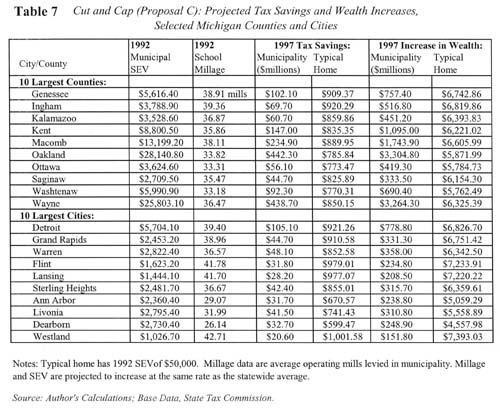

Table Seven contains projections of tax savings and wealth increases for property owners in the ten largest Michigan cities and counties. These projections are based on 1992 average school operating millage rates and SEV for each municipality, using the same methodology as the statewide model outlined in Appendices II and IV. SEV and millage rates are assumed to grow in each municipality at the same rate as statewide, both under current law and Cut and Cap.

In Michigan cities, the owner of a typical home assessed at $50,000 in 1992 could expect to receive a 1997 tax cut of $921 in Detroit, $911 in Grand Rapids, and $671 in Ann Arbor. In Michigan counties, the owner of a typical home assessed at $50,000 could expect to receive a 1997 tax cut of $850 in Wayne, $786 in Oakland, $890 in Macomb, and $835 in Kent.

These tax cuts would increase the 1997 property values, and hence the homeowners' equity, in a typical home by amounts ranging from $5,059 in Ann Arbor to $6,820 in Ingham County. Such increases in wealth could be converted into spendable dollars by selling the property, leasing it, or obtaining a home equity loan.

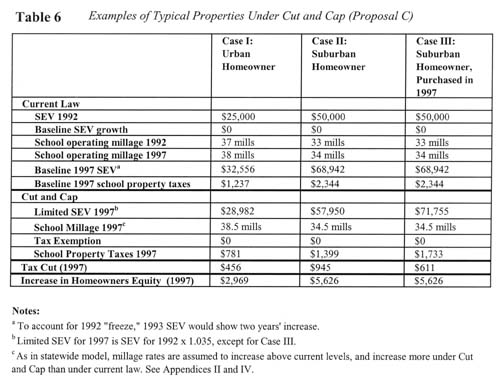

The typical home in each municipality is defined as one having a 1992 SEV of $50,000, meaning that its approximate current market value would be $100,000, This is done for ease of comparison, and does not reflect an average home value for each municipality. To adjust the projections for properties of greater or lesser value, simply increase or decrease the amounts by the same percentage as the property differs in market value from $100,000. For example, a home with a current market value of $120,000 would be expected to receive a tax cut and an increase in value 20% higher than the typical home for each municipality.

The SEV of the typical home is assumed to increase at the same rate as statewide SEV, reflecting a mix of newly-sold and unsold parcels, as well as new construction. This is different from the three examples shown in Table Six. These have no new construction, and either remain owned by the same person, or (Case III) are purchased and reassessed in 1997. Actual increases in market value could vary considerably among municipalities across the state.

Effects on Schools and Local Governments

Cut and Cap would reimburse school districts for the exempted property tax. The proposal properly limits the reimbursement to the millage rate approved by the voters in 1991, so there is no incentive to raise millage rates further.[29] However, this does create a disincentive to lowering millage rates below 1992 levels. The revenue analysis assumes increases in school operating millage rates under current law, and larger increases under Cut and Cap, and limits the reimbursement from the state to that calculated with the 1991 millage rate.

Under Cut and Cap, revenue to local units of government from property taxes and state reimbursement to local schools is projected to increase at annual rates increasing from 6.6% in 1993 to 6.9% in 1997. Local government revenue increases from $9.0 billion in 1992 property tax revenue alone to $12.6 billion in combined property tax and reimbursement revenue in 1997.

This strong revenue growth occurs even with the assessment growth cap and limits on the reimbursable millage rate. A number of factors contribute to this:

Even with the assessment growth cap, SEV is projected to grow from $154 billion in 1992 to $207 billion in 1997, a 34% increase over five years.

The "cap" would reduce the number and amount of Headlee rollbacks, thus allowing higher millage rates. The actual reduction in revenue due to the assessment cap is not the growth rate of property less 3%, but a much smaller rate.

Tax capitalization would generate a large increase in the actual value of property, which will gradually work its way into SEV as property is sold. This expands the tax base on which millage is levied.

Citizens would still have the ability to vote higher millage, within constitutional limits.

Furthermore, local governments would benefit from the tremendous economic stimulus of the tax cut. Thus, the overall effect of Cut and Cap on local governments, at least over the long term, would be similar to that on the overall economy of the state.

Effects on Local Governments: Local Share of State Revenue under the "Headlee" Amendment

Under Article IX Section 30 of the Michigan Constitution, added by the "Headlee" amendment, the state is required to allocate a minimum share of its spending to local units of government, taken as a group. The state, through a complicated scheme, violated this provision of the Constitution in the 1980's, and Oakland County sought relief from the court. After losing in the Circuit and Appeals courts, and facing an adverse Supreme Court ruling, the state settled in June 1991.[30] The settlement forces the state to begin allocating over $400 million in state spending to local units of government beginning in Fiscal Year 1993. This requirement will be difficult to meet without constant policing of state spending.

The state's reimbursement payments to local schools under Cut and Cap would count towards its obligations to local governments under section 30 of the Headlee amendment. Should Cut and Cap pass, and the state not enter into any new prohibited maneuvers, the required reimbursements should move it into easy compliance with the Section 30 requirement. This does create the risk that the state would reduce its support of other local government services. However, Article IX section 29 of the Michigan Constitution, also added by the Headlee amendment, requires the state to fully fund any individual activity or service provided by local governments that is mandated by the state.[31] This will limit, though not eliminate, the risk of state reductions in local government support.[32]