As noted above, governments enact RES policies to prop up the price of renewable electricity generation. They begin with disadvantages: renewables are less efficient and therefore more costly than conventional sources of generation. Thus they are demanded and valued less in the open marketplace. RES policies force utilities to buy electricity from renewable sources. These policies guarantee a market for the renewable sources. These higher costs are passed to electricity consumers, including residential, commercial and industrial customers.

The U.S. Department of Energy’s Energy Information Administration estimates the “levelized energy cost” — or financial breakeven cost per MWh — to produce new electricity in its Annual Energy Outlook.[24] The EIA provides LEC estimates for conventional and renewable electricity technologies — coal, nuclear, geothermal, landfill gas, solar photovoltaic, wind and biomass — assuming the new sources enter service in 2016. The EIA also provides LEC estimates for conventional coal, combined cycle gas, advanced nuclear and onshore wind only, assuming the sources enter service in 2020 and 2035.[*]

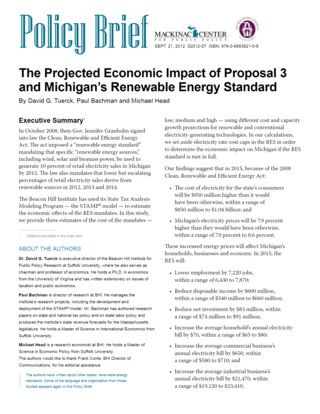

While the EIA does not provide LEC for hydroelectric, solar photovoltaic and biomass for 2020 and 2035, it does project overnight capital costs for 2015, 2025 and 2035. We can estimate the LEC for these technologies and years using the percent change in capital costs to inflate the 2016 LECs. In its Annual Energy Outlook, the EIA incorporates many assumptions about the future price of capital, materials, fossil fuels, maintenance and capacity factor into their forecast. Graphic 4 shows LEC projections for seven different energy sources. Four of these — coal, gas, nuclear and wind — are EIA projections; these LECs are expected to decrease from 2016 to 2035, with the exception of the LEC for gas. The fall in capital costs for coal, nuclear and wind drives the drop in total system LEC over the period.

The LECs for solar, biomass and hydroelectric power were estimated using the EIA change in overnight capital costs. These projections produce LEC reductions for solar biomass similar to wind’s from 2016 to 2035. The biomass LEC drops by 38.7 percent and solar by 53.5 percent over the period. These compare to much more modest cost reductions of 5.2 percent for coal, an increase of 14.2 percent for gas, and a drop of 22.1 percent for nuclear over the same period. EIA does provide overnight capital costs for renewable technologies under a “high cost” scenario. However, for each renewable technology the EIA “high cost” scenario projects capital costs to drop between 2015 and 2035.

Graphic 4: U.S. Energy Information Administration Estimates of Levelized Cost of Electricity from Conventional and Renewable Sources

Source: “Levelized Cost of New Generation Resources in the Annual Energy Outlook 2011,” (U.S. Energy Information Administration, 2011), http://goo.gl/DG6Qk (accessed June 13, 2012); “Figure 81. Levelized electricity costs for new power plants, 2020 and 2035 (2009 cents per kilowatthour),” (U.S. Energy Information Administration, 2011), http://www.eia.gov/ forecasts/archive/aeo11/excel/fig81.data.xls (accessed Sept. 18, 2012).

* Authors’ projections based on linear changes in EIA estimates for overnight capital costs during these time periods. For overnight capital costs, see “Assumptions to the Annual Energy Outlook 2011,” (U.S. Energy Information Administration, 2011), 168, http://goo.gl/irI69 (accessed Sept. 18, 2012).

Graphic 4 also displays capacity factors for each technology. The capacity factor measures the ratio of electrical energy produced by a generating unit over a period of time to the electrical energy that could have been produced at 100 percent operation during the same period. In this case, the capacity factor measures the potential productivity of the generating technology. Solar, wind and hydroelectric have the lowest capacity factors due to the intermittent nature of their power sources. EIA projects a 34.4 percent capacity factor for onshore wind power, which, as we will see below, appears to be at the high end of any range of estimates.

Estimating a capacity factor for wind power is particularly challenging. Wind is not only intermittent but its variation is unpredictable, making it impossible to dispatch to the grid with any certainty. This unique aspect of wind power argues for a capacity factor rating of close to zero. Nevertheless, wind capacity factors have been estimated to be between 20 percent and 40 percent.[25] The other variables that affect the capacity factor of wind are the quality and consistency of the wind, and the size and technology of the wind turbines deployed. As the U.S. and other countries add more wind power over time, presumably the wind turbine technology will improve, but the new locations for power plants will likely have less productive wind resources.

The EIA estimates of LEC and capacity factors paint a particularly rosy view of the future cost of renewable electricity generation, particularly wind. Other forecasters and the experience of current renewable energy projects portray a less sanguine outlook.

Today, wind and biomass are the largest renewable power sources and are the most likely to satisfy future RES mandates. The most prominent issues that will affect the future availability and cost of renewable electricity resources are diminishing marginal returns and competition for scarce resources. These issues will affect wind and biomass in different ways as state RES mandates ratchet up over the next decade.

Both wind and biomass resources face land-use issues. Conventional energy plants can be built within a space of several acres, but a wind power plant with the same nameplate capacity (not actual capacity) would require many square miles of land. According to one study, wind power would require 7,579 miles of mountain ridgeline to satisfy current state RES mandates and a 20 percent federal mandate by 2025.[26] Mountain ridgelines produce the most promising locations for electric wind production in the eastern and far western United States.

After taking into account capacity factors, a wind power plant would need a land mass of 20 by 25 kilometers to produce the same energy as a nuclear power plant that can be situated on 500 meters square (one-quarter square kilometer).[27]

The need for large areas of land to site wind power plants will require the purchase of vast areas of land by private wind developers, and/or allowing wind production on public lands. In either case land acquisition/rent or public permitting processes will likely increase costs as wind power plants are built. Offshore wind is vastly more expensive than onshore wind power and suffers from the same type of permitting process faced by onshore wind power plants, as seen in the 10-year permitting process for the planned Cape Wind project off the coast of Massachusetts.

The swift expansion of wind power will also suffer from diminishing marginal returns as new wind capacity will be located in areas with lower and less consistent wind speeds. As a result, fewer megawatt-hours of power will be produced from newly built wind projects. Moreover the new wind capacity will be developed in increasingly remote areas that will require larger investments in transmission and distribution, which will drive costs even higher.

The EIA estimates of the average capacity factor used for onshore wind power plants, at 34.4 percent, appears to be at the higher end of the estimates for current wind projects. This figure is inconsistent with estimates from other studies.[28] According to the EIA’s own reporting from 137 current wind power plants in 2003, the average capacity factor was 26.9 percent.[29] In addition, a recent analysis of wind capacity factors around the world finds an actual average capacity factor of 21 percent.[30] Moreover, other estimates find capacity factors in the mid-teens and as low as 13 percent.[31]

Biomass is a more promising renewable power source. Biomass combines low incremental costs relative to other renewable technologies and reliability. Biomass is not intermittent and therefore it is distributable with a capacity factor that is competitive with conventional energy sources. Moreover, biomass plants can be located close to urban areas with high electricity demand. But biomass electricity suffers from land use issues even more so than wind.

The expansion of biomass power plants will require huge additional sources of fuel. Wood and wood waste comprise the largest source of biomass energy today. According to the National Renewable Energy Laboratory, other sources of biomass “include food crops, grassy and woody plants, residues from agriculture or forestry, oil-rich algae, and the organic component of municipal and industrial wastes.”[32] Biomass power plants will compete directly with other sectors (construction, paper, furniture) of the economy for wood, food products and arable land.

One study estimates that 66 million acres of land would be required to provide enough fuel to satisfy the current state RES mandates and a 20 percent federal RES in 2025.[33] When the clearing of new farm and forestlands are figured into the GHG production of biomass, it is likely that biomass increases GHG emissions.

The competition for farm and forestry resources would not only cause biomass fuel prices to skyrocket, but also cause the prices of domestically produced food, lumber, furniture and other products to rise. The recent experience of ethanol and its role in surging corn prices can be causally linked to the recent food riots in Mexico,[34] and also to the struggle facing international aid organizations that address hunger in places such as the Darfur region of Sudan.[35] These two examples serve as reminders of the unintended consequences of government mandates for biofuels. The lesson is clear: Biofuels compete with food production and other basic products, and distort the market.

[*] “Figure 81. Levelized electricity costs for new power plants, 2020 and 2035 (2009 cents per kilowatthour),” (U.S. Energy Information Administration, 2011), http://www.eia.gov/forecasts/archive/aeo11/ excel/fig81.data.xls (accessed Sept. 18, 2012). While not specified in the source document, the levelized cost estimates for coal, nuclear and wind are for conventional coal, advanced nuclear and onshore wind, respectively.