The proposed "Stop Overspending" state constitutional amendment, which failed to gain ballot status in the November 2006 election, addressed four major areas:

capping the annual increase in state spending at the percentage sum of annual inflation growth and population growth;

depositing 50 percent of any surplus state revenues into the state budget stabilization fund, up to a total fund balance of 10 percent of total state spending from state resources, and allowing withdrawals only when annual state revenues were less than the state spending cap established in the first provision above;

preventing the sale of certain types of local bonds without voter approval; providing a definition distinguishing taxes from fees; requiring that special tax assessments be subject to voter approval; extending the statute of limitations for challenging potentially unconstitutional taxes; and preventing so-called "preapproval" of property tax rollback "overrides"; and

prohibiting state legislators from receiving state-funded pensions.

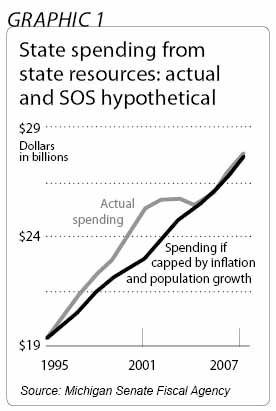

Total state spending from state resources (as opposed, for instance, to federal government resources) was about $19.3 billion in fiscal 1995 and more than $25.2 billion in fiscal 2001, a total growth of more than 30 percent.* During the same period, the sum of the inflation rate and the state’s population growth rate was less than 20 percent. If the SOS proposal had taken effect in fiscal 1995, the state budget would have been more than $2.2 billion smaller, or about 9 percent less, in fiscal 2001 than it actually was. In addition, because the SOS proposal would have precluded the rapid rise in state spending from fiscal 1995 to fiscal 2001, state government would have spent approximately $9.6 billion less from fiscal 1995 to fiscal 2007. The proposal would have required that an estimated $8 billion of this $9.6 billion be returned to taxpayers as annual income tax refunds.

Because the spending cap would have continued to rise, however, and because actual Michigan state spending declined after fiscal 2001, the spending cap and actual state spending in fiscal 2007 would have differed very little. If the SOS proposal had been in effect, fiscal 2007 state spending from state resources would have been just one-quarter of one-percent less than spending in fiscal 2007 is currently budgeted to be.

Michigan’s budget stabilization fund had a balance of almost $1.3 billion in fiscal 2000. It is effectively empty today. Under a hypothetical SOS proposal, the budget stabilization fund would have contained more than $2.2 billion by fiscal 2001 and almost $2.5 billion after a likely withdrawal from the fund in fiscal 2005. Under the SOS proposal, it appears that after 2001, state government would have had a larger budget stabilization fund and experienced diminished surpluses, rather than larger deficits.

|

* Sources for the findings cited in the executive summary are provided in endnotes to the main text of this Policy Brief. |

The Stop Overspending initiative has been compared to Colorado’s "Taxpayer’s Bill of Rights." TABOR, as the Colorado provision is commonly abbreviated, is a 1992 amendment to the Colorado Constitution that usually caps the annual percentage growth of Colorado’s state spending and revenue at the sum of the percentage rates of inflation and population growth.

TABOR and the SOS proposal are similar in two ways: Both use the inflation-and-population standard to regulate the growth of state spending, and both contain some local taxpayer provisions like those mentioned above. TABOR and SOS are also dissimilar in several ways: TABOR is more strict in restraining state spending, since TABOR includes more state revenues, such as tuition paid to state colleges, towards the spending cap; TABOR does not permit a budget stabilization fund comparable to what would have existed under the SOS proposal; TABOR does not require withdrawals from the budget stabilization fund when state revenue is less than the spending limit; and TABOR "ratchets down" Colorado’s annual spending limit to the actual spending level for any year when state revenue lags, while the SOS proposal would simply have kept the current (higher) spending limit in place.

The implementation of TABOR coincided with strong economic growth for Colorado. Even after a pronounced recession beginning in 2001, Colorado’s job growth from 1993 to 2006 was nearly 38 percent, or almost 690,000 new jobs, according to data from the U.S. Bureau of Labor Statistics. This increase substantially eclipsed the 20 percent national job growth for the same period. In contrast, in the 10-year period prior to TABOR’s enactment, the nation added 18 percent to its jobs base, and Colorado added a more average 19.1 percent.

The Washington, D.C.-based Tax Foundation has observed that by preventing Colorado state government from increasing state spending rapidly prior to 2001, TABOR appears to have mitigated the budgetary challenges that could have appeared after 2001. In 2002, when Colorado’s total state revenues declined by more than $1 billion, the state budget faced a deficit of about $196 million — considerably less than the $1.1 billion deficit the state might have faced absent TABOR’s spending limitations.

U.S. Census Bureau data show that from 1993 to 2005, Colorado’s population increased 29 percent, a rate more than twice the national average. The Washington, D.C.-based Heritage Foundation also found that measures of per-capita personal income growth and per-capita gross state product show Colorado lagging the national average in the decade prior to TABOR and then significantly outperforming the average in the decade afterward.

By some measures, Colorado state government spending on such programs as health care and education is below the national average. The United Health Foundation nonetheless ranks Colorado as the 17th healthiest state in the nation for 2005 — 9.7 percent above the national average. In 2003, Colorado’s primary and secondary school students scored 15th highest in the nation on the National Assessment of Educational Progress, a ranking mostly unchanged from 1992, prior to the implementation of TABOR.

Michigan state government would have spent an estimated $9.6 billion less from fiscal 1995 to fiscal 2007 if the SOS proposal had been in effect. These state spending reductions would have meant fewer state programs and activities, but there is also economic evidence that lower taxes aid in the creation of economic activity and jobs.

The necessity for some of the $9.6 billion in spending was called into question by many of the lawmakers themselves. The majority party in the state House of Representatives convened a task force in 2000 to examine potential cases of government waste in the 1999 budgets and issued a report that classified more than $131 million worth of spending for that year as "non-essential."

Some have argued that the SOS spending cap would be ill-suited to state government, since government purchasing is disproportionately concentrated on such items as health care and education, which increase faster than the official inflation rate. This argument should be balanced against two additional observations: Individual and business taxpayers must bear such costs as rising health care as well, and much of the rising cost of a government good like public education appears to be the result of its being a government enterprise. The fact that government spending on a government enterprise is rising quickly compared to private-sector spending could easily be an argument in favor of the state spending cap, rather than against it.

It does not appear that the SOS provision to end publicly funded pension plans for state legislators would have put the pay of legislators in Michigan below that of legislators in other states. Michigan is one of a dozen or so states with a full-time legislature (an exact count depends on how "full-time" is defined). Michigan lawmakers are the second-highest compensated state lawmakers in America. They presently receive more than $79,000 per year in base salary, and they are permitted an expense account for $12,000 more. About half of all states pay a base annual salary of less than $20,000.