In a "Coalition for Secure Retirement-Michigan" press release arguing against closing the school employee pension fund to new members and converting to a 401(k) plan, former head of the Michigan Senate Fiscal Agency Gary Olson argued that the state would face transition costs mandated by the Governmental Accounting Standards Board.

"Any deviation from GASB accounting guidelines could result in short-term savings but could result in a drop in Michigan's credit rating, which may increase borrowing costs for the State of Michigan and local units of government," the release stated.

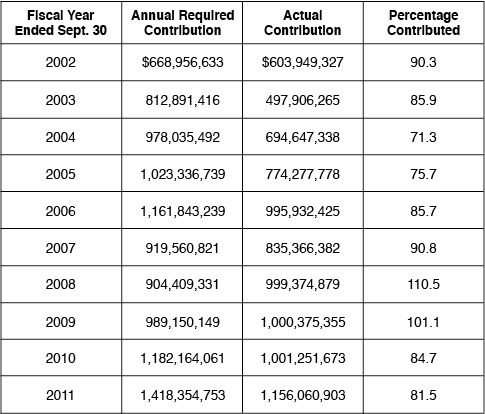

What Olson neglects to mention is that the state is in charge of setting pension funding policies and already flouts GASB standards. The table below is from state financial reports and describes the GASB required report for the Annual Required Contribution. It also shows how much the state contributed. It has only met or exceeded its GASB reporting standard in two years during the past decade.

In fact, Michigan's consistent underfunding of the school employee pension fund shows that the state ought to close its pension system.

State officials argue that timing issues impact its ability to meet these schedules. However, by converting to a defined-contribution retirement system, the state would no longer be able to pass along the uncertain costs of current benefits onto future taxpayers.

Source: "Michigan Public School Employees' Retirement System: Comprehensive Annual Financial Report for the Fiscal Year Ended Sept. 30, 2011," (Michigan Office of Retirement Services, 2011), 47, http://goo.gl/hyUcr (accessed Feb. 15, 2012).

~~~~~

See also:

Teacher Pension Underfunding Hits $22B

Taxpayers Agree: 401(k)s for New Hires

House GOP on Verge of Surrendering to MEA

Get insightful commentary and the most reliable research on Michigan issues sent straight to your inbox.

The Mackinac Center for Public Policy is a nonprofit research and educational institute that advances the principles of free markets and limited government. Through our research and education programs, we challenge government overreach and advocate for a free-market approach to public policy that frees people to realize their potential and dreams.

Please consider contributing to our work to advance a freer and more prosperous state.