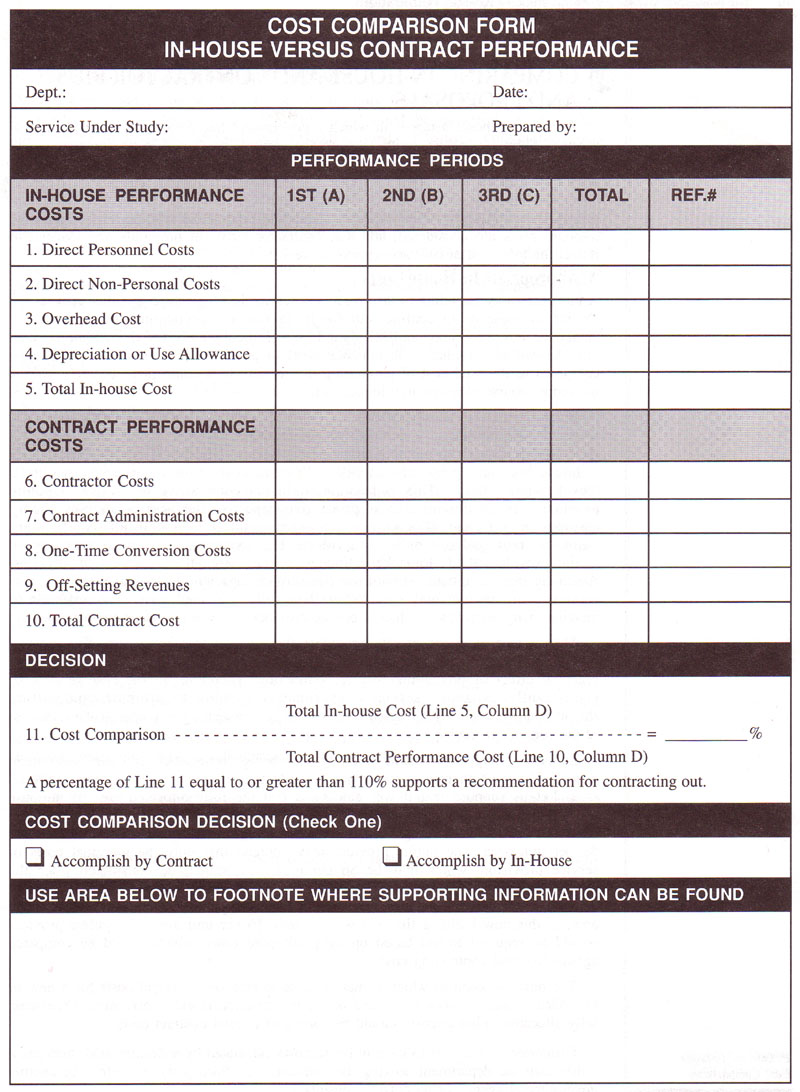

A number of state and local governments have developed cost comparison formats to assist officials in presenting a summary of cost comparison data between in-house and contract service delivery. The City of Cincinnati, Ohio has developed one of the more comprehensive formats.[31] A modified version of the City of Cincinnati's cost comparison format appears on the following page.

While the cost-comparison format is basically self explanatory, three aspects do warrant special mention: 1) avoidable costs; 2) performance periods; and 3) the cost-comparison ratio.

A. Avoidable Costs

Only avoidable costs are entered in the various categories under in-house service delivery costs. The cost-comparison format assumes that the fully allocated costs of in-house service delivery have already been determined.

B. Performance Periods

The format provides space to include cost-comparison data for up to three performance periods. A performance period is one fiscal year, or a portion thereof if a target service is being considered for contracting out in the middle of a fiscal year. Several reasons exist for carrying out the cost comparison over multiple performance periods. For example, the total cost savings associated with contracting out may not be realized in the initial performance period due to such factors as large contractor start-up costs for facilities or equipment and/or significant government one-time conversion costs. In both instances, these costs should be amortized over multiple performance periods. Another reason is that short-ten-n cost comparisons (i.e., one performance period) may fail to account for possible relevant future changes in the costs of labor, materials, transportation, etc.[32]

C. The Cost-Comparison Ratio

The cost-comparison ratio (see line 11 of the cost-comparison format) is the

ratio between the total cost of in-house service delivery and the total cost of contract service delivery. The purpose of the cost-comparison ratio is to establish a cost-savings threshold that justifies a decision to change the mode of service delivery. While theoretically justifiable on the basis of any cost savings, many government agencies have adopted the policy that the cost savings should be sufficient to warrant the organizational upheaval associated with the changeover. The federal government, the state of Texas, and the City of Cincinnati, Ohio have all established a threshold level of 10 percent when considering a change from in-house to contract service delivery.[33]