Objective Questions

The objective of this analysis is to answer three questions:

The Variation of SBT

Burdens Across Industries

Is there a substantial and

consistent difference in the relative SBT burdens of various industries, across

different time periods and economic situations?

The Taxation of the

Financial Industry

In particular, how does the

Financial Industry compare with other Michigan industries in their SBT burden?

The SBT and Business

Expansion

What peculiar facets of the

SBT discourage or encourage business expansion in Michigan, and what does this

suggest for retaining, modifying, or replacing the VAT concept for Michigan

business taxation?

Findings

The analysis produced the following findings:

The Single Business Tax

Comprehensiveness of the Single Business Tax System

The use of a single, comprehensiveness tax system has built-in advantages in the equality of treatment among industries. Multiple tax systems must overcome the built-in disadvantages of complexity and redundancy. The legislature's purpose in creating the Single Business Tax included greater equality of treatment. The recreation of multiple tax systems would work against this purpose.Cyclicality of a VAT

The VAT-type SBT limits the cyclicality of revenue to the State government, but increases the cyclical pressures on taxpaying businesses. The benefits of better cyclical stability of tax revenue under a VAT must be discounted by the cost of increased cyclical instability for the taxpaying businesses and individuals.The SBT and Capital Expenditures

Because the depreciation deductions allowed in most profits tax systems understate the true cost of capital expenditures, consumption-type VAT's like the SBT are more favorable to capital expenditures than profits taxes. Because many of Michigan's major industries are capital-intensive, this more-neutral treatment of investment is a major advantage of the SBT over the profits tax systems in other states. The full expensing of capital investments under the SBT encourages businesses to invest in Michigan.

The 1985 Treasury Report

The government study of record on the SBT was authored by the Michigan Department of Treasury in 1985. The quantitative analysis in this study relies on the data gathered for the Treasury study, and critically reviews its methodology. The findings below summarize the limitations of the Treasury data, and the biased results introduced by the Treasury methodology.

1985 Treasury Report Data Limitations: Unusual Sample Year

The sample period of the Treasury study was a time of extreme economic contraction, which affected some Michigan industries more than others.Insufficient Sample Period

The sample period of the Treasury study was very short, and does not indicate the behavior of various industries over the entire economic cycle.Old Data

The number and importance of economic changes occurring in the over-five-year time lapse between the sample period and the current date limit the predictive power of the data.Aggregation

The groupings of industries into standard categories can hide differences between the industries. In the Financial Industry category, banks, insurance companies, and real estate companies are grouped together, even though substantial differences exist among the three in business operation. Conclusions about a group cannot be generalized to all its components without further analysis of disaggregated data.Biased Results from the Use of an Incorrect Tax Base

The 1985 Treasury Report relied on an incorrect measure of the tax base, which ignored capital expenditures. Thus, their analysis systematically biased downward their calculated SBT burdens. The actual tax burdens of Michigan industries were higher than those stated in the Treasury study, particularly for those industries making large capital expenditures in the sample period.

Analysis of Single Business Tax Burdens on Michigan Industries

Using the proper methodology, which took into account capital expenditures in selecting a tax base, this analysis produced the following findings about the SBT burdens on Michigan industries.

Relative Tax Burdens

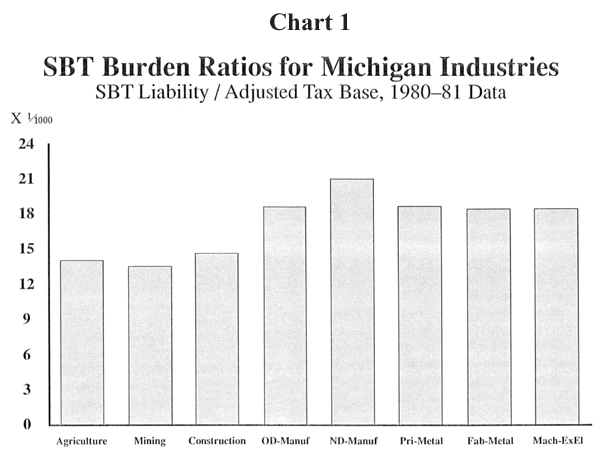

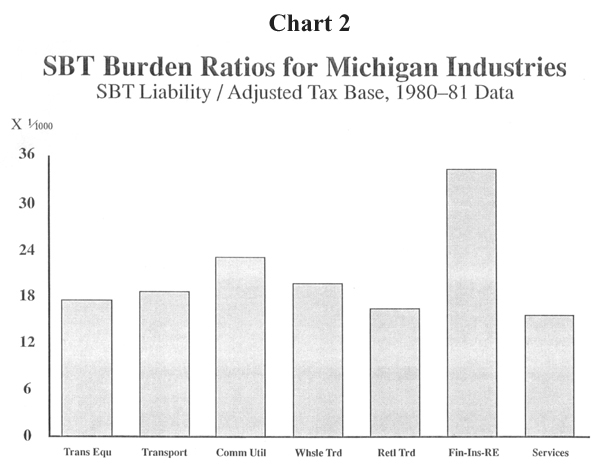

The SBT burden as a percentage of the Adjusted Tax Base varied considerably across industries during the sample period, ranging from 1.4% for Agriculture to 3.35% for Finance, Real Estate, and Insurance. The average tax burden ratio for all firms was 1.8%.Comparison with Treasury Results

The tax burden ratios are higher and more varied than those reported in the Treasury study. To conclusively determine relative tax burdens, data from one complete economic cycle must be analyzed, using the proper methodology.The SBT Burden Compared with Profits

The aggregate SBT liability of Michigan firms represented over 20% of their pretax profits in the sample period. The SBT clearly intensifies the cyclical pressures faced by Michigan businesses; this ratio probably drops sharply in good economic years.Business and Personal Tax Burdens in Michigan

Both business and personal tax burdens in Michigan are significantly higher than the national average. US Census Bureau data show that Michigan's 1984-85 Corporate Taxation burden was the second highest in the nation, double the national average. Because both theory and experience show that high tax burdens discourage economic growth, the Legislature should lower the overall tax burdens in the State.The "Fairness" of SBT Burdens on Michigan Industries

For a tax system to be equitable and efficient, it must levy a similar proportionate burden for firms of different size and in different industries over the entire economic cycle. During the sample period, the tax burden ratios varied significantly, indicating that there may be a bias against some industries in the SBT caused by unequal use of special credits and deductions.The Tax Burden of the Financial Industry

During the sample period, the tax burden of the Financial industry was the highest of all industries. While data from a complete cycle are needed to conclusively establish relative burdens, there is no basis to conclude that the Financial industry escapes its share of the SBT burden.

{kind=link}

{kind=link}