Discussion of the SOS proposal in Michigan has so frequently involved TABOR and its impact on Colorado’s state budget and economy that Colorado’s experience is reviewed in some detail below. Also reviewed are the SOS spending cap’s possible effects on Michigan had the SOS proposal been in place during the past dozen years; the spending cap’s use of inflation and population; the provision eliminating pensions for legislators; and issues concerning debatable terminology in the SOS proposal.

The Colorado Economy: 1993-2001

An analysis of Colorado state spending both before and after the passage of TABOR suggests that the amendment restrained state spending growth. According to the Golden, Colo.-based Independence Institute, from 1993, when TABOR was enacted, to 2002, total state spending grew about 64 percent — more or less matching the combined total growth of population and inflation for the period. In contrast, in the decade before TABOR, Colorado spending increased nearly 90 percent — more than double the 40.1 percent combination of inflation and population.[22]

The implementation of TABOR coincided with strong economic growth for Colorado. Even after a pronounced recession beginning in 2001, Colorado’s job growth from 1993 to 2006 was nearly 38 percent, or almost 690,000 new jobs.[23]∂∂ This substantially eclipsed the 20 percent national job growth for the same period. In contrast, in the 10-year period prior to TABOR’s enactment, the nation added 19 percent to its jobs base, while Colorado added 17.2 percent.[24]

Likewise, an analysis of U.S. Census Bureau data shows that Colorado’s population increased faster than the national average following enactment of TABOR.[25] The Washington, D.C.-based Heritage Foundation also found that measures of per-capita personal income growth and per-capita gross state product show Colorado lagging the national average in the decade prior to TABOR and then significantly outperforming the average in the decade afterward.[26] From 1993 to 2005, U.S. Census Bureau figures show that Colorado’s population increased 29 percent, double the national average.[27]

Colorado’s post-TABOR economic success had many contributing factors, and it would be inaccurate to ascribe the state’s exceptional economic success to any one of them. However, the acceleration of Colorado’s economy in the wake of implementing TABOR suggests that the resulting restraint on government taxes and spending may have contributed to Colorado’s economic and population growth.

|

∂∂ Colorado’s higher rates of job growth existed prior to the modification of TABOR in 2005. The job growth rate from June 1993 to June 2005 was 32.5 percent, which was well above the national average of 17.8 percent. |

Colorado’s Post-2001 Recession

The recession that began for the entire nation in 2001 was more severe in Colorado. As noted in a 2005 Cato Institute study, the terrorist attacks of September 11, 2001, resulted in a 14 percent decline in skiing tourism that winter.[28] The worst drought in decades occurred the following year, touching off damaging forest fires and reducing both summer tourism and agricultural production. Nearly 12 percent of the Colorado workforce relies directly upon these two industies.[29]

The Cato Institute’s study also found that this sharp economic contraction contributed to a 12 percent reduction in tax collections for 2002.[30] A smaller reduction in revenue for 2003 brought the two-year total reduction to more than 13 percent. Most states experienced revenue shortfalls because of this recession, but Colorado’s was about twice the national average.[31]

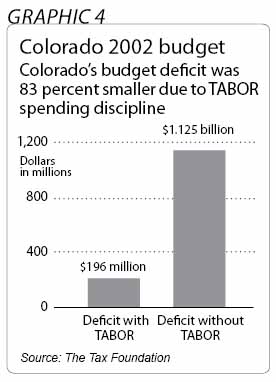

As the Washington, D.C.-based Tax Foundation has observed, the spending discipline enforced by TABOR appears to have mitigated the budgetary challenges that appeared after fiscal 2001. TABOR required a state tax rebate of about $1 billion in fiscal 2001, because revenue collection had exceeded the TABOR limit by that amount. The 2001 state budget — the last before the recession reduced state revenues — was therefore not based on spending the extra $1 billion. In 2002, when total revenues declined by more than $1 billion, the state budget faced a deficit of about $196 million — considerably less than the $1.1 billion deficit the state would have faced if the $1 billion in extra revenue in fiscal 2001 had been spent in the state budget, instead of being returned to taxpayers.[32] Thus, TABOR’s spending cap probably reduced the largest state budget deficit of Colorado’s recession by 83 percent.

Colorado’s poor job growth since the recession has led some to argue that TABOR’s economic impact has been negative.[33] One figure from the U.S. Bureau of Labor Statistics suggests that Colorado has had virtually no job growth since fiscal 2001.

This measurement is not consistent with other figures put out by the Bureau of Labor Statistics and other independent economic sources. The bureau’s monthly national unemployment statistics indicate that Colorado has added more than 137,000 jobs since 2001. This is a job growth rate of nearly 6 percent, compared to a national growth rate of less than 4 percent.[34]

In April 2005, the Federal Deposit Insurance Corporation issued a state profile that found that Colorado had the 10th fastest annual state job growth in 2004, achieving a rate 31 percent above the national average. According to the Denver Business-Journal, an FDIC spokesman commented about the findings: "Colorado has had a remarkable turnaround. I don’t think anybody expected the type of rapid acceleration that the state has had."[35]

While it will be easier to tell by next year whether Colorado’s economic and job growth are indeed above the national average, it seems unlikely that the Bureau of Labor Statistics data suggesting no growth is correct.

Amendment 23 and Referendum C: The Education Spending Mandate and the TABOR "Time-Out"

Colorado’s fiscal 2002 budget was heavily affected by Amendment 23, a constitutional spending mandate for primary and secondary education that was approved by Colorado voters in November 2000. Amendment 23 requires that state spending on local public schools through 2010 increase annually by no less than one percentage point above the rate of inflation. After 2010, the amendment requires state spending on local public schools to meet or exceed the inflation rate.¶¶

As a 2003 Colorado House report on TABOR observed, Amendment 23 was passed during a widespread assumption in 2000 that Colorado’s budget surpluses would continue.[36] From 1998 to 2001, Colorado’s economic growth had resulted in state tax revenue that annually exceeded the TABOR limit by more than $500 million, requiring tax refunds of comparable size.[37]

The budget surpluses ended shortly after voters approved the spending mandate, however. Overall state spending had to be reduced to match the lower revenue, but the state budget for primary and secondary education, representing about 24 percent of total Colorado government spending, was constitutionally required to increase above the inflation rate.[38] By 2006, according to the Cato Institute, Amendment 23 mandated that public school spending be $818 million higher than it had been in 2001, even as state tax collections remained $226 million less than they were in fiscal 2001.[39]

Colorado lawmakers achieved the education spending increases by making cuts to other state programs. In 2005, advocates of these programs persuaded Colorado voters to ratify "Referendum C," a statewide ballot proposal that allows the state to keep all of the projected revenue surpluses through 2010.

The estimated cost to taxpayers of the forgone rebates during the next five years is more than $4.88 billion, a larger sum than the total TABOR rebates to date.[40] Absent the education spending mandates in Amendment 23, taxpayers would have been much less likely to incur these costs, since the higher spending would have required voters to approve new taxes.

|

¶¶ A similar education spending mandate is contained in Michigan’s current Proposal 5, which will appear on the November 2006 statewide ballot. The Michigan proposal mandates increases only at the inflation rate, but the proposal also mandates increases in state spending on higher education. The proposal includes several other spending mandates as well (see the Mackinac Center for Public Policy’s “An Analysis of Proposal 5: The ‘K-16’ Michigan Ballot Measure,” September 2006). |

TABOR’s Effect on Government Programs

Some critics of the SOS proposal have argued that TABOR harmed Colorado government programs for health care, roads and education, and that the SOS proposal would cause similar damage in Michigan.[41] One statistic cited is that in 1992 Colorado ranked 35th as a share of personal income for primary and secondary education spending, but fell to 49th by fiscal 2001. Similar figures exist for higher education.

Lower spending figures do not necessarily mean that the quality of services is lower, however. As of July 2005, more than 1 million people had moved to Colorado since enactment of TABOR. This immigration produced a total growth in state population of 29 percent, which is double the national average over those years and significantly higher than a comparable period prior to the passage of TABOR.[42] This influx of new residents to Colorado suggests the state was a relatively attractive location. It seems unlikely that Colorado became an attractive place to live while simultaneously developing a poor education, health and road system.

The United Health Foundation, while noting that the state has comparatively low spending on public health, nonetheless ranks Colorado as the 17th healthiest state in the nation for fiscal 2005 — 9.7 percent above the national average. This is not substantially changed from 1990, three years prior to the enactment of TABOR, when Coloradans ranked 14th healthiest.[43]

The education statistics cited above involve spending as a share of personal income, a measure that is somewhat distorted by Colorado’s rapid economic growth. In the 12 years following the implementation of TABOR in 1993, per-capita personal income in Colorado increased from 17th highest in the nation to eighth highest, growing from 3 percent above the U.S. average to 10 percent above the average. The fact that education spending fell as a percentage of this rapidly rising income means only that education spending did not rise as quickly, not that this spending did not rise at all.[44]

The latest data available for per-pupil education expenditures on primary and secondary education reveals that in 2003 Colorado was the 26th highest spending state, similar to the 22nd place ranking for per-pupil spending that Colorado achieved in 1992, before TABOR was enacted. In 2003, Colorado’s primary and secondary school students scored 15th highest in the nation on the National Assessment of Education Progress tests, an apparent improvement from 1992.[45]

As noted above under The State Budget: 1995-2007, The Budget Stabilization Fund, and Spending Limits and Taxpayer Rebates, the SOS proposal would have had a significant impact on state spending from fiscal 1995 to fiscal 2001, the years in which Michigan state revenues were growing rapidly in response to a strong state and national economy. If the SOS proposal had taken effect in fiscal 1995, the state budget would have been more than $2.2 billion smaller in fiscal 2001 than it actually was.[46] In addition, because the SOS proposal would have prevented the rapid rise in state spending from fiscal 1995 to fiscal 2001, state government would have spent approximately $9.6 billion less from fiscal 1995 through the recently enacted budget for fiscal 2007.[47] An estimated $8 billion of this $9.6 billion would have been returned to taxpayers as annual income tax refunds.[48]

These state spending reductions would have meant fewer state programs and activities, a result that some would argue is necessarily a net loss to the state. Nevertheless, it is not clear that all of the $9.6 billion in spending represented necessary state services. Total tax collection for 1999 and 2000 exceeded lawmakers’ projections, and for each year, new "supplemental" appropriations bills were written to spend the unexpected surplus taxes — more than $300 million for 1999, and nearly $400 million for 2000.

A number of new spending items were created during this period. For example, lawmakers in 2000 instituted a $2,500 college scholarship for high school students who score well on the state’s education assessment test. From fiscal 2000 to fiscal 2006, more than $800 million was spent on this new program.[49]

The necessity for some of the additional state spending during this period was called into question by many of the lawmakers themselves. The majority party in the state House of Representatives convened a task force in 2000 to examine potential cases of government waste in the 1999 budgets and issued a report that classified more than $131 million worth of spending for that year as "non-essential." Much of that $131 million involved spending enabled by the unexpected surge in tax revenues that year. A few months later, state lawmakers passed more supplemental spending for 2000.[50]

The monies spent on "non-essential" services were not available to taxpayers for their own savings and investment — uses that might have been more economically productive. The SOS proposal would have required that the state return almost $8 billion of the $9.6 billion tax revenue surplus from fiscal 1995 to fiscal 2007 to income taxpayers as annual refunds.[51] While the national recession that began during 2001 would have affected Michigan regardless of how much money state government was spending, there is historical economic evidence that lower taxes aid in the creation of economic activity and jobs,[52] a result that appears to occur at least in part because government spending, which is not subject to market discipline, can be less efficient.

Hence, under the SOS proposal, the Michigan economy might have exceeded its actual historical performance following the recession. The largest tax rebates under the proposal — estimated at more than $2 billion in fiscal 2001 and more than $1.5 billion in fiscal 2002 — would have occurred on the threshold of the national recession.[53]

Based on Colorado’s experience with TABOR and on the calculations in "The State Budget: 1995-2007" above, the SOS proposal might have created more stable state budgeting and a stronger economy. The proposal’s use of inflation and population to set a cap in state spending growth also had a certain plausibility. Government programs often face rising costs due to inflation and to the desire to provide government programs to an increasing population. Using the combined increase in inflation and population to limit spending growth would seem to allow spending to adjust to basic changes in the state’s circumstances without major, fundamental increases from current state spending as a percentage of Michigan’s economy.

Critics of the cap, however, have argued that government purchasing is disproportionately concentrated on items that increase in cost faster than the goods in the Consumer Price Index that determine the official inflation rate. The items most frequently cited as creating special demands on state government are education and health care. Critics have also argued that limiting spending increases by population growth is flawed because Michigan’s aging population will lead to a disproportionate number of persons needing state services, such as health care payments.[54]

The demand for some government programs, such as health care subsidies, may indeed increase with an aging population. It is not clear, however, that the demand for other programs would also rise at a similar rate. For instance, the demand for such programs as primary and secondary schools, higher education and corrections might rise more slowly or even decrease, given that the demand for these programs is often related to the presence of younger people. These three programs together constitute more than half of state spending from state resources.

Government is not alone in paying the rapidly rising cost of health care and medical services. Businesses and other taxpayers bear these costs as well. Additionally, consumers spend more than twice as much of their average budget on transportation costs as government does, and these costs have been exceeding the rate of inflation as fuel prices have soared.[55] Providing a cap on the growth of state spending would likely leave individuals with more resources to cope with such costs.

Public primary, secondary and higher education constitutes about 54 percent of state government spending from state resources, and costs in this area have increased more than twice the rate of inflation.[56] However, much of the rising cost of public education appears to be the result of its being a government enterprise.

The presence of a tax base means that government spending is often less responsive to market signals. For example, one source of rising public education costs in Michigan is the retirement plan for Michigan public school teachers. According to the Michigan Senate Fiscal Agency, the cost of this benefit now consumes a significant share of all new state spending on primary and secondary education.[57] The retirement plan pays benefits that the vast majority of Michigan’s private-sector employers do not offer.[58] In addition, many Michigan public school districts are reluctant to privatize their noninstructional services, despite evidence that privatization could lower costs without harming service quality.[59]

The objection to the SOS cap on grounds that education costs rise faster than the inflation rate seems unpersuasive. The fact that government spending on a government enterprise is rising quickly compared to private-sector spending could easily be a better argument in favor of the state spending cap than against it.

The SOS proposal’s prohibition on state-funded lawmaker pensions would have reduced state legislators’ overall compensation. It does not appear that this reduction would have put the pay of legislators in Michigan below that of legislators in other states.

Michigan is one of a dozen or so states with a full-time legislature.*** Michigan’s lawmakers presently receive more than $79,000 per year in base salary, and they are permitted an expense account for $12,000 more.††† They are the second-highest compensated state lawmakers in America.

Most states have a part-time legislature and pay lawmakers considerably less than Michigan does. About half of all states pay a base annual salary of less than $20,000. Texas, the second largest state for both geography and population, meets every other year for five months and pays lawmakers an annual salary of $7200. New Mexico lawmakers receive only expenses while in session, and New Hampshire lawmakers receive nothing more than a flat $200 fee for two years of service.[60]

|

*** An exact count of the number of full- and part-time legislatures depends on how these terms are defined. ††† Those who serve in leadership positions, such as the Speaker of the House and the Senate Majority Leader, may receive up to $27,000 in additional compensation. |

Prior to the SOS proposal’s dismissal from the November 2006 ballot, critics of the SOS proposal had suggested that the proposal’s language was unclear. The Michigan Chamber of Commerce asserted that the SOS proposal "is ambiguous, would introduce unfamiliar terms into the state constitution, and lacks clarity." The chamber concluded that the proposal "would result in years and years of costly litigation."[61] The Defend Michigan Coalition, a group formed to oppose the SOS proposal, has suggested that the SOS amendment would force every license or fee increase to go to a countywide vote.[62]

If the proposal did produce litigation, as seems likely, the result would be in keeping with most major constitutional reforms. The Headlee amendment produced substantial litigation involving disputes over definitions and language. As discussed earlier, the ultimate decision by the Michigan Supreme Court to define a "mandatory user fee" as a tax requiring voter approval was decided in 1998, 20 years after the amendment’s ratification. The "Durant" lawsuits over application of the Headlee amendment’s unfunded-mandate clause took roughly as long.

Indeed, for the first six years after passage of the Headlee amendment, Michigan government failed to make an official calculation of the Headlee revenue limit. This was remedied in 1986, after an estimate of the prior year accounts seemed to indicate that the revenue limit had been exceeded for the first time. While it was ultimately determined that the limit had not been exceeded, a formal system for calculating and reporting compliance with the limit was finally created by the Legislature only after this event.

The assertion that such items as dog licenses would have required a vote of the entire electorate seems less likely to have prompted serious dispute. For instance, the director of the Michigan Senate Fiscal Agency specifically singled out dog licenses as a user fee that would not require voter approval before the fee could be increased.[63]