The average cost of treating an auto accident injury in Michigan tripled over the last decade and is now more than five times the cost in the next most-expensive state. Despite this, insurance companies have, on average, lost money selling auto insurance over the same period. Those are two of the findings from a recent deep dive conducted by Crain’s Detroit Business and Bridge Magazine.

Crain’s and Bridge recently teamed up to do some fantastic research on the hottest topic in Lansing: auto insurance reform. The results strongly support the case for changing the way auto insurance works in this state.

The most obvious and immediate take-away from looking at the data is that there is a very real problem with Michigan’s auto insurance laws. And, if the status quo remains, things are likely to get worse.

For example, according to Crain’s and Bridge’s analysis of data from the National Association of Insurance Commissioners, the average cost for treating automobile injuries in Michigan tripled from 2000 to 2013, growing 90 percent faster than total health care inflation. And this was during a period when the number of motorists injured in accidents actually decreased. The average cost to treat an injury from an auto accident in Michigan is now north of $75,000, more than five times the next highest state, New Jersey.

This is not hyperbole: Medical costs for treatment from car accident injuries are out of control. The primary reasons for this are that medical providers can essentially charge whatever price they think they can get away with and there’s no limit to the amount of benefits an individual can receive. Plus, a 2010 Michigan Supreme Court ruling made it easier for people injured in accidents to sue and win even more benefits.

This is why the cost controls proposed in House Bill 5013, sponsored by Rep. Lana Theis, R-Brighton, are necessary. Since the state requires all drivers to purchase expensive personal injury protection, it should impose a fee schedule on what medical providers can charge insurers for services and procedures. Similar types of fee schedules are used for Michigan’s workers’ compensation program and government-run insurance programs, such as Medicaid and Medicare. The bill would also allow drivers to choose a policy that limits their total benefits, resulting in a reduced-priced premium.

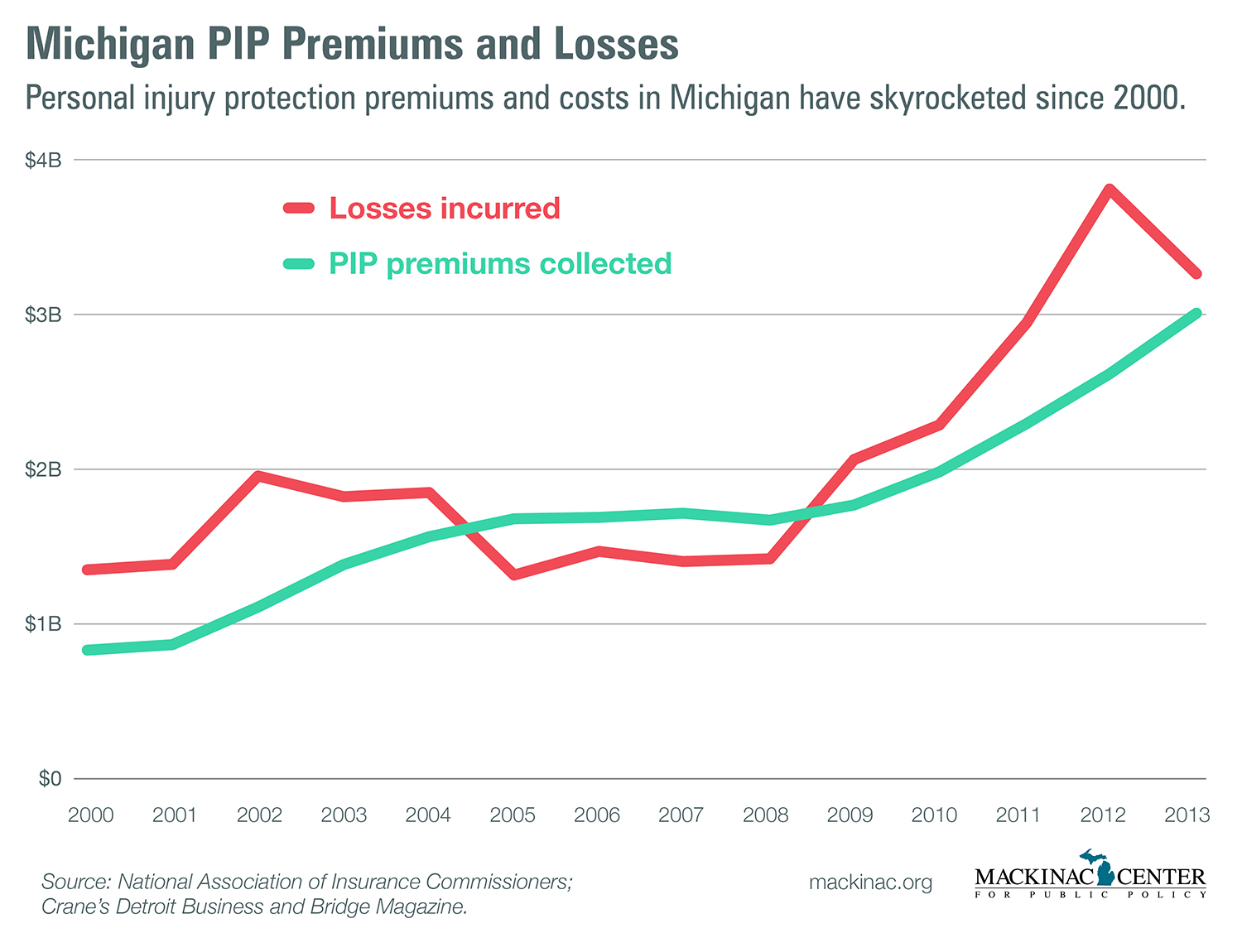

Opponents to this type of reform often claim that efforts to change the system are simply attempts to further enrich profitable and powerful insurance companies. The Crain’s and Bridge research shows, however, that insurance companies in Michigan are not raking in the dough. In fact, they’ve paid out more in medical benefits, or to use the industry term, “losses,” than they’ve received in revenue through premiums paid by Michigan drivers. This has been the case for the past several years now. Not surprisingly, then, from 2005 to 2014, the average profits for companies selling auto insurance were -2.9 percent, according to Crain’s and Bridge.

Even though the record shows that Michigan drivers aren’t lavishing large profits on insurers, their premiums have consistently ranked at or near the top in the nation. The new data obtained by Crain’s and Bridge provides even more detail on how Michigan compares to states that use similar no-fault insurance systems.

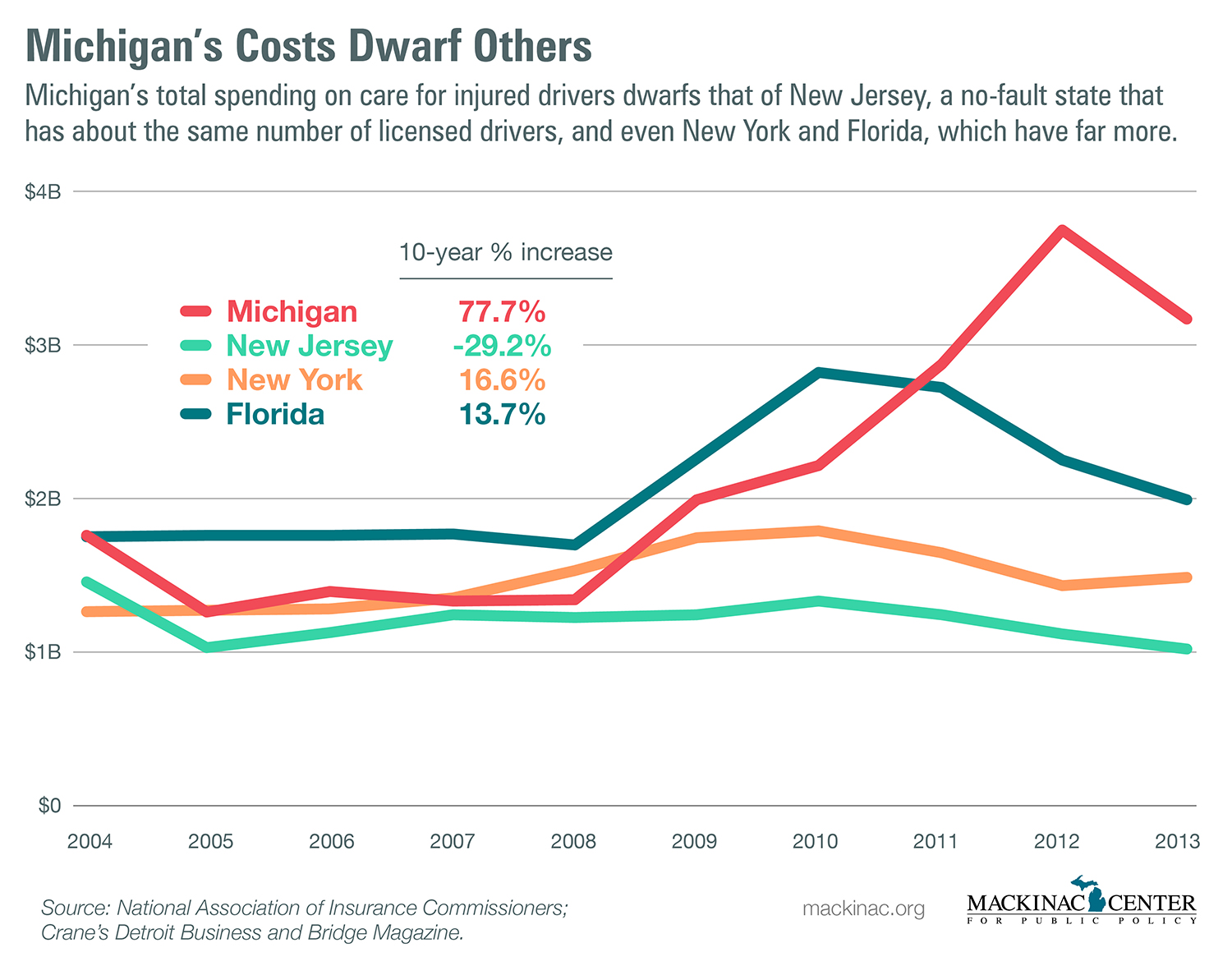

From 2004 to 2013, total spending on medical care for people injured in auto accidents in Michigan increased by 78 percent. In New Jersey, however, spending fell by 29 percent, even though the Garden State has close to the same number of drivers as Michigan. Total spending on medical care caused by auto accidents increased by 17 percent in New York and 14 percent in Florida. Those increases are significantly less than what Michigan has seen, despite the fact that these states have one-and-a-half to two times as many drivers as Michigan.

Regulating insurance markets is a complicated business, but the latest data unearthed by Crain’s and Bridge Magazine supports a simple conclusion: Michigan’s auto insurance laws are failing and need to be substantially reformed.

To learn more about this issue, visit https://www.mackinac.org/insurance.

Get insightful commentary and the most reliable research on Michigan issues sent straight to your inbox.

The Mackinac Center for Public Policy is a nonprofit research and educational institute that advances the principles of free markets and limited government. Through our research and education programs, we challenge government overreach and advocate for a free-market approach to public policy that frees people to realize their potential and dreams.

Please consider contributing to our work to advance a freer and more prosperous state.