By Jack McHugh

By Jack McHugh

Most informed Michigan citizens know that the revenue cap imposed by the 1978 Headlee constitutional amendment limits state spending, taxes and fees. What these same Michiganians probably do not know is that the Headlee limit looks increasingly unlikely to restrain the growth of state government.

Passed in the midst of a nationwide tax revolt, the Headlee constitutional amendment established that "the legislature shall not impose taxes of any kind which, together with all other revenues of the state, federal aid excluded, exceed" 9.49 percent of the aggregate personal income of Michigan citizens in any given year. If revenues overrun the limit by 1 percent or more, the state must prorate and rebate the "overcharge" back to every person who paid personal income or business tax in the previous year.

The revenue cap in dollar terms has risen as personal income has grown. Some of that is due to inflation, but much of the increase has a happier cause: Our society and most families are wealthier now. Given the presence of a mostly free-market system and the rule of law, this is not surprising. Despite attacks from those who hate or resent these institutions, history shows that when allowed to flourish, free markets and the rule of law always create more wealth and distribute it more widely.

There is lots of direct and indirect evidence for this. For example, the increasing wealth of most families can be seen in homeownership rates. In Michigan, even in its current economic malaise, 77.1 percent of households owned their own home in 2004, up from 70.7 percent 20 years ago.

For aggregate personal income growth we have direct evidence. In constant 2003 dollars, Michigan’s per-capita personal income grew from the equivalent of $24,144 in 1977, the year of the Headlee index, to $31,189 in 2003 — a 29 percent increase in real terms. Over the same period, the state’s population rose from 9.20 million to 10.08 million. These are the components that combine to determine the Headlee revenue limit.

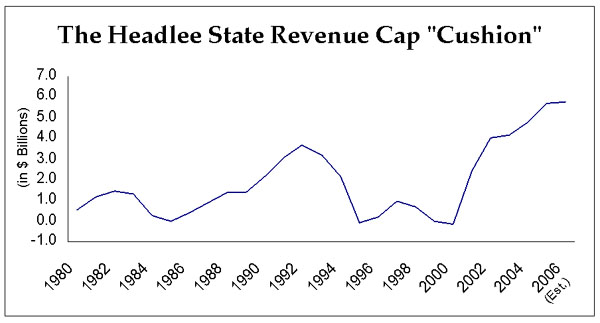

So has Headlee restrained tax and spending growth? The answer is an unequivocal "maybe." In its 26-year history, the cap was exceeded just three times, and only once by enough to trigger a rebate. In 19 of those years, revenue was at least $500 million beneath the cap, and in 15 years, that cushion exceeded $1 billion. As a result of Proposal A in 1994, $3.5 billion in school spending and revenue was shifted to the state, and still there was enough cushion to accommodate this change without triggering a rebate.

It’s impossible to definitively conclude whether this history proves the cap was just too high to be effective, or the opposite: that it held back legislators from tax and fee hikes they might otherwise have passed. The cap might have been effective in another way, too: Using personal income as the Headlee index gave the beneficiaries of government spending a stake in economic growth, possibly inhibiting the adoption of more economically damaging taxes and regulations.

Having said that, there is no question that since 2001 the Headlee cap has "run away" so far from actual revenues that it has become irrelevant. In 1980, revenues were $526 million less than the maximum amount allowed, a difference equal to 7.1 percent of actual spending. Fast forward to 2005: The revenue cap is $29.84 billion, and actual revenues are $24.16 billion. This means Lansing could raise taxes and spending by $5.67 billion, or 23.5 percent, without bumping against the cap. This would translate into a tax increase of more than $560 on every man, woman and child in the state.

Looked at another way, for the current Headlee cap of 9.49 of aggregate state personal income to limit spending and taxes by one penny, the per-capita annual income of Michigan residents would have to fall by more than $5,900 ($17,700 for a family of three). Alternatively, the state’s population would have to decline by about 1.9 million. Either scenario would be highly unfortunate.

Michigan citizens concerned about the growth of state government need to look closely at the Headlee amendment’s constitutional cap on taxes, fees and spending. Perhaps now is the time to consider a more sure-fire way to limit the growth of government — a “taxpayer bill of rights” that caps state spending growth at the rate of inflation plus population growth.

#####

Jack McHugh is a legislative analyst for the Mackinac Center for Public Policy, a research and educational institute headquartered in Midland, Mich. Permission to reprint in whole or in part is hereby granted, provided that the author and the Center are properly cited.

The Mackinac Center for Public Policy is a nonprofit research and educational institute that advances the principles of free markets and limited government. Through our research and education programs, we challenge government overreach and advocate for a free-market approach to public policy that frees people to realize their potential and dreams.

Please consider contributing to our work to advance a freer and more prosperous state.