Few issues are more emotional and controversial than how states care for children who are removed from families because of neglect, abuse or abandonment. This extensively documented report finds that it is less costly to place children in foster care supervised by private agencies than for this service to be provided by Michigan's Department of Social Services. Privatization of this important social service serves as a model for other states. 16 pages.

An earlier version of Child Foster Care in Michigan: A Privatization Success Storywas produced in 1991 under another title by the Michigan Federation of Private Child and Family Agencies and authored by Charles D. Van Eaton and Gary L. Wolfram. Upon examination of that manuscript, The Mackinac Center for Public Policy confirmed its essential findings and felt that the information therein was worthy of updating and providing to a wider audience. At the initiative of Mackinac Center analyst Mark Michaelsen, additional data and insights were incorporated to yield this final version. We thank the Federation for its original work and for its commitment to policies which enhance the quality of life for the children of Michigan.

Municipalities all across Michigan are experimenting with privatization of many types of local services, from trash collection to law enforcement. Led by Michigan Governor John Engler, state government is also pursuing opportunities for privatization. This extensively documented 16-page study of privatization of child foster services in Michigan marks the Mackinac Center for Public Policy's first analysis of family and social issues.

Few issues are more emotional and controversial than how a state cares for children who are removed from their families because of neglect, abuse or abandonment. The Mackinac Center study finds it is less costly for Michigan taxpayers to place children in foster care environments supervised by private agencies than for this service to be provided directly by the state Department of Social Services (DSS). The vast majority of Michigan private child care agencies deliver care at a rate lower than the $21.82 daily per child cost of DSS child foster care service provision.

But cost alone should never be the sole criteria by which private foster care is judged. Most national child care accreditation agencies recommend child-to-worker ratios of 25:1. It is well documented that DSS continues to fall well short of this ratio, while private agency ratios currently range from 19:1 to 23:1. Using this measure, Michigan taxpayers are receiving more foster care supervision at a lower cost through private agencies than through direct DSS supervision of foster care placement.

Private agency provision of child foster care services is a privatization success story. From 1981 to 1991, the number of children placed in foster care for reasons of abuse and neglect rose 62%. During this time, the number of children supervised by private agencies rose 200%. In 1991, private agencies provided services to 65.6% of such children.

But public policy decisions, such as continued use of private contractors to supervise the majority of child foster care placements, are not merely a matter of economics; politics also plays a major role. The Mackinac Center authors use a "public choice" model of government behavior pioneered by James M. Buchanan, recipient of the 1986 Nobel Prize for economics, to explain the process by which many interests, including those of taxpayers, collide to shape policy decisions.

Municipalities all across Michigan are experimenting with privatization of many types of local services, from trash collection to law enforcement. Led by Michigan Governor John Engler, state government is also pursuing opportunities for privatization.[1]

During the past decade, many analysts have examined how privatizing government services can reduce costs to taxpayers and improve the effectiveness of services.[2] Methods of privatization studied have included selling government assets, allowing private firms to compete with government, and contracting with private groups to provide services.

When government has a compelling interest in the provision of a certain type of activity, contracting with private providers is often the best privatization option. In most cases studied, analysts have found contracting both more effective and efficient, freeing up resources to meet other public needs. No one would dispute that the State of Michigan has a compelling interest in protecting the lives, health and welfare of the state's children.

Few issues are more emotional and controversial than how a state cares for children who are removed from their families because of neglect, abuse or abandonment. We find that it is less costly for Michigan taxpayers to place children in foster care environments supervised by private agencies than for this service to be provided directly by the state Department of Social Services (DSS). The vast majority of Michigan private child care agencies deliver care at a rate lower than the $21.82 daily per child cost of DSS child foster care service provision.

But cost alone is not the only criteria by which private foster care is preferable to public provision of foster care. Not only is the rate paid to private foster care agencies by DSS lower than our estimates of DSS in-house care per child, private agencies also provide a lower child-to-staff ratio than does DSS, an important measure of quality of service. Most national child care accreditation agencies recommend a child-to-caseworker ratio of 30:1, which is also DSS's stated staffing goal. However, it is well documented that DSS continues to fall well short of this ratio, while private agency ratios currently range from 19:1 to 23:1. Using this measure, Michigan taxpayers are receiving more foster care supervision at a lower cost through private agencies than through direct DSS supervision of foster care placement.

Private foster care has often been characterized as more caring, therapeutic and effective than public care. In some cases, although not all, this is probably true. This contention finds some support in the recent University Associates study of the Families First initiative, in which family preservation services are delivered to families whose children are judged at high risk of out-of-home placement.[3] While this paper examines the Families First program, the uniqueness of the initiative's partnership of public and private resources does not lend itself well to a comparison of public and private foster care provision.

Application of purely economic analysis suggests private care's clear superiority over public child foster care services. As a result, DSS officials and judges have placed an increasing share of the state's neglect/abuse wards in foster homes supervised by private caseworkers. From 1981 to 1991, the number of children placed in foster care for reasons of abuse and neglect rose 62%. During this time, the number of children supervised by private agencies rose 200%. In 1991, private agencies supervised 65.6% of such placements. This is a remarkable privatization success story.

But public policy decisions, such as continued use of private contractors to supervise the majority of child foster care placements, are not merely a matter of economics; politics also plays a major role. Use of a "public choice" model of government behavior pioneered by James M. Buchanan, recipient of the 1986 Nobel Prize for economics, can help explain the policy process. Buchanan's contribution to the science of economics is his leadership of a school of study, often called the "Virginia School," which views public policy as a market in which interest groups compete to maximize their benefits.[4]

In this paper, we briefly describe Michigan's system of foster care supervision. We explore how one should properly analyze the costs of government provision of a service, and examine the cost of DSS-provided foster care compared to the rate DSS pays private agencies to provide similar services. We examine alternatives to foster care, such as family preservation initiatives. Finally, we outline a public choice model of the public decision process regarding privatization in general and privatized child foster care in specific.

In Michigan, children are removed from their natural homes and brought under the care of the State only after a series of legal steps have been taken to ascertain what is best for a child. If DSS and court officers determine that the needs of the child cam best be met by removing the child from his or her natural home, the child will be assigned to a setting where protection, oversight and counseling cam be best provided.[5]

When a decision has been made to remove a child from his or her home, DSS has the authority to exercise several options: 1) regular foster care; 2) specialized foster care; or 3) institutional care. Regular foster care covers placement in a family foster care home of a child who, in the judgment of DSS, does mot require intensive services by either the foster family or the supervising agency. Specialized foster care is for children with more serious adjustment problems who are judged to need intensive intervention short of what would be provided in the more costly and restrictive institutional care setting.

In both types of foster care, the child and the foster family are serviced by a professional caseworker. This caseworker may be am employee of DSS or a private foster care agency. DSS has administratively defined "specialized foster care" so that it applies only to specialized care that is provided by private child-placing agencies. Amy care provided through direct DSS casework service is classified by DSS as "regular foster care," even if the child is receiving specialized services and the foster family is being compensated at the specialized care rate.[6]

When the needs of the child indicate that placement in a foster home rather than am institutional setting is appropriate, DSS cam either assign the child to a local DSS case-worker or to a private child-placing agency. Except in the Family Assignment System in Wayne County, where foster care cases are assigned on a rotating, random basis to participating private agencies and DSS, the local DSS office has complete power to exercise its own discretion regarding assignment.

Private child-placing agencies which administer regular and specialized foster care receive daily reimbursement rates for each child in their care as specified by DSS under terms of a contract. The rate pays for the casework services of the private agency and is separate from the compensation paid to the foster care family.[7] These rates are determined by DSS based, in large part, on the agency's cost of providing the service.

In setting the rates, DSS monitors and processes private agency fiscal reports and communicates standards and guidelines for rates through its Cost Schedule Instruction Manual Bulletin. Reimbursement rates are established and paid only after cost figures have been audited and verified, maximum number of days' care have been established, and adjustment of costs to reflect price level changes have been determined. (Michigan standards and guidelines closely mirror federal standards, promulgated by Office of Management and Budget for U.S. government contracts with private agencies through OMB Circular A-122.[8] The federal standards are a primary addendum to the state bulletin.)

To avoid excessive rate increases, DSS may limit growth of daily payment rates. DSS also reserves the right to monitor the accumulation of large amounts of cash and other liquid assets by providers to assure that rate increase requests from private agencies are not the result of "having used their cash reserves to increase program expenditures substantially through the use of large reserves of cash or other liquid assets without prior contractual agreement with DSS."[9] This mechanism assures that requests for rate increases represent only necessary reimbursement for legitimate services.

Private agencies have been an active part of Michigan's child care system for many years. Through contracts, DSS has taken advantage of the skills which these agencies have to offer. In fact, state law obligates DSS to purchase foster care services from private agencies to meet children's needs unless "licensed and caring institutions or placement agencies are not available" or there is a religious conflict.[10]

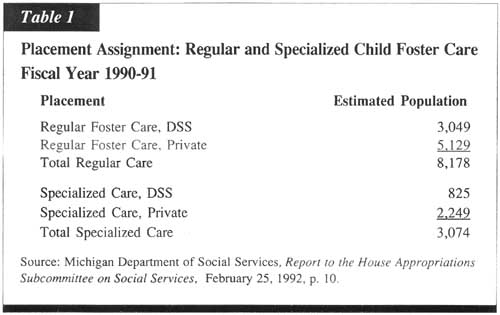

Table 1 indicates that in Fiscal Year (FY) 1990-91, 63% of children in regular foster care were managed be caseworkers in the private agency sector, and 37% by DSS public sector caseworkers. In addition, the private child and family services agencies were responsible for 73% of the children in specialized foster care. In all, private agencies supervised 65.6% of the 11,252 state neglect/abuse wards in Fiscal Year 1990-91.

The share of state wards placed in foster care arrangements supervised by private agency caseworkers grew dramatically during the decade from 1981 to 1991. In 1981, 44% of these children were served by private caseworkers. The decade also saw a 200% increase in the number of children removed from their natural homes due to abuse and neglect. The number of children supervised by DSS employees remained static, while the number of children supervised by private sector caseworkers increased by more than 62%.[11]

After reaching its highest point at 11,310 in April, 1992, the number of children in foster care for neglect and abuse subsequently declined slightly every month for the next nine months. In January, 1993, 10,459 children were in out-of-home placements for reasons of neglect and abuse.[12] This downward trend continues, partially as the result of the family preservation initiatives discussed in Section V below.

How long a child remains in out-of-home foster care depends on a number of factors, including the seriousness of problems in the child's home, a child's emotional and behavior problems, and adoption rates. The average length of time neglected children had been in the foster care system was 30 months as of October l, 1983, and 28 months as of October 1, 1989. The average length of time neglected children had been in their current placements was 18 months as of October l, 1983, and 16 months as of October 1, 1989.

Although the average duration for all placements has declined slightly, children under age 6 are entering the system at much higher rates than is true for other ages. The total number of children in the foster care system increased by 52% from October l, 1983, to October 1, 1989, with the increase in those ages 0-6 increasing 75%; ages 7-11, 48.5%; and ages 12 and over, 36.1%. Moreover, African-American and female children are entering the system at much higher rates than males or children of other races.[13]

Nearly half (47%) of the children currently in specialized foster care had a prior foster family placement, and 37.6% of the children in regular foster care also had a prior foster family placement. However, while 22% of the children in specialized foster care had a prior institutional care experience (suggesting that at the point of first protective intervention by DSS they were judged to be too difficult to benefit from foster care), only 4% of the children in regular foster care had previously been placed in institutional care before their current foster care placement.[14]

Because intensive institutional care is used almost exclusively for the most aggressive, emotionally troubled and older children, specialized foster care has become a substitute for institutional care and has placed new pressures on the system. Some would argue that the recent increase in the use of specialized foster care as an alternative to the far more expensive and restrictive institutional care system – an increase dictated by the changing profiles of many children – may explain why children are not moving more smoothly from foster care placements to permanent homes.

In 1989, the National Council on Crime and Delinquency conducted an extensive study of Michigan's foster care system. The study included a survey asking both DSS and private agency caseworkers what had contributed to the rise in specialized foster care caseloads. Both sectors said that children's problems are now far more severe and families are more dysfunctional than in the past. In this context, it was generally acknowledged by survey respondents that, even though children placed in specialized foster care are similar to those placed in institutional care in the past, foster care can, if properly managed, offer appropriate services at costs much lower than in a public or private institutional care setting.[15]

Providing foster care services is an extremely stressful undertaking for personnel in both public and private sectors and at all levels of service delivery, from front-line licensed foster care families through top-level administrators. Foster families face daily stresses related to the special needs and behavior problems of children entrusted to their care. They also face problems related to state regulation and licensing. Undocumented or even anonymous allegations by neighbors, natural parents or other individuals can result in the rapid, even overnight, transfer of foster children to another provider and/or revocation of a foster care license. The frequency of such actions is accelerating. One DSS official told the Detroit Free Press that in all of 1992, there had been about 90 such actions, while the department had proposed 110 such actions in the first quarter of 1993 alone.[16]

While the state has a compelling interest in weeding out poor providers and protecting children from abuse or neglect in foster homes, legal fees associated with fighting spurious charges are often beyond the reach of foster families, and the upheaval caused by frequent displacement of foster children is detrimental to continuity of care. Because of such stresses, approximately 25% of Michigan's estimated 7,700 foster families leave the system annually, to be replaced by new licensed foster families.[17]

Similar stresses face DSS foster care workers. In 1990, several county-based social workers testified to the House Appropriations Subcommittee on Social Services that their excessive workloads make it impossible to provide sufficient care and supervision to foster care children. One county DSS director told committee members that several case-workers on her staff had asked for demotions to clerical positions because they couldn't handle casework demands.[18]

Top DSS officials responsible for foster care and budget administration understand these problems and are trying to remedy them. In 1990, DSS confirmed the frustrations expressed by county-based DSS foster care workers. DSS reported that movement of staff out of foster care was too high. From October 1, 1988 to February 3, 1990, Wayne County lost 38% of its staff (60 of 157), and DSS suffered a statewide 28% loss in staff (100 of 359). In addition, foster care licensing reports indicated problems in the quality of service due to heavy workloads – monthly visits to children in foster care were not always made – and service plans and reports were late, incomplete or poorly done.

There have, of course, been widely publicized, even tragic, problems in child foster care service delivery.[19] These are not exclusively the fault of state government, the judicial branch, or private child care agencies, but are chiefly the result of conditions which now present the system with many children whose problems are often far more complex and intractable than previously.

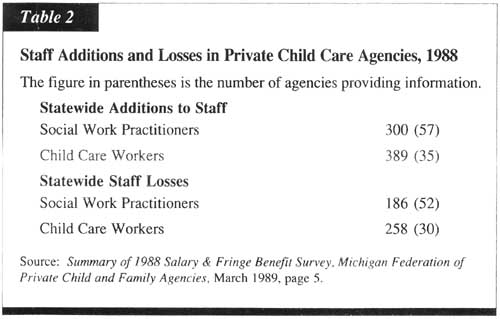

Table 2 indicates that private agencies have also had significant staff turnover.

However, despite staff losses during the time period studied, private sector agencies experienced net increases in staff available to provide direct field services in foster care. Overall, private agencies added 114 new social work practitioners and 131 new child care workers. By contrast, DSS suffered a net loss in field staff serving foster care cases. A loss of trained staff continues to plague DSS.

Further increasing the number of children supervised directly by DSS would require a substantial increase in staff and a concerted effort to reduce staff turnover to provide adequate care and attention to children in foster care. In 1990, DSS noted that its goals for family and child services staffing ratios are 30:1 (clients/staff) when services are delivered by DSS employees; 90:1 when services are directly purchased from private agencies; and 100:1 when services are licensed to private agencies.[20]

Historically, the 30:1 goal has proved elusive. In 1989, DSS reported to private agencies that DSS needed 432 more staff to meet the 30:1 objective. By 1990, the shortfall in the number of staff needed grew to 507.[21] As recently as November, 1992, DSS was still 159 employees short of its 30:1 target.[22] Public child foster care in Michigan has thus consistently failed to achieve the 25:1 caseload ratios considered optimal by most accreditation agencies.

|

Meeting the 30:1 Ratio Standard |

|

|

The DSS staff number increase required to meet the optimal 30:1 ratio: |

|

|

1989 |

423 |

|

1990 |

507 |

|

November 1992 |

159 |

On the other hand, most private agencies met or exceeded both the 30:1 and 25:1 ratios during 1989 and 1990.[23] More recent analysis of private agency caseloads indicate a current ratio of from 19:1 to 23:1 in regular foster care and from 12:1 to 14:1 in specialized foster care.[24]

There is also an important intangible aspect to private provision of child foster care services. Many private agencies view their participation in the system as a "ministry." Periodic revenue shortfalls have often been absorbed by these agencies when state reimbursements have failed to fully cover costs. Unreimbursed costs have not caused such agencies to refuse children. Instead, new placements have been financed out of private donations and, in some cases, income from carefully managed endowments.

Over the past eight years, no fewer than six blue-ribbon panels have studied Michigan's foster care system and made recommendations for improvements.[25] Legislators, judges, child welfare advocates and public and private caseworkers are committed to providing services to meet the special needs of neglected and abused children without having to revert to the old pattern of regular foster care or institutional care with no viable option in between. Despite the levels of frustration and turnover rates, public and private sector child care workers believe the foster care system can be improved.

Most regular and specialized foster care is now contracted by the State to private agencies. As noted above, private agencies service 63% of regular foster care placements and 73% of specialized foster care placements. This partnership has been in place for decades, and private agencies are continually adding, training, and motivating professional staff to meet the new challenges faced by children with more difficult needs. Nevertheless, an argument has surfaced that foster care is not working, that it is too costly, and that the state can better address social problems by removing private child care agencies from the process and directing funds toward alternatives to foster care. This argument is often advanced most vigorously by public sector union representatives.

Could the state save money by removing the private sector from the foster care process, freeing up funds for alternative programs? This requires us to answer two questions. First, what does it cost for the state to provide child foster care and how does that compare to private agency payment rates? Second, to what extent is foster care a needed part of any care continuum?

Economic principles tell us nothing is produced for free, including government programs. What it costs to deliver a bottle of milk, for example, and what it costs to deliver a government program have one thing in common: they both absorb scarce economic resources. A dairy company which fails to fully account for a) labor costs, including all fringe benefits and b) capital costs, including the value of foregone interest income when funds are sunk in machines, tools, and equipment, will eventually face bankruptcy. Similarly, failure to account for the same type of costs absorbed by one government agency will, in the face of public resistance to tax hikes, eventually result in either denial of scarce resources to other equally important government services, or a reduction in the quality of services.

In the production of foster care services, what costs must be measured by private and government child care agencies?

DIRECT COSTS

These include salaries, supplies, transportation expenditures (if the caseworker uses his or her own vehicle and is paid a mileage rate), telephone and fax charges, postage, printing and other charges for which specific invoices exist and can be clearly noted and assigned to particular activities.

INDIRECT COSTS

These include so-called "overhead costs" – especially costs such as fringe benefits and accrued pension liabilities and insurance – which are not immediately identifiable and assignable for specific services. Private firms use accounting systems that discover, count and assign such charges to specific activities. Failure to discover and assign overhead costs would leave a private firm in the dark, making it impossible for the firm to know if it should do certain things directly and "in-house" or hire someone else to do it for them. Firms "outsource" when they discover that a job can be done better or for less by paying someone else to do it for them.

Governments should do the same thing. One problem with the accounting procedures used by governments, i.e., "fund accounting," is that overhead costs are often not precisely assigned to specific agencies and activities. Government overhead costs are usually kept in separate budget accounts and are therefore difficult to count and assign. To determine whether or not it is appropriate to contract out a government program or have it done in-house, overhead costs should be discovered and assigned to every government agency which performs a public service task.

CAPITAL COSTS

Virtually no government agency fully accounts for the value of physical capital used in performing the agency's services. Private firms, since they must over the long run receive revenues in excess of all their costs, do account for the depreciation of their capital.

Property and equipment used in providing a service or producing a good should be depreciated, and the full opportunity cost of capital should be measured. Explicitly or implicitly, private firms determine the return that capital could earn in its next best alternative use, along with the expected useful "economic" life of the project. The application of this concept to capital equipment generates information which tells firms whether or not funds should be invested in machines and equipment and if they should be rented rather than purchased.

Governments act as if they have no use for this concept.[26] Under usual government accounting procedures, capital costs are normally charged as a capital outlay expense in the year of purchase. The total purchase cost is assigned as an asset to a General Fixed Asset Group, and the depreciation costs of these assets (even if some effort is made to charge depreciation costs) are not included as a cost for performing a specific project. Therefore, the full value of capital absorbed by a specific agency or project will never be fully discovered and assigned, and the actual capital costs of providing a yearly service will never be fully known.

Government, including the State of Michigan and DSS, does not track function-specific costs the same way a private agency does. This is not to say that government operates dishonestly, but rather to say that the usual accounting procedures used by all levels of government are not specifically designed to allocate costs by agencies and by specific activities within agencies.

Somewhat ironically, all private, nonprofit child and family services agencies that provide social services under contract with DSS must account for and assign all costs. Unlike government, private agencies do not have the power to levy taxes. Nor do they have access to credit markets in the same manner as do governments. Therefore, their revenues must cover all their costs. If private agencies didn't know all their costs at every moment in time, they would be operating in the dark and, sooner or later, they would be forced to close. In that respect, private, nonprofit agencies have something in common with private, for-profit firms which neither has in common with government: they can go bankrupt.

Because accounting systems for private agency placement services and for DSS placement services are different, one cannot answer the first question posed earlier – what does it cost the state to do the job compared to what it costs to have the private sector deliver the same services? The best way to do this is to attempt to hold con-stant the level of service being provided and account fully for all costs – then comparing apples to apples and oranges to oranges.

As is the case with many government services, there is no clear measure of output for foster care supervision services. The quality of the caseworker's advice, his or her ability to interact with the children and their foster families, and other types of activities are very difficult to measure. The best we can do is to presume that, on average, caseworkers employed by the private sector will be as successful in providing these services as case-workers employed by DSS. We know of no claims to the contrary. Indeed, because private agencies must compete for contracts with one another and with in-house DSS supervision, failure to provide adequate service can result in elimination of contracts. There is direct market feedback to the private service provider as opposed to indirect feedback for government provision of services. Thus, we accept equal service levels for equal inputs as a reasonable assumption.

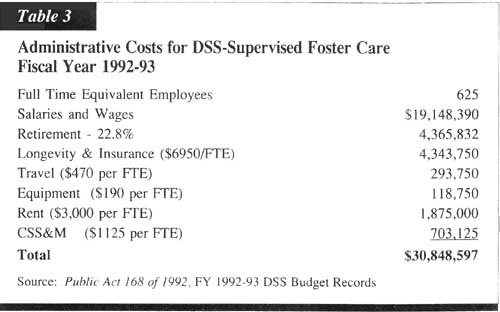

Table 3 provides aggregate budget data on current DSS-supervised child foster care for Fiscal Year (FY) 1992-93:

The estimated average salary DSS foster care workers will receive in FY 1992-93 is slightly more than $30,600. Retirement costs are anticipated to be an additional 22.8%, or approximately $6,985, with longevity and insurance an additional $9,950 per worker. Thus, total compensation per worker is approximately $47,535. This presumes that retirement benefits are fully funded out of current revenues allocated to the DSS. If they are not fully funded each fiscal year, then at some point in the future, as DSS employees retire, the State will have to divert funds from other programs to meet pension obligations.

In Table 1 above, we said there were 3,874 children in DSS-supervised foster care placements in FY 1990-91. Although this number fluctuates from year to year, it provides a useful starting point for economic analysis. Multiplying 3,874 children by 365 days yields 1,414,010 days of care per year. Dividing the current DSS foster care budget of $30.8 million by days of care yields a DSS administrative rate of $21.82 per day. That is, DSS has an in-house cost of at least $21.82.

Private child care agencies know exactly what it costs them to produce foster care services. DSS also knows what it costs the private sector to do the job. In the DSS Cost Schedule Instruction Manual Bulletin, we find the following:

"Each child-caring agency which provides service to youth under agreement with DSS and/or provides services to court wards is required to provide cost information annually to DSS using Cost Schedule Forms DSS-573 and DSS-573A." Furthermore, "The agency's Financial Audit Report is to include a statement of functional expenses as required by industry audit guide on 'Audits of Voluntary Health and Welfare Organizations.' The Report is also to include an expressed opinion on paid days of care and adoption contact hours/or placements if applicable." The agency is required to maintain records of equipment purchase, daily attendance reports, staff payroll records and time sheets, and other information as outlined in the manual.[27] In addition, DSS retains the responsibility to monitor and process fiscal reports in this purchase of services system, and after the cost schedules have been returned to the department, only then will a per diem rate be established for any foster care agency, regardless of the department's intent to purchase from the agency.

Strict controls – as indeed should be the case – are exercised by DSS on rates paid to private agency services. Indeed, one could argue that DSS has a tighter hold on what it costs to contract for foster care services from a private agency than on what it costs to have the work done "in-house."

When DSS examines the costs incurred by private agencies to supply foster care services, a daily "administrative rate" is determined. This is the payment received by the private agency. The DSS Services Manual Bulletin of March 1, 1993, provides administrative rates paid to private agencies for various programs in the current fiscal year. Fifty-one of the private agency programs are paid an. administrative rate of less than the $21.82 calculated for DSS-supervised care for FY 1992-93. Of those paid a rate above $21.82, nearly all are supervising specialized foster care or providing intensive institutional services.

Only four agencies that receive more than $21.82 are not also providing institutional care, managing semi-independent living or supervising difficult children. These are Area Youth for Christ in Battle Creek at $31.29; Child and Family Services, St. Joseph at $33.38; Camp Highfields in Onondaga at $37.45; and Sault Ste. Marie Tribe Binoji Place-ment Agency at $30.70. These agencies may also be supervising difficult youths, but this is not indicated by the DSS Services Manual.

In our effort to compare apples to apples, we have discovered that the administrative rate paid by DSS to private agencies is lower than what DSS spends for in-house care. In fact, since we presumed equal inputs result in equal outputs, private agency placement is even less costly to taxpayers than our estimates show. This is because private agencies have a lower child-to-staff ratio than DSS.

Because most of the children under DSS supervision are placed in regular foster care, it is appropriate to compare the daily administrative rate paid for regular foster care supervision to the DSS in-house estimate. As we have noted, the administrative rate paid to private agencies is clearly less than even our lower estimate for DSS in-house costs. There are at least two obvious explanations for this. One is that at least some private agencies receive donations or have endowments that allow them to subsidize care. The second has to do with labor costs.

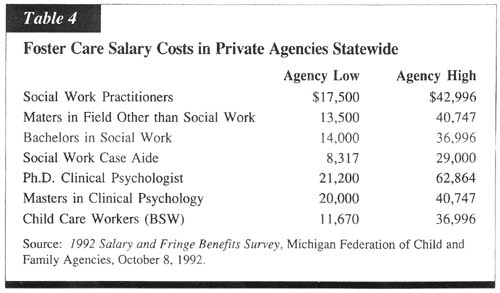

Table 4 indicates that salaries for many highly-trained people in private foster care agencies are below what the state pays its own employees.

What is the fringe benefit rate for child care staff in the private sector? In the cost schedule supplied to DSS – under rules of the DSS Cost Schedule Instruction Manual mentioned above – by one of the larger private agencies in Michigan, employee benefits represented

9.2% of salaries, and payroll taxes represented 7.2% of salaries. By contrast, as noted in Table 3 above, DSS employee retirement benefits alone represented 22.8% of payroll, and Longevity &; Insurance were charged at $6,950 per FTE. Thus, private agency labor costs are much lower than the $47,535 per DSS worker we estimated above.

If we are to compare the costs of providing a given amount of foster care supervision, then it is clear that for the same child-to-foster-care-worker ratio the private sector has lower costs – answering the first of the questions posed at the end of Section III above.

Nearly all major studies of Michigan's foster care system recommend initiatives to reduce the need for removal of children from parental homes by addressing the conditions that lead to out-of-home placements. The recommended continuum of services ranges from substance abuse counseling and employment training to remedial parenting skills instruction and more generous public assistance stipends.[28]

There is system-wide experimentation with various models of family preservation activities by both DSS (usually at the initiative of county DSS offices) and private agencies. It makes good financial sense to try to preserve families at risk of having children removed from the home due to neglect and abuse; the cost of intervention is usually much less than expensive child foster care. Earlier this year, too, seven private agencies announced their desire to deliver a comprehensive continuum of family services through a consortium called ChildNet.[29]

One such family preservation program has been studied extensively. In 1989, Michigan began experimenting with a new model of service delivery, known as "Families First." Under Families First, private agency caseworkers provide comprehensive and intensive assistance to families in which children are at imminent risk of removal for abuse and neglect. Each intervention period typically lasts from four to six weeks. A typical caseworker assigned to a Families First target family has only two active cases at a time and is on-call 24-hours, seven days per week.

A study that examined the success of Families First found that intensive intervention resulted in 16.6% fewer removals of children from natural homes for neglect/abuse 12 months after intervention, with similar results three and nine months after intervention. Ninety-eight percent of program staff, DSS and court workers who referred cases to Families First, and families who received services rated the program as either effective or extremely effective.[30]

It is more expensive to provide such intensive services ($1,936 per child) relative to foster care in the short term, but in the long run the potential cost savings from avoiding foster care placements altogether are dramatic. The University Associates' Families First evaluation concluded if 75% of at-risk children were referred to Families First, the savings to the state from foster care placement reductions could reach $36 million.[31]

But even with extraordinary efforts to preserve intact families, some home environments cannot be rendered safe from neglect and abuse of children. Even after Families First referral and intervention, 19.4% of children served by Families First still needed to be placed in foster care.[32] Thus foster care remains a crucial part of any services continuum – answering the second of the questions posed at the end of section II above.

Will Michigan's successful use of private child care agencies to care for the majority of the state's neglect and abuse wards continue? Let us construct a model of public decision-making for privatization in general and then adapt that analysis to the question of the choice between public and private delivery of child foster care services.

In the public choice model of policy decisions, interested parties interact in political markets to shape government action in a way which maximizes their benefit. Manipulating policy is especially important to those who benefit from government programs and who may seek to expand employment opportunities, obtain higher payment rates or bar competitors from the market.

In such a political market, there is a battle for public "share of mind," the definition for market share in our public choice model. All actors seek to influence public opinion and legislative actions, judicial opinions and executive decisions. On the one hand, the interest of those who directly benefit from government programs tend to have concentrated power in these markets. The interest of taxpayers tends to be diluted, since the cost of any one type of government service usually represents a very small share of an individual's tax bill.

Privatization, whether for something as small as municipal trash pickup or as large as a major state program, provides an interesting case for public choice analysis. There is usually a group of parties which feel threatened by privatization because of the potential loss of economic benefit, but the interests of taxpayers and others who may benefit from privatization also compete for public share of mind. Whether privatization can be success-fully applied to any specific government activity depends on which interests prevail in this battle for market share.

Current state policy makers in Lansing support continuing the use of private child foster care agencies to provide services to a large share of children removed from their natural homes due to abuse and neglect. These decision makers include Governor Engler, key state legislators, judges, and DSS Director Gerald Miller. At this time, private child care agencies service more than 60% of child foster care placements. In a public choice model, the interests of taxpayers are best served by continuing to pursue privatization of foster care. Private child care agencies deliver the best care at the lowest price, state decision makers agree.

However, an interesting aspect of competition in the debate over privatization into new activities is spillover of the terms of debate in these new areas into some activities where privatization of services is already well established. Interest groups such as DSS employees, public sector union representatives, and other beneficiaries of public child foster care provision all stand to gain from a reversal of current policy if they can offset private providers' share of public mind.

However, we have demonstrated that it is clearly more cost-effective to taxpayers for child foster care services to be delivered by private agencies. In the face of tight budgets and understaffed state programs, rejecting the services offered by private agencies in the name of "saving money" carries with it the grave risk of not only not saving money, but also of not saving children.

Charles Van Eaton, Privatization: Theory and Application for Michigan, (Michigan State Chamber of Commerce Foundation), June, 1988.

See, for example, E.S. Savas, Privatizing the Public Sector (Chatham, NJ: Chatham Housc Publishers, Inc.), 1982; James Bennett and Manuel Johnson, Better Government at Half the Price (New York: Kapman and Company), 1981; and The Role of Privatization in Florida's Growth, (Florida Chamber of Commerce), 1987.

Evaluation of Michigan's Families First Program Summary Report, University Associates, March, 1993.

Public choice scholarship takes its alternative name, the Virginia School, from Buchanan's long service on the faculty of three Virginia Universities: the University of Virginia (1956-62), Virginia Polytechnic Institute (1969-83), and George Mason University (1983-present). Interestingly, the University of Michigan Press has played a leading role in catapulting public choice theory into academic prominence, publishing three of the most important collections of papers on the subject. See J.M. Buchanan and Gordon Tullock, ed., Calculus of Consent, University of Michigan Press, 1962; J.M. Buchanan and Robert D. Tollison, ed., The Theory of Public Choice, University of Michigan Press, 1972; and J.M. Buchanan and Robert D. Tollison, ed., The Theory of Public Choice-II, University of Michigan Press, 1984.

Michigan Compiled Laws Annotated (MCLA), Sec. 400.1 et seq. See also MCLA 722.111 et seq.

Ibid. For administrative rules, see Michigan Administrative Code R400.23 et seq.

Cost Schedule Instruction Manual Bulletin, Michigan Department of Social Services, No. 91-1, pp. 3-4. Selected pages of the bulletin were updated by Cost Schedule Instruction Manual Bulletin, Michigan Department of Social Services, No. 93-1, but these amendments do not effect any citations in this paper.

Office of Management and Budget Circular A-122, "Cost Principles for Nonprofit Organizations," June 27, 1980.

Cost Schedule Instruction Manual Bulletin, No. 91-1, op cit, p. 8.

MCLA 411.18c.

Information Packet, Michigan Department of Social Services, March, 1992, p.43.

"Families First Evaluation Released," press release, Department of Social Services, May 10, 1993, pp. 3, 7.

Department of Social Services, Report to the Michigan House Appropriations Subcommittee on Social Services, March 1, 1990, pp. 17-18.

Foster and Residential Care in Michigan: A Descriptive Study of Children in Placement, The National Council on Crime and Delinquency, April, 1989, p. 4.

Ibid, p. 20.

"Foster Parents Walk a Fine Line," Detroit Free Press, March 26, 1993, p. B 1.

Ibid.

"Burdened Social Workers Tell Panel Heavy Caseloads Jeopardize System," Flint Journal, March 2, 1990, p. A2.

"A Meeting of Victims Ends in Tragedy," Detroit Free Press, April 3, 1993, p. 1A.

Report to Michigan House Appropriations Subcommittee, op cit.

Michigan Federation of Private Child and Family Agencies memorandum, January, 1989.

Joan Abbey, A Chorus: Themes for Michigan's Child Welfare System, Skillman Foundation, January, 1993, p. 9, note 36.

Michigan Federation of Private Child and Family Agencies memorandum, op cit.

Donald J. Austin, Jr., Summary Report on Federation Financial Data Base, April 12, 1993.

See Abbey, op cit., for an in-depth examination of the commonality of these studies' recommendations.

For further discussion of public-private accounting differences, see Brian Cromill, "Explaining the Infrastructure Crisis," Federal Reserve Bank of Cleveland Quarterly Economic Review, 2nd Quarter, 1989.

Cost Schedule Instruction Manual, No. 91-1, op cit, pp. 6-7.

Abbey, op cit, pp. 2-7.

"Rethinking Foster Care," Detroit Free Press, February 2, 1993, p. 3A.

Evaluation of Michigan's Families First Program Summary Report, op cit, pp. 4-7. s'

Ibid, pp. 12-15.

Ibid, p. 11.

Mark G. Michaelsen is a Lansing policy analyst and writer with a long record of service in government and education in Michigan and Washington, D.C. Michaelsen received a B.A. with Honors from the University of Wisconsin in Madison, where he studied economics and political science. He has written for policy journals and national magazines of opinion.

Charles D. Van Eaton is a widely published economist who is currently the chairman of the Economics Department at Hillsdale College and a member of the Board of Directors for the Mackinac Center for Public Policy.

Gary L. Wolfram is a professor of Economics at Hillsdale College and a Senior Policy Analyst for the Mackinac Center for Public Policy. Wolfram is also a former Deputy Director of the Department of Treasury for the State of Michigan.