Results from the model include:

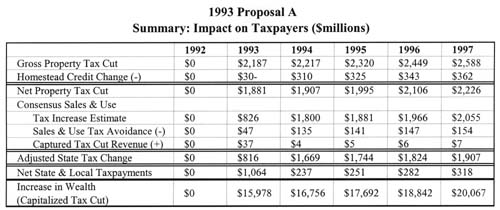

School millage rates are cut from a statewide average of 34.6 in 1992 to 22 mills in 1993, generating a gross tax cut of $2.2 billion in the current year. After adjusting for reduced "homestead" income tax credits, the net property tax cut in 1993 is almost $1.9 billion, which grows to over $2.2 billion by 1996.

The value of property under "A" grows from $308 billion in 1992 to $408 billion in 1996, partially due to "tax capitalization" of roughly $16 billion in 1993, growing to almost $19 billion in 1996.

Because of the assessment-growth cap. the State Equalized Value (SEV) grows more slowly, from $154 billion in 1992 to $200 billion in 1996. The combined effect of higher property values, and capped assessment increases, is annual tax savings of over $500 million from 1993 through 1996. Interestingly, the assessment cap does not stop the growth of SEV, which continues to grow only slightly slower than under current law for two reasons: First, as parcels are resold, their re-assessed values are significantly higher. Second, new construction of roughly 2% per year comes directly into SEV.

Sales and Use and other state tax revenue increases by over $800 million in 1993 and almost $1.7 billion in 1994. This includes two adjustments from the consensus estimate by state government agencies of the sales and use tax revenue increase under "A," which basically assumes that a 50% rate increase results in a 50% revenue increase. First, it adds the tax revenue gained from the additional disposable income from the net tax cut. Second, it accounts for consumers' avoidance of the 50% higher sales tax rate. Using conservative estimates of tax avoidance behavior, the model predicts that a 50% increase in the sales and use tax rates would result in a 5% drop in taxed transactions. This tax avoidance results in about $135 million less sales and use tax revenue in 1994 than the consensus estimate.

The net state-and-local impact on Michigan taxpayers would be a sharp $1.1 billion tax cut in 1993, and a smaller tax cut of $237 million in 1994, growing to $282 by 1996.

Table Two presents the summary results of the model.