Uniformity Clause Exception

HJR H would create an exception to one of the most important and enduring principles in property taxation: uniformity. This exception will allow different taxation rates to emerge, for two reasons:

Limitation on annual

assessment increases on homestead property.

Since the assessed

valuation of "homestead" parcels could not increase more than the rate of

inflation or 5%, whichever is less, the SEV of many of these parcels would lag

behind 50% of the market value, until they are sold.

The unusual nature of HJR H

stems from its combination of an assessment growth cap on some parcels with a

split "Headlee" millage rollback. The pros and cons of an assessment growth cap

alone are discussed in the section on Cut and Cap, page 19.

Split "Headlee"

rollback calculations

Under the "Headlee"

amendment, if the assessed value of one class of property grows at the rate of

inflation, and that of another grows faster, the millage rate on the latter

class alone will be rolled back. This will create two millage rates for each

current millage authorization.

Since "homestead"

assessment growth is capped, the class including homesteads will often show a

slower rate of growth in value. This will result in fewer and smaller rollbacks

for residential and agricultural property.

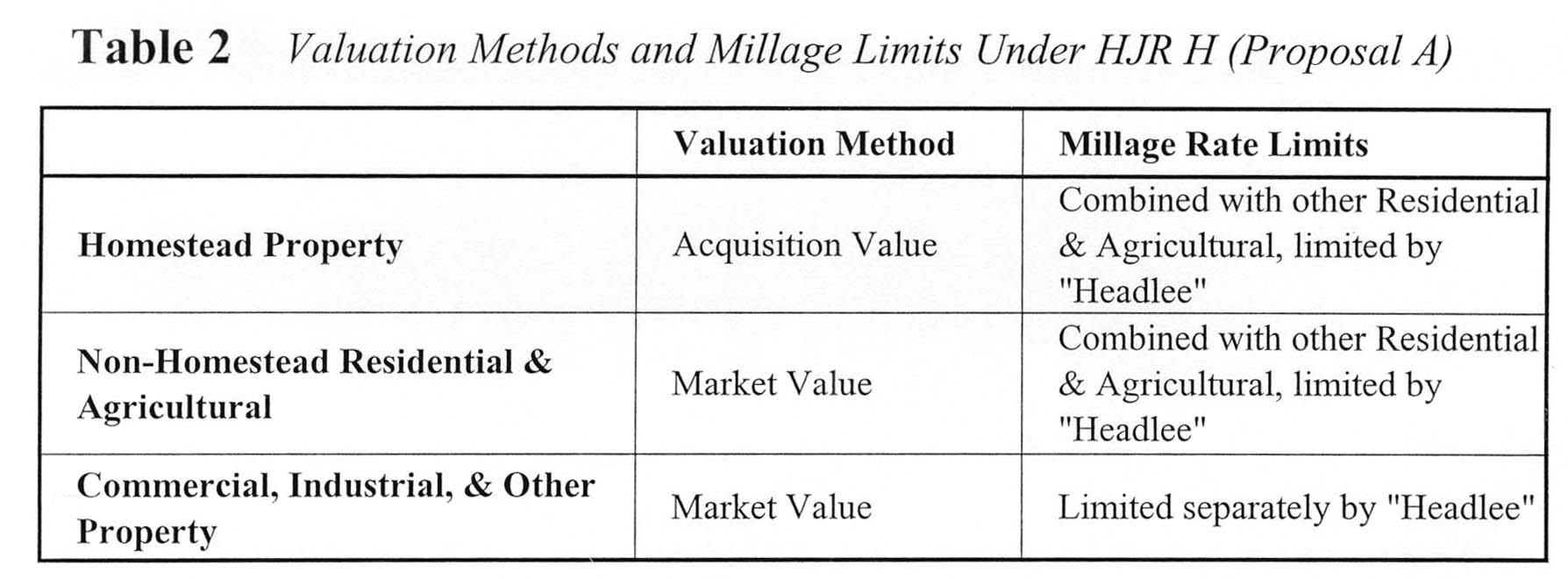

HJR H Creates Three Classes of Property

HJR H would actually create three classes of property:

Homestead property;

Non-homestead Residential and Agricultural property; and

Other property, including Commercial, Industrial, Timber-Cutover, and Developmental. Commercial and Industrial property would comprise the majority of these classes, and they are often lumped together as "business" property. [15]

Each of these would face a different combination of valuation methods and millage rate limits. See Table Two.

Split-Headlee Rollbacks vs. Homestead Assessment Cap

One of the primary motivations for HJR H was to protect homeowners from assessment increases that, some felt, would often be larger than those on commercial and industrial property. The drafters inserted two elements to ameliorate this: an assessment growth cap on homesteads only, and Headlee rollbacks by class. Unfortunately, the two elements work directly against each other, and would often result in the very group HJR H is designed to protect – homeowners – paying higher millage rates!

This occurs because the Headlee rollback provisions of Article IX Section 31 of the Constitution depend directly on the SEV calculated according to Article IX Section 3. Since HJR H would amend section 3 to limit the SEV growth on homesteads, the residential and agricultural class will appear to have slower SEV growth than actually occurred. Thus, when calculating the required rollbacks in millage rates for the two classes, "business" property would often show higher SEV growth, and therefore would have millage rates reduced by the Headlee amendment. However, residential and agricultural property, of which the majority will often be homestead parcels, would have SEV growth artificially capped, and hence would see fewer and smaller Headlee rollbacks.

The results in different communities would vary widely, and would depend on the difference between the actual inflation rate and the arbitrary 5% growth cap contained in RJR H. If inflation – and therefore the expected increases in property values – was higher than 5%, millage rates on "business" property would trend below that of residential and agricultural property in many communities.

Interaction with Millage Limits

HJR H would not change the Constitution's limits on property tax millage, but would open the door to significant mischief with the limits.

Under HJR H, different classes of property would face different millage rates. Article IX Section 6 limits "the total amount of general ad valorem taxes imposed on real and tangible personal property for all purposes" to certain limits, notably the 50-mill limit for counties, townships, and school districts. The section further allows separate limits for charter authorities, and exempts voter-approved debt millage. Under HJR H, the multiplicity of millage rates would complicate the limit calculation. With probably two millage rates for every level of government, how do you add them up?[16]

The Constitution clearly attempts to limit the highest possible sum of millage rates, and the best interpretation would be the same under HJR H.[17] However, HJR H would admit the possibility of imaginative ways to exceed the limit, by creatively adding up millage rates.

Tax Increases on One Class of Property

Although the proposal does not state so explicitly, the HJR H could allow increases in millage rates on one class of property alone. Such a single-class tax increase – impossible under the current constitution's uniformity requirement – could come about through a variety of ways:

Split "Headlee" Rollup

Should millage rates have been previously rolled back on one class, but remain at their voted rates for another, local governments could perform a "Headlee rollup" on just the rolled-back class.

For example, assume a voted school millage rate of 35 mills. Under HJR H, if inflation is 5%, and "business" property grows at 8% for three years, the "Headlee" rollback would reduce its maximum rate to about 32 mills. If the SEV of residential and agricultural property grew at or below 5% – homesteads are limited to 5% annual assessment growth unless sold – they would receive no rollback. This would result in a millage rate of 32 for "business" property, and 35 for residential.

However, if in the following year assessments for all classes did not grow, and inflation was above 9%, the school board could directly increase millage rates on just the "business" property through a simple vote of the board.[18]

Increase by Equalization

If a county or state equalization board were to determine that a jurisdiction's assessments were too low, and order an increase in the SEV for the whole jurisdiction, such an increase could fall only on non-homestead property.

For example, assume that a jurisdiction had its homestead parcels all increase at the maximum 5%, and calculated the Headlee rollbacks based on these figures. Subsequently, the county or state equalization board orders the jurisdiction to increase its SEV through a simple factor of say, 1%. However, since the Constitution (as amended by HJR H) would override the equalization statute, the increased factor could only be applied to non-homestead properties. If homesteads were 50% of the tax base, that would mean a nominal 1% increase would be transformed into a 2% increase in SEV – and therefore in effective tax rates – for all non-homestead property.

State and county equalization boards could partially avoid this by ordering only equalization adjustments on classes other than residential. However, this would still leave non-homestead residential parcels without equalization.

This problem begs the question: what equalization could occur under HJR H?[19] This would be largely left to implementation by the legislature. Because of the uncertainties involved, the effect of implementation would be large.

Voted Increase on One Class

After Headlee rollbacks on one class of property reduce that class's millage rate, an attempt could be made to vote a higher millage rate on just that class. This could be either a new authorization, or a "Headlee override" vote. Since "business" property would likely receive more Headlee rollbacks than residential, many local governments may find it easy to attain voter approval of higher tax rates on businesses, since businesses cannot vote.

Pre-emptive Tax Increase

If local units of government subject to the 50-mill limit vote more than 50 mills, then the last voted millage must be reduced to comply with the limit.[20] Under RJR H, a municipality would be tempted to vote higher millage rates even though they exceed the limit and could not be immediately levied. Subsequently, when the split-Headlee rollback provision of HJR H results in reductions in millage rates for one or more classes, the previously-voted mills would then be levied – without any vote of the people. This could occur soon, or years later, and just residential & agricultural, just "business" property, or both.