The overall property tax burden would change only slightly under HJR H. It is likely that property taxes would be slightly higher under HJR H in 1993, and could be slightly higher or lower after that.

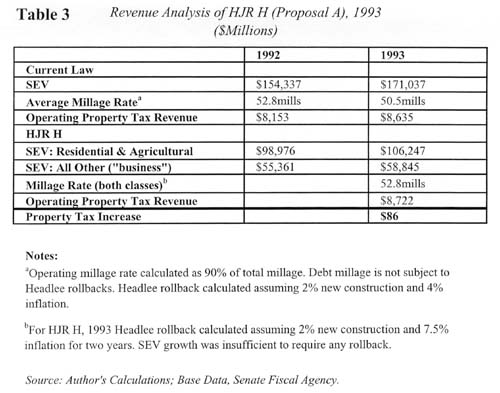

Table Three outlines projected property taxes under current law and HJR H in 1993. Under current law, the Headlee amendment would roll back the average millage rate by a significant amount in 1993. HJR H, on the other hand, would not require a reduction in average millage rate, as its special 1993 provision allows assessment increases to raise property tax revenue by the equivalent of two years' inflation, before triggering a Headlee rollback.[21] Even with a slightly lower SEV due to the assessment growth cap on "homesteads," this would result in property taxes being about 1% higher under HJR H than under current law.

In subsequent years, the assessment growth cap might cause property tax burdens to decline to slightly below current law. However, the creation of split millage rates, and the possibility of direct tax increases on only one class of property, might result in overall tax burdens higher under HJR H than under current law. With the considerable uncertainty as to how HJR H would actually be implemented, one cannot predict with much confidence the relative tax burdens more than a year or two out.

Why No Tax Savings?

The lack of any tax savings under HJR H, and the likelihood that taxes would actually increase slightly compared with current law, are mostly explained by the following three factors:

HJR H does not promise any direct reduction in millage rates or the assessment ratio.

Whatever relief results would frequently come to one class of property owners at the expense of another. Since the Headlee rollbacks would occur by class, rather than as a whole, a larger rollback in one class simply means a smaller rollback in another. Similarly, the assessment growth cap on homesteads means a smaller Headlee rollback for other residential & agricultural property.

In 1993 HJR H would allow tax revenue to increase by a rate of two years' inflation, setting a higher base to begin with.

Comparison With Other Revenue Analyses

This study directly calculated Headlee rollback factors to determine millage rates under both current law and HJR H. The reduction in millage rates under current law, compared with no reduction under HJR H, resulted in slightly higher 1993 property taxes under HJR H.

By comparison, Senate Fiscal Agency revenue analysis of HJR H assumed a slight increase in overall millage rates under HJR H, and somewhat lower millage rates under current law. They project a very slight decline in property tax burden in the first few years, growing to about 2% by 1997. Business taxes were projected to increase slightly, with residential tax burdens declining slightly.[22]