in tile following instances:

The inflation rate increases to 5% or more.

The market value of property increases due to more productive uses, for example, when converting farmland to residential use, or when private sector investment increases the productivity of nearby land.

Consumers shift preferences, making some areas more desirable than others, even without a change in the underlying use of the land.

Government actions increase or reduce the tax burden of certain parcels, restrict development rights or land usage, or finance improvements.

Assessing practices are arbitrary, improper, or changing.

Uniform Taxation

This proposal does attempt to make one change voters rejected in the past: it limits annual assessment increases on individual parcels of property.Limiting annual assessment increases on individual parcels would provide predictability to homeowners, and avoids the backlogged and clearly unfair assessment appeals system

The downside is that it creates disparities in effective tax rates. Owners of similar houses on the same street can end up paying significantly different tax bills, depending on how long they have owned their property. Their tax bills would probably be less than either would have paid had Proposal A not passed, but the lack of uniformity is a problem.

Uniformity and theConstitution

The lack of uniformity in an acquisition-value assessment scheme raises the question of whether such a system violates the U.S. Constitution's guarantee of equal protection under the laws This question was answered conclusively in a case involving a provision similar to "A" in the California constitution.

The U.S. Supreme Court, in Nordlinger v Hahn,[7] ruled that states may limit assessment growth oil individual parcels, and thus create different effective taxation rates, without violating the US Constitution's guarantee of equal protection under the laws. The court ruled that a state may establish an acquisition-value system of assessment, since it had at least two rational bases: The preservation of neighborhoods, and the predictability and affordability ("reliance interests") of future property taxation.

The U.S. Supreme Court, in the prior case Allegheny Pittsburgh Cool v Webster,[8] had ruled that arbitrary differences in tax rates, when those differences were contrary to state constitutions directing uniform taxation, violated the equal protection clause of the U.S. Constitution. The court noted in the Nordlinger deacision that the rational bases for the California constitution's assessment-growth cap contrasted with the facts in Allegheny which "precluded any plausible inference that the reason for the unequal assessment practice was to achieve the benefits of an acquisition-value tax scheme."[9]

Proposal A would create an acquisition-value assessment scheme for the State of Michigan which would share the same rational bases as California's Proposition 13, and thus should be upheld against any federal Constitutional challenge.

The proposal contains an unusual, and perhaps unintended interaction between the per-parcel assessment growth cap it would place in the Constitution and the existing "Headlee" amendment limit on tax increases caused by assessment growth in an entiremunicipality. Proposal "A" would not be effective if approved by the voters until after the "Headlee" amendment already reduced millage rates in 1993.[10] Thus, many taxpayers would receive a "double rollback" in 1993; a "Headlee" millage rate rollback, and a Proposal "A" assessment rollback.

Article IX. Section 31 (part of the "Headlee" Amendment) states in part:

If the assessed valuation of property as finally equalized, excluding the value ofnew construction and improvements, increases by a larger percentage than the increase in the General Price Level from the previous year, tile maximum authorized rate applied thereto in each unit of Local Government shall be reduced to yield the same gross revenue from existing property, adjusted for changes in the General Price Level, as could have been collected at the existing authorized rate on the prior assessed value.

This sentence requiring "Headlee rollbacks," would not be modified or limited by any other operation of Proposal A. The key phrase is the beginning of the sentence, "[i]f the assessed valuation of property as finally equalized . . . " Section 34 of the General Property Tax Act (MCL 211.34) states that the county board of commissioners in each County shall meet in April to determine county equalized value, which equalization shall be completed and submitted before the first Monday in May. The state board of equalization under 1911 PA 44 (MCL 209.4) must receive the reports from the counties' assessing officers and the state tax commission by the fourth Monday in May. Although the provision is made in these laws for subsequent adjustment based on appeals to the state tax tribunal, itappears that property is "finally equalized on the fourth Monday of May when the State Equalization Board meets.

Appeals

Section 39a of the GPTA (MCL 211.39a) requires that. Should an appeal to the tax tribunal delay determination of county equalized value, the assessing officer shall levy taxes upon the equalized value of property as determined by the state board of equalizations. While this section goes on to state that the results of such appeals may result in an adjusted tax rate, called a "final levy," such appeals would be confined to those made on the basis of deviations from 50% of true cash value under current law, not speculation over ballot issues. Appeals by local officials within a county under Section 34(4) (MCL 21 1.34) for improper equalization could lead to a change in the relative assessments within the county, but not the overall assessment.

Tax Reduction From the "Double Rollback"

The "double rollback" would result in additional property tax savings above that required by either the Headlee amendment alone. or the 3% maximum change for individual parcels. This reduction would occur in 1993, and would establish a lower millage base for future years. However, its impact is limited to operating millage levied by units of local government other than schools, since school millage would be reset by the constitutional amendment and its implementing legislation based on prior year revenue. See the section on the school funding guarantee, page 19.

Using the model presented later in this study, page 21, the additional gross property tax savingsfrom a "double rollback" in 1993 would be approximately $110 million.[11]

By reducing property tax burdens significantly, "A" would give a powerful boost to the state's economy. The permanent reductions in tax burden would result in greater disposable income available to Michigan consumers, increases in wealth due to tax capitalization and better incentives to entrepreneurs to locate in Michigan. As detailed in Appendix I to this study, page 30, such a reduction in tax burden would increase employment and improve per-capita income.

Tax Capitalization

A lower tax rate directly increases the value of an economic asset, through tile phenomenon known as "tax capitalization." Whenever the cost of holding an asset declines, its value increases, since the owner now will be required to pay less each year. This improvement of the owner's cash flow is capitalized into the price of the asset. Tax capitalization in property values is well established in commercial practice, the law of taxation and assessment, and the financing of homes. The revenue analysis in this study explicitly includes estimates of tax capitalization. To not include tax capitalization would be to ignore fiscal reality, as well as Michigan law. Further explanation of the commercial. legal and financial aspects of tax capitalization is in Appendix II, and the revenue analysis is presented on page 21.

This analysis indicates that permanent reduction in property taxes under "A" would result in a large increase in the wealth of Michigan property owners on the order of $l6 billion. This would be about $1775 for every Michigan resident in real, spendable wealth – a further stimulus to the Michigan economy.

Because "A" would affect both the property tax rate and its base, the sales and use tax rates, credits against the Michigan income tax. and deductions under the Federal income tax, and affect the disposable income, homeowner's equity and business incentives of Michigan residents, a proper individual analysis is not easy. Many of the early analyses of Proposal "A" contained examples of individual taxpayers designed to determine whether such taxpayers would pay more, or less in total taxes. None of these took into account the full impact of the proposal, and some were deeply flawed.[12] Among the effects left out of some of these analyses were:

Ignoring the effect of lower taxes on property values. or ignoring the change in assessments over time altogether;

Ignoring likely millage rate changes because of "Headlee" rollbacks, or ignoring SEV changes all together;

Ignoring the first-year impact of an entire year of property tax savings along with 5 1/2 months of sales tax increases;

Incorrectly assuming that most individuals both receive an itemized deduction for property taxes and a "circuit breaker" credit; as discussed below, only about a third of Michigan taxpayers itemize, and many two-earner or higher income households are ineligible for a full circuit breaker credit;

Ignoring the effect of reduced business taxes on workers, investors. and consumers; while the discussion below indicates a detailed breakdown may be impossible, it also concludes that at least $400 million in these benefits go to Michigan residents;

Ignoring the impact on non-property owners such as renters and students, or assuming the impact is entirely negative;

Incorrectly assuming that half or more of annual income typically is spent on sales-taxable items, or that the sales tax isn't "progressive" or "fair;"

The sections below discuss the actual impact on different classes of taxpayers

Renters

Renters pay property taxes through their rent. The Michigan income tax code allows renters the same "circuit breaker" credit by assuming that 17% of rental payments go to property taxes. By reducing the tax burden on rental property, "A" would lead directly to a reduction in rent. This reduction would be delayed for many renters until the end of their lease period, and would be mixed in with other costs, many of which will be rising. A rough estimate of the average effect, over time, on rent due to the property tax cut would be a reduction of around 4%.[13] Because other costs will probably increase, the reduction in the property tax costs would show up in many areas as a slowdown in the increase in rental costs. The reduction in rent would not come about because of government edict, but because of competitive market pressures – a far more effective control on profit margins and prices.

Consumers

People will face the sales and use tax increase when they consume goods and services. The sales and use taxes are consumption taxes, which do not penalize savings and investment like income and property taxes.

"Fairness" and the Sales Tax

The property tax is widely seen to be an unfair tax, because it is not related to "ability to pay" and because the assessing system is not reliable. On both these measures the sales tax is much more "fair." First, there is little question over the base of the tax, since it is generally collected on the sales price. at the time of the sale.

Second, the sales tax is very closely related to "ability to pay." Despite frequent claims to the contrary, the Michigan sales tax is slightly "progressive" when properly analyzed, meaning that the proportional burden increases as income increases. Two factors account for this: First, the sales and use taxes exclude food, prescription drugs, and most services including rent. For many lower income taxpayers, food, drugs, and rent are a very high proportion of their spending. As a statewide total, the sales and use tax revenue compared with personal income in the state indicates that about 45% of income is spent on sales- or use-taxable items.[14]

The second factor is that consumption, over a period of years, tracks income almost exactly. Taxpayers who earn more than they spend in a single year and save the difference, are simply deferring their consumption.[15] In a typical lifespan most taxpayers start out consuming far more than they earn (as children, teenagers, and college students); then begin earning. although borrowing heavily; then earn more than they spend, as they pay off debts and save for retirement; and finally begin spending much more than they earn, by living off pensions and other savings. Over the life cycle, a flat percentage sales tax ends up taking about the same share of income from high-income as low-income taxpayers. With the exclusions for food, drugs, and rent, the Michigan sales tax is slightly progressive.

Embedded Business Taxes

Consumers also pay taxes mixed into the prices of their goods and services. Much as renters pay property taxes through their rent, consumers pay business taxes through the prices of every good and service they purchase. Business taxes are also paid indirectly by investors, who receive lower returns. Since the majority of investments are made for retirement savings and pensions, this means lower income during retirement years. Finally, workers receive lower wages because of business taxes. Since workers require both real property (land) and personal property (computers and equipment) to work productively, the property tax is an indirect tax on their output, and therefore their wages.

Embedded local business taxes are almost impossible to decompose into the prices consumers pay, the returns investors receive, and the wages workers receive. Nonetheless, the reduction in the property taxes businesses pay will provide a significant benefit to Michigan Consumers, investors, and workers. In the aggregate, business property tax reductions would add at least $400 million of benefits to these groups.[16]

Senior Citizens and the "Circuit Breaker"

Many senior citizens benefit from an income tax credit for property taxes, known commonly as the "homestead" or "circuit breaker" credit. The Constitutional amendment contained in Proposal "A" would not change the "circuit breaker" program, which was created by state law. This credit can be for up to 100% of property taxes above a fraction of income, within certain income limits and subject to a $1200 limit. Many analyses of "A" assume that all senior citizens receive this credit. and that a reduction in income tax credit offsets their entire property tax cut.

This would not apply to the majority of senior citizens, for the following reasons. First, according to the Department of Treasury, 30% of those seniors receiving income tax credits for property taxes are already at the $1200 limit.[17] Thus, a reduction in their property taxes at least initially does not reduce their credit. Second, a reduction in property taxes is an immediate increase in disposable income, while a property tax credit is often received sometime the following spring or summer. Taxpayers are better off holding their own money, rather than allowing the state to draw interest on it. Third, the income thresholds are not indexed to inflation, and apply to total household income.Thus, many seniors who have saved for their retirement, or who have some earnings, are not eligible for the full credit. (This is particularly true for non-senior citizens families with two-earners.) Finally, the "circuit breaker" is a part of the income tax code, which can be changed at any time by the legislature. Even if it is not changed, inflation is slowly reducing its value.

The State/Local Balance and the Lottery Debacle

"A" would constitutionally dedicate lottery earnings to the school aid fund. However, this is more an attempt to redress an injustice perpetrated over the past two decades than to reduce property tax burdens. Lottery revenue is already dedicated by statute to the school aid fund. However, under "A" the state/local share of public school funding will return to close to what it was in the mid-1970's, plus additional lottery funding: about 58% state share, plus another 8% for the lottery.[18]

Proposal "A" would have significant indirect effects including those on federal tax liabilities. The biggest immediate effect is a reduction in property taxes which are deductible for those who itemize under the current IRS code. Sales taxes used to be deductible, but currently are not. The revenue analysis in this study does not include federal tax effects for three reasons.

First, the federal tax code will almost certainly change. The new administration has several times promised to increase taxes on "the rich," and their formal proposals have specified tax increases on those with income as low as $25,000 – making "rich" a very vague term indeed. The sales tax used to be deductible, and property tax deductions are already limited for higher-income taxpayers. Thus, it is not at all clear what the future federal tax code will be.

Second, only about 35% of Michigan taxpayers itemize their deductions, and those tend to be the higher-income taxpayers. Thus, the majority of Michigan taxpayers do not now receive any federal deduction for property taxes, and the new administration in Washington has already proposed tax increases on everyone else, which could easily include further restriction on property tax deductibility.

Third, analyses that include federal tax deductibility normally make two other incorrect assumptions: that the additional federal taxes bring no benefit to Michigan, and that all Michigan taxes are paid by Michigan residents. In the first case. the benefit to Michigan of an additional dollar's worth of federal taxes is clearly a small fraction, but probably not zero. In the second case, tourists pay probably pay 5% or more of the sales and use taxes in the state, although this figure is not well supported by evidence. Thus, to include federal deductibility, we would have to also include these other factors.

The impact of these factors, while not included in the basic analysis is estimated separately in the "What if?" section, page 24.

A key question for taxpayers is whether the proposal would strengthen their control over their local school expenditures. Since school millage is both the largest source of property taxes, and the most rapidly growing, this concern is crucial.

At first glance, the expansion of the nonvoted "allocated" mills to 18 would reduce taxpayer control. This is clearly the case in the handful of school districts which currently levy less than 18 mills.[19] However, for the large majority of school districts, the proposal would increase the taxpayers' control over local school district expenditures, for the following reasons:

The allowance of 18 nonvoted mills means that voters will only make decisions on marginal expenditure increases, up to an additional 9 mills. School districts will not be able to combine their millage requests into an "all or nothing" proposition, and would not be able to threaten voters with closure of the entire school system if a millage request fails at the ballot.

The proposal, in a little-noted sentence, restricts school districts to no more than two millage elections each year. This eliminates the practice of continually asking the voters to approve a millage until they are finally worn down.

By establishing a uniform statewide per-pupil guarantee, "A" would enable taxpayers to more easily see the actual expenditures of their school district and compare them to others.

The proposal would increase the state sales and use tax rates from the current 4% rates to 6% effective July 17, 1993.[20] The limit on the sales tax rate would also increase to 6%. There would be no change in the current exclusion for food and drugs.

The Use Tax Act is a separate Public Act from the General Sales Tax Act, and both are currently levied by the state at 4%. However, other use taxes are also levied. The proposal does not establish a limit on use tax rates, nor does it prohibit local use taxes. The legislature has allowed various units of local government to levy use taxes as high as 30%.[21] The courts have held that use taxes are not limited by the current constitutional sales tax limit of 4%, and the amendment would not change this.[22]

The proposal also would dedicate the revenue from the additional 2% rate of state sales and use taxes to the school aid fund.[23]

Proposal A would establish a per-pupil state and local funding guarantee for all local public school districts across the state. For each district levying 18 mills the state would guarantee that the combined local property tax revenue and state aid would equal at least $4,800 per pupil. This guarantee is indexed to state and local revenue growth adjusted for tax rate changes. Thus, the local school districts would have a stake in a growing Michigan economy.

In the initial year, millage rates above 18 mills would be determined as the rate necessary to allow a 3% increase. This is implied in the constitutional amendment, and stated in Senate Bill 597 introduced on April 29. According the Michigan Department of Treasury, the statewide average school operating millage under "A" would be approximately 22 mills.

Hold Harmless & Transition Rules

Schools currently receiving more than $4,800 revenue per pupil would be guaranteed at least a 3% increase in 1993-94, and future aid to ensure no reduction in revenue. Those school districts receiving less than $4,800 currently would be limited to a 10% annual growth in revenue.

Does More Money Mean Better Schools?

School districts currently spending less than $4,800 per pupil would receive 10% per year increases in funding until they reach the per-pupil guarantee level. Since this level would be indexed as well, it would give some school districts 10% annual revenue increases for a number of years. This is a substantial increase in revenue, and will result in those districts currently below the state average in spending to dramatically increase salaries, facilities, and workforce size.

Reducing the disparity in per-pupil spending is one goal of the amendment, and the proposal would accomplish that by increasing the spending of the lower-spending districts. Will such an increase in spending result in improved education, or just more spending? Exhaustive research over the past quarter-century has demonstrated clearly that there is no firm relationship between spending and student performance. As Eric Hanushek's research, recounting 187 studies on public schools, concluded: "There is no strong or systematic relationship between school expenditures and student performance."[24] Thus, while the goal of reducing the Current disparity in expenditures may be laudable, the higher expenditures in and of themselves will probably not result in better student performance.

What "Schools" Are Guaranteed Funds?

The Constitution, at Article V111 section 2, currently prohibits state aid to nonpublic schools, so all "schools" would not receive funds under "A." However, "A" would establish the principle of the state guaranteeing a per-pupil amount of funding. This would allow an easier transition to a system where parents could choose which schools their children would attend, with the dollars following the students. Unless the prohibition on aid to private schools was changed, however, such a "schools of choice" system would be limited to public schools.

Given the likelihood that increased school expenditures under "A" would not result in improved student performance, this prospect for a limited amount of competition is probably the most important school quality reform contained in "A."

What Does the Guarantee Fund?

The proposal would guarantee school funding for "operating purposes," and also allows the legislature to fund additional "instructional programs." Currently, the state gives "formula" aid to most school districts, and "categorical" aid for specific programs to all.[25] Proposal "A" would roll many of these funding vehicles into one. This would allow school districts to more efficiently use their funds, since the local districts could choose how best to allocate resources.

This raises two implementation questions that are not resolved in the amendment itself. First, the legislature is allowed to define expenditures for operating purposes, and to select additional "instructional programs" for additional funding. Second, and more important is the question of what guarantee funds are counted against the requirement in Article IX section 29 ("Headlee") that the state fully fund all mandated school programs. Some categorical programs, such as vocational education, are required by state law, and the "Headlee" amendment requires that the state fund these, even for "out of formula" school districts.[26] The amendment implies that such programs would continue to receive protected funding, but it is not clear whether guarantee funds could be counted as funding for required programs. These questions are important both in terms of local control, and the continuing effectiveness of the "Headlee" amendment in protecting local school districts.

The revenue projections were generated by an economic model developed by the author for the Mackinac Center for Public Policy. The model differs from the standard. "static" models commonly used in government agencies in that it attempts to estimate the actual, dynamic behavior of individuals when confronted by changes in tax rates. This dynamic behavior is reflected in changes in the value of property, the avoidance of laws, voter approval or rejection of millage rates, and the partial capture by other taxes of additional disposable income from a cut in the property tax. The model is discussed in detail in Appendix III, on page 37.

This study takes a skeptical view of additional tax relief contained in other bills, but not included in the amendment. In particular, it does not assume the enactment of SB 146, which would create a one-year delay in assessment increases starting in 1994. It does include a "double rollback" in 1993, as discussed on page 11, because it is required under current law.

Results from the model include:

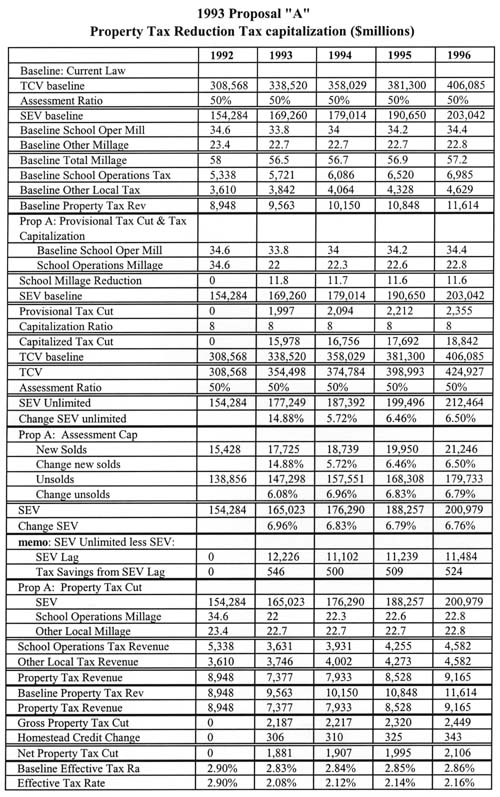

School millage rates are cut from a statewide average of 34.6 in 1992 to 22 mills in 1993, generating a gross tax cut of $2.2 billion in the current year. After adjusting for reduced "homestead" income tax credits, the net property tax cut in 1993 is almost $1.9 billion, which grows to over $2.2 billion by 1996.

The value of property under "A" grows from $308 billion in 1992 to $408 billion in 1996, partially due to "tax capitalization" of roughly $16 billion in 1993, growing to almost $19 billion in 1996.

Because of the assessment-growth cap. the State Equalized Value (SEV) grows more slowly, from $154 billion in 1992 to $200 billion in 1996. The combined effect of higher property values, and capped assessment increases, is annual tax savings of over $500 million from 1993 through 1996. Interestingly, the assessment cap does not stop the growth of SEV, which continues to grow only slightly slower than under current law for two reasons: First, as parcels are resold, their re-assessed values are significantly higher. Second, new construction of roughly 2% per year comes directly into SEV.

Sales and Use and other state tax revenue increases by over $800 million in 1993 and almost $1.7 billion in 1994. This includes two adjustments from the consensus estimate by state government agencies of the sales and use tax revenue increase under "A," which basically assumes that a 50% rate increase results in a 50% revenue increase. First, it adds the tax revenue gained from the additional disposable income from the net tax cut. Second, it accounts for consumers' avoidance of the 50% higher sales tax rate. Using conservative estimates of tax avoidance behavior, the model predicts that a 50% increase in the sales and use tax rates would result in a 5% drop in taxed transactions. This tax avoidance results in about $135 million less sales and use tax revenue in 1994 than the consensus estimate.

The net state-and-local impact on Michigan taxpayers would be a sharp $1.1 billion tax cut in 1993, and a smaller tax cut of $237 million in 1994, growing to $282 by 1996.

Table Two presents the summary results of the model.

The results presented above represent the best estimates, based on reasonably conservative assumptions. These assumptions will certainly not accurately predict all the variables used in the model. However, sensitivity analyses, or "what if?" tests give some indication of how the results would change if the assumptions were changed.

Assessment Lag in 1994 (SB 146)

The consensus government agency estimates of tax relief under "A" include the effects of Senate Bill 146, which would introduce a one-year delay in assessing property in 1994. An estimate of the additional tax relief under SB 146, on top of the net tax savings under "A," is about $440 million.[27]

Federal Deductibility and Tourist Taxes

For the reasons discussed above, page 17, the revenue analysis did not include federal tax effects. A rough estimate of the effect of federal income tax deductions, under the current federal income tax code, would be about $185 million in additional federal taxes per year.[28] If the common, although unsupported, assumption that tourists pay 5-10% of Michigan sales and use taxes is correct, then non-Michigan residents would account for around $90 to $180 million in additional sales tax revenue. Neither of these estimates are as reliable as those included inthe revenue analysis in the model, and the fact that they roughly offset each other is another reason for excluding both.

School Millage Rates

The level of school millage rates is a critical assumption under "A." The analysis relies on the Treasury Department calculations, based on their large database and proposed implementation legislation, in assuming an average school millage rate of 22 in the current year under "A." As a conservative assumption, the model assumes that school millage rates grow 50% faster under "A" than under current law for the next few years.

To estimate the effect of higher school millage rates, the entire model was re-calculated using an average school millage rate one mill higher. The effect was to reduce net taxpayer savings by about $140 million per year. The same exercise, using a reduction in the average millage rate of one-half mill, produced additional taxpayer savings of about $75 million per year.

Proposal "A" would have some important effects on protections offered to local units of government and all state taxpayers.

State Taxes and the "Headlee" Tax Limit

The "Headlee" amendment to the Michigan constitution, at Article IX, section 26, contains a limit on the total amount of taxes the state can take. as a percentage of personal income. Because of the peculiar economic circumstances at the time the amendment was adopted, the state has enjoyed a substantial cushion above the limit during most years since its adoption.[29] "A" would increase state taxes by approximately $1.7 billion in 1994, which would be applied against the limit. The state currently has a substantial cushion of at least $3 billion below the limit, although this would fluctuate with the economic cycle even under current law. By using up about half of the current cushion, "A" would have the effect of preventing a future legislature from levying a substantial state tax increase.

State Aid to Local Government and the "Headlee" Minimum Local Share Requirement

As the additional sales and use tax revenue is counted against the "Headlee" state tax limit, the additional state aid to schools under "A" will count against the "Headlee" minimum local share requirement, established at Article IX, section 30 of the Michigan Constitution. Section 30 of the Headlee amendment requires the state to send at least 41.6% of all its spending to local units of government taken as a group. "A" has the intended effect of increasing state aid to local schools while reducing local property taxes. It also has the unintended effect of reducing the effective protection of other units of local government under the Headlee amendment. While local units of government would still have section 29 of "Headlee" which requires state funding of any mandated program of local governments, non-school local governments would not have the same protection against reductions in the total amount of state aid.

"A" carries enormous benefits to the state, along with considerable risks. The voter is being asked to change their Constitution, significantly increase their sales and use tax rates, and trust that they will receive permanent property tax relief that outstrips the sales and use tax increases. This is a tall order, and requires a skeptical and thorough review. Two questions spring to mind: Does it truly reduce and limit taxes, and does it repeat the mistakes of past proposals? Let us examine each question.

The revenue analysis in this study is deliberately conservative. It does not include any promised tax relief not spelled out in the Constitutional amendment. It assumes that both taxpayers and government officials will continue to act in their interests – meaning tax avoidance on the part of taxpayers, and revenue maximization on the part of government. It relies on an independent model, with no results, or even assumptions, accepted uncritically from the same government agencies that have forwarded the proposal.

The results are clear. "A" is a big tax cut in the first year and a small tax cut in the succeeding years. While individual circumstances will vary, there is no doubt that the average Michigan resident would have more disposable income left after state and local taxes under "A" over the next few years than without it.

Why should voters adopt "A," when they've rejected so many seemingly similar proposals in the past? This proposal is soundly designed to provide immediate tax reduction, true tax limitation for the future, and a school funding guarantee that protects even school district against reductions in funding. Past proposals have failed because they lacked one or more of these features:

The two proposals defeated overwhelmingly in 1989 were both net tax increases. This is a net tax cut.

Proposals in 1992 and 1989, although billed as property tax limitation, would have allowed higher property taxes. This proposal follows up on tax reduction with strong tax limitation.

The voucher plan proposal in 1976 would have eliminated school property taxes but did not specify how the new educational voucher would be financed. This proposal creates a per-pupil guarantee (although not for private schools) and dedicates sales tax revenue and lottery proceeds to fund it.

Proposal C in 1992 would have cut taxes by over a half-billion the first year, growing to $2 billion within a few years. Many school administrators and public employee union officials felt this was too much of a tax cut and did not identify a school funding source. This proposal is a modest tax cut of around $250 million in 1994 and constitutionally allocates funding for schools.

While the proposal avoids the problems that doomed the preceding proposals, it does contain one provision featured in a previous proposal which failed at the ballot box:

Both this proposal, and Proposal C of 1992, contained per-parcel caps on assessment growth. These overlap the existing Headlee amendment protections, and introduce nonuniformity in taxation, but also relieve much taxpayer anxiety over the current assessment system.

Although introducing some non-uniformity via an individual parcel assessment cap, the proposal avoids the systematic disparities that marred earlier measures.[30]

The proposal passes the big test: it is a tax cut. Furthermore, it avoids the obvious mistakes that doomed previous proposals. However, it has more than the usual number of uncertainties which leave the legislature with considerable leeway in implementing it. In particular, the all-important tax limitation provisions leave to the legislature the task of defining and implementing the limits. This is the major danger to the proposal, and voters should watch very carefully what the current legislature enacts to implement "A." The courts, who will certainly be forced to adjudicate disputes over just what the amendment means should it pass, will likely give heavy weight to any statute passed before the election date, since voters would presumably have been able to include this information in their thinking.

If implemented in a straightforward manner. "A" would be a boon to the Michigan economy. It would mean a billion-dollar tax cut in the current year, a quarter-billion dollar or so tax cut in future years and over $16 billion in additional wealth to Michigan property owners. It would make Michigan a more competitive state, and help the private sector create and retain new jobs.

It would probably not directly increase public school performance. since more dollars have little relationship with better performance. However, it would encourage the prospect of competition among public schools, and allow better management efficiency within districts.

Its major drawback is the allowance for legislative implementation of numerous provisions. Especially worrisome is the possibility that the property tax limitations could be weakened. While the amendment itself is reasonably clear that all school property taxes are firmly limited, it also allows the legislature to define important points of this limitation. Voters must watch carefully to see whether this legislature exercises this responsibility with integrity.

Given the great taxpayer benefits that the proposal offers if implemented properly, the major question is one of trust. Each voter must ultimately decide for themself if the obvious benefits are worth the risks.

This appendix discusses and explains the existing property tax system in Michigan, in the following sections:

Michigan's Property Tax Burden;

Tax Reduction and the Michigan Economy

Your Property Tax Bill Explained; and

The "Headlee" Amendment.

Readers who are familiar with these topics may wish to skip ahead to the following chapters and appendices.

Michigan taxpayers paid over $9 billion in property taxes in 1992 – more than tile sales tax and income tax combined. Almost 70% of property tax revenues go to local public school districts, with the rest split between cities, townships, counties, community colleges, and other local authorities.[31]

By any measure, Michigan's property tax burden is much higher than the national average. Wide the exact ranking among the 50 states varies with the year and the measure, Michigan consistently ranks in the top 15 states for property tax burdens on their citizens.

A recent survey by the Senate Fiscal Agency recorded Michigan's property tax burden on two important scales.[32]

Property Taxes per $1,000 of Personal Income: This measure. from the U.S. Census Bureau, is probably the best measure of the relative burden of taxes. In fiscal year 1990, Michigan ranked 10th among the 50 states with $47.09 in property taxes per $1.000 of personal income. The national (50-state) average was $35.62. Michigan's high burden also placed it second among the 12 Midwestern states.

Property Tax Effort Index: This sophisticated measure developed by the Advisory Commission on Intergovernmental Relations takes into account the tax revenue raised and the value of property that is taxed. For 1988 (the latest year available), Michigan's index of 157 was the second highest among the 50 states, which had an average index of 100.

The Senate Fiscal Agency study also notes that Michigan's property tax burden would still rank among the top 15 on both these scales if "Homestead" income tax credits were assumed to reduce the property tax burden.[33] Other studies have also shown Michigan's property tax burden to be much higher than the national average.[34]

Since property taxes are almost entirely local taxes in Michigan, this high state average includes communities with more reasonable burdens, as we as those with stratospheric property tax rates. In particular, Detroit was rated the city with the highest property tax burden on a typical family among the largest cities in all 50 states and the District of Columbia.[35]

In addition to high property taxes, Michigan has consistently endured a much higher overall state-and-local tax burden than most other states. The income, business, and property taxes are significantly higher in Michigan than in most other states, while the sales tax is somewhat lower.[36] However, Michigan's total state-and-local tax burden. while still above the national average has recently become much closer to the average of the other states, for two reasons: First, other states have raised taxes, while Michigan has not; and second, Michigan's economy has not grown as rapidly as other states, and therefore has not generated the same increase in tax revenue.

For almost a half century following the beginning of the Great Depression, Michigan enjoyed per-capita income above the national average. Beginning in the early 1980's our per capita income dropped to and then below the national average, where it stands today. This decline in relative economic strength came on the heels of a dramatic increase in state and local tax burdens beginning in the 1960's.

Both economic theory and common sense hold that Michigan's high tax burden depresses economic growth by reducing the disposable income available to consumers, and discouraging entrepreneurs from locating in the state.[37] Research beginning in the late 1970's. and continuing into this decade, has confirmed that high tax burdens are associated with slower job growth more unemployment, less attraction of new businesses, and income stagnation. These Studies also confirm that reducing tax burdens powerfully improves the economic prospects of a state.[38]

For example, the five states that raised taxes the most between 1978 and 1987 saw real per-capita income fall by an average 1.1%, while the five states that reduced taxes the most saw real per-capita income increase by an average 8.5%.The five "tax increase" states saw their unemployment rates increase by an average 2.6%, while the five "tax cut" states enjoyed a decline in their unemployment rates of an average 0.5%.[39] See Table Three.

Two states in the "tax cut" group, California and Massachusetts, began the decade under study with major property tax cuts – "Proposition 13" in California, and "Proposition 2 1/2" in Massachusetts. Both states saw dramatic economic growth following the tax cut, as evidenced by the results in the table. However, by the end of the 1980's or beginning of the 1990's both had reversed fiscal policy, and substantially increased taxes. Subsequently, both experienced economic and budgetary distress. This is a clear lesson for Michigan: An industrial state can significantly improve its economy with a tax cut, or it can depress its economy with tax increases.

The property tax bill on each parcel is the product of three factors:

Property tax bill = "True Cash Value" of parcel x Assessment Ratio x Total Millage Rate.

Each of these factors is discussed below.

Assessments

Property taxes are ad valorem taxes, or taxes levied on the value of an asset. Thus, assessing the value of property is just as important in determining the property tax bill as the millage rate.

Market value, called true cash value in the Michigan Constitution, is the value of a parcel of property at a normal sale. Since parcels do not sell every year, their value must be estimated using some method, other than reviewing a sale price.[40] These estimates, or assessments, are made by local tax assessors employed by local governments.

The assessments of all property in each jurisdiction are then collected, and adjusted or equalized by the counties and finally by the State Tax Commission. Equalization ensures that local assessors do not under-assess their parcels, in tile hopes of passing off some of the tax burden on other areas within the same taxing jurisdiction. Normally this happens in the background with little input notice or input from the taxpayer. After local assessments have been equalized by the State Tax Commission, the values given to property are known as State Equalized Value (SEV). This SEV, or a preliminary estimate of SEV, appears on a notice issued in the spring of each year to property owners.

The assessment and equalization processes are intrinsically inaccurate, and inequities and abuses are common.

Assessment Ratio

The SEV of a parcel of property should be about half the actual market value. This ratio is know as the assessment ratio, or the portion of the value of property on which taws are paid. The Constitution sets the assessment ratio at no more than 50% and the Michigan Legislature in the General Property Tax Act, set the ratio at the maximum 50%.

At the current assessment ratio of 50%, a home with a true cash value of $100,000 should be given an assessment or SEV of $50,000. A millage rate of 57 (about the current statewide average) would produce tile following property tax bill:

$100,000 x .50 x 57/1000 = $2,850.00.

Millage Rates

A mill is a rate of 1/1000. In the equation above, a millage rate of 57 mills is expressed as 57/1000, and multiplied by the assessed value of $50,000.

Millage rates are levied by schools (about 70% of total millage), counties (11 %), cities (15%) and other authorities. The Constitution sets a 50-mill limit on property tax rates, but exempts voted for general-obligation debt millage, cities, and certain other chartered authorities from the limit.[41]

Thus, most urban and many suburban areas levy substantially more than 50 mills and the

statewide average now totals about 57 mills.[42]

Article IX section 31 of the Constitution added as part of the "Headlee" Tax Limitation Amendment of 1978, limits the tax revenue increase that results solely from increases in assessments. Should the value of property, excluding an increase due to new construction, increase faster than the rate of inflation, the excess growth requires a proportionate reduction in the maximum authorized millage rate. This mechanism keeps the property tax bill for the entire taxing jurisdiction growing at about the "real" rate of growth in the district.[43]

A lower tax rate directly increases the value of an economic asset through the phenomenon known as "tax capitalization." Whenever the cost of holding an asset declines, its value increases, since the owner now will be required to pay less eachyear. This improvement of the owner's cash flow is capitalized into the price of the asset. Tax capitalization in property values is well established in commercial practice, the law of taxation and assessment and the financing of homes.

The revenue analysis in this study explicitly includes estimates of tax capitalization. To not include tax capitalization would be to ignore fiscal reality, as well as Michigan law.

Commercial, Legal, Financial Use of Tax Capitalization

Investors in Commercial properties, such as apartment and office buildings routinely capitalize the expense and revenue streams predicted for a property when estimating its market value. For example, if an apartment building returned $12,000 a month in rent, and cost $10,000 a month in expenses and taxes, the margin of $2000 a month would be capitalized to estimate the market value of a property. To "capitalize" an income stream means to project out the cash flows into the future, and then add up the net present value (the value after discounting for the time value of money) of those flows. In the example, an income stream of $2000 a month or $24,000 a year might be capitalized at 10:1 to reach an estimated value of $240,000.[44]

Michigan law relies on the capitalization of revenues and expenses, including property taxes as one of three recognized methods of assessing property.[45]

Mortgage lenders use this principle in determining how much a home buyer can borrow.[46]

Thus, law, economic theory, and current practice ensure that a reduction in property taxes will result in an increase in the value of property.

Tax Capitalization and Tax Revenue

"A" would reduce the tax expenses of holding a parcel of property, and therefore increase its value. The increased value will result in higher tax revenue than would have occurred without the increase in value. In this case, the reduction in school operating tax rates would be capitalized into the true cash value of property across the state. This higher true cash value will then be taxed, but at the lower rate. Because of the higher true cash value the change in tax revenue will be less than the change in the tax rate.

An Example of Tax Capitalization

For example. Take a property with a true cash value (TCV) of $200,000, assessed at the 50% ratio at $100,000, and paying school operating property taxes of $3300 at 33 operating mills. A straight 30% reduction in taxes – dropping down about 10 mills – would be .30 x $3300 = $990. Capitalizing this into the market value of the property, using a 10:1 capitalization ratio, yields additional TCV of $9,900, for a total TCV on the property of $209,900, assessed at 50% at $104,950. The new school taxes of 23 mills would be .023 x 104,950 = $2,413.85.[47]

Comparing this with the original tax bill of $3300 shows how tax capitalization does two important things: First, it increases the value of the property. In this example, the property owner experienced an increase in wealth of $9,900. The property owner could recognize that immediately through a home-equity loan or the sale of the property or wait until later.

Second, the nominal reduction in property taxes is slightly smaller than the reduction in the tax rate. As a percentage of the value of the property school taxes went down by the full 30%. However, the value of the property increased slightly so the nominal dollar tax cut was smaller than 30%.

Tax Capitalization and the Assessment Growth Cap

In the simplified example above we ignored the effect of the assessment growth cap on the individual parcel. Under "A," the assessment cap would prevent much of the increased value from being taxed, until sold. However, the increased value could be tapped by a home-equity loan, a mortgage refinancing, or simply become part of the wealth of the homeowner.

Baseline Assumptions

The revenue projections were generated by an economic model developed by the author for the Mackinac Center for Public Policy. The model differs from the standard, "static" models commonly used in government agencies, in that it attempts to estimate the actual dynamic behavior of individuals when confronted by changes in tax rates.

The baseline assumptions [48] for current law include:

SEV growing 9.7% in 1993 (coming off the "freeze" during 1992), 5.8% in 1994, and 6.5% annually in the succeeding years;

New construction accounting for 2% of SEV growth annually;

Millage rates which continue to grow under current law; and

An assumed state reduction in "Homestead" or "Circuit Breaker" Income Tax Credits of 14% of the gross property tax reduction.

Legislative and Local Government Assumptions

The model does not assume that any other companion tax reduction legislation will pass, beyond that necessary to implement "A." In particular, it does not include Senate Bill 146, which would create a one-year lag in assessments in 1994. This is a key difference between this independent study and the "consensus" revenue estimates adopted by the staffs of the Department of Treasury, Senate Fiscal Agency, and House Tax Committee.

School millage rates have been increasing under current law and indeed are a major justification for the proposal. As discussed in the text. the proposal would probably result in more taxpayer control of school finances, and slower-growing millage rates. Nonetheless, to make the tax-reduction projections more conservative, school millage rates were assumed to grow at 3/10 a mill each year through 1995 under the proposal, 50% faster than the 2/10 a year rate assumed under current law.

Dynamic Effects

There are three explicit dynamic effects in the model. The first is tax capitalization, discussed at length in Appendix II. A provisional tax cut is calculated, using a simple static analysis. The provisional tax cut is then capitalized, by multiplying it by the capitalization ratio. This capitalizedtax cut is then added to the baseline True Cash Value (TCV), and, multiplied by the assessment ratio, becomes the (unlimited) SEV for the "A" projection. This SEV will be larger than for current law, so the gross tax cut – the difference between current law and projected tax revenue – will be smaller than a static analysis would indicate.

The second area of dynamic influence is the projection of additional tax revenue from other taxes, on additional disposable income left from the property tax cut. A fraction of this is assumed to be taxed, after incorporating the avoidance factor for the sales and use taxes. The third dynamic effect is the tax avoidance behavior of consumers.

Assumptions for dynamic effects in the model include:

Turnover (sales of property) of 10% a year.

School millage rates which grow faster under "A" than under current law for the first few years, both because of fewer "Headlee" rollbacks, and the possibility that school districts would attempt to regain some of the reduction in millage.

Tax avoidance by Michigan taxpayers, who are assumed to reduce their tax payments by 1/10th the proportional increase in the sales and use tax rates. This "elasticity" is assumed to the 2/10 in 1993, when consumers could easily accelerate purchases of big-ticket items to avoid the sales and use tax increases.

A Capitalization Ratio of 8, equivalent to about an 12% cap rate.

The capitalization ratio, tax elasticity, and other dynamic factors used in the model are conservative. A full dynamic model would attempt to include changes in employment, investment, and other factors, and would likely generate larger dynamic changes than those indicated here.

SEV Algorithm

The assessment growth cap presents a difficult modeling problem. The algorithm used here to project SEV under the assessment cap works as follows:

An unlimited SEV series is created, based on the True Cash Value, as augmented by tax capitalization.

A share of the current year SEV, equal to 1/T where T = the turnover period, is calculated as equal to the same share of unlimited SEV. This accounts for the newly sold parcels.

The remaining (T-1)/T share is projected from last year's SEV, by adding new construction and increasing it at the limited rate.

Aggregation Problem